Macro Events & News

FX News

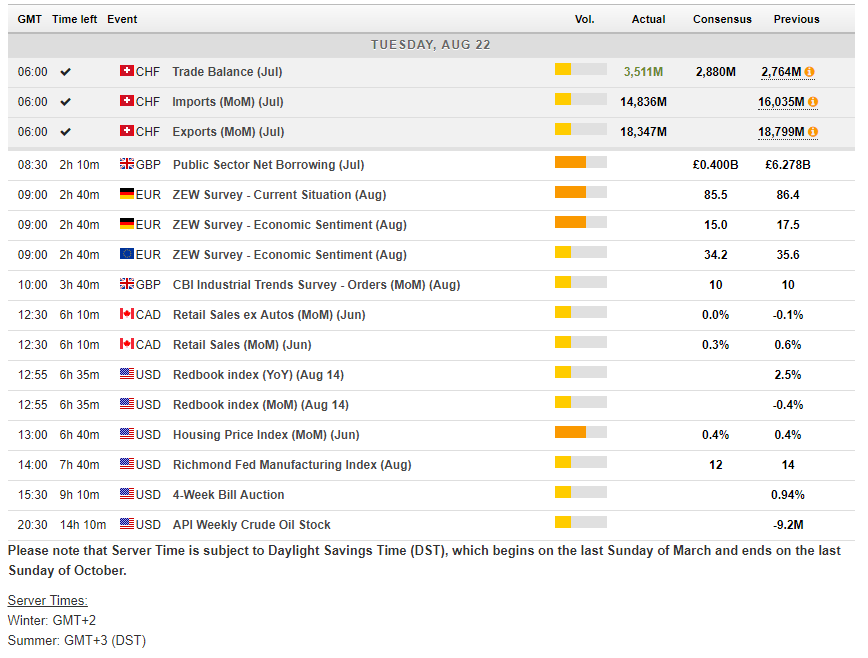

European Outlook: Asian stock markets mostly moved higher in quiet trade, after Wall Street managed to close with slight gains. Hong Kong stocks outperformed on positive earnings report, while Japan underperformed despite a weaker Yen. U.K. and U.S. stock futures are moving higher and it seems risk appetite is slowly returning, after being knocked back by geopolitics. Bund futures continued to rise though in after hour trade yesterday the 10-year Bund yield, which closed below 0.4% may make little headway at the start. The local calendar is hotting up today, providing some distraction from the political arena. German ZEW investor confidence and the U.K.’s CBI industrial trends survey will give a flavour of the economic situation on both sides of the Channel and the U.K. also has public finance data for July.

FX Update: The dollar has traded softer versus many currencies during the pre-London session in Asia, including against the euro, and commodity and emerging world currencies, though the greenback gained versus the yen. A revival in risk appetite brought some pressure on the Japanese currency, while there remains a degree of position jostling ahead of the Jackson Hole symposium (which starts on Thursday). USD-JPY lifted back to the low 109.0s after dipping yesterday to a low of 108.63, which by our data is 3 pips above last Friday’s four-month low. EUR-USD, meanwhile, ebbed back to the 1.1800 level after yesterday logging a one-week high at 1.1828, and USD-CAD carved out an 18-day low at 1.2547 and AUD-USD a three-session peak, at 0.7950. Cable has entered its fifth consecutive session of orbiting 1.2900.

Canada’s wholesale report maintained the outlook for weak June GDP, with a flat reading (0.0%) expected after the 0.6% GDP surge in May. Wholesale shipment volumes fell 0.7% in June. The final ingredient for GDP is today’s retail sales report, where a 0.3% gain is expected in total shipment values, which a larger (0.5% or better) improvement in volumes. Housing starts grew 9.5% to a 212.9k pace in June from 194.5k in May. Hence, the contribution from construction production should be positive. The outlook for mining, oil and gas production is to the downside. Energy export values plummeted 9.2% m/m in June while petroleum and coal manufacturing shipment values dropped 7.1%. However, the erosion in petro and coal values was driven by falling prices, suggestive of a less pronounced decline in the GDP report’s petro and coal volume measure. A flat reading in June GDP would leave a lofty 3.7% growth pace for Q2. Moreover, any pull-back in June GDP should be temporary. Hence, the broader theme of upbeat growth remains supportive of a 25 bp rate hike from the BoC to 1.00% in October.

Main Macro Events Today

German ZEW Sentiment – German ZEW investor confidence expected to be particularly impacted by the latest spell of risk aversion in markets and are looking for a decline in the headline August reading to 15.5 from 17.5 in July.

Canada retail sales – Retail sales, expected to rise 0.3% m/m in June after the 0.6% expansion in May. Another firm month is expected for seasonally adjusted vehicle sales. CPI implies a drag on retail sales values from falling prices. Notably, falling gasoline prices should weigh on total and ex-autos retail sales, and hence we’d put the risk to the downside on this report.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in