Macro Events & News

FX News

European Outlook: Risk aversion amid tensions between the U.S. and China continued to hang over markets during the Asian session. Still, losses in Japan and Australia were relatively modest, while Hong Kong stocks underperformed and are heading for the biggest lost since last year amid concerns about the tensions between the U.S, and North Korea. U.K. stock futures are actually slightly higher, while U.S. futures remain in the red. Investors remain nervous but Bund futures started to move down from highs during the PM session yesterday and yields are likely to have bottomed for now. Eurozone markets underperformed and spreads widened, which highlights that peripheral yields remain vulnerable to bouts of risk aversion. Overnight, RNBZ left the official cash rate unchanged, while announced that inflation remains subdued. Today’s calendar has production and trade data from the U.K. as well as production data from France and trade data from Italy. Released overnight, the U.K. RICS house price balance fell back to 1% from 7%, further adding to signs that the housing market is slowing down.

U.S. reports: revealed a solid round of June wholesale trade figures after big upward May revisions that lifted prospects for GDP, alongside a slightly stronger than expected 0.9% Q2 productivity rise after revisions that paralleled the annual revisions in the GDP and income reports. Now it is expected a Q2 GDP growth trimming to 2.4% from 2.6%, with a $7 bln boost in wholesale inventories but downward revisions of $3 bln for factory inventories and $9 bln for construction. The Q3 GDP growth still expected at 3.3%, with a $26 bln inventory addition. Yet, even with today’s firm inventory gains, inventories have yet to recover from the big 2015-2016 petro-hit, and wholesale petroleum inventories fell by a hefty 5.2% in June despite a 1.9% sales rise.

Fedspeak: Fed’s Bullard said there’s risk the FOMC could be too aggressive on rates, in comments on Bloomberg radio yesterday. The Fed doesn’t need to be preemptive on rates due to weak inflation trends. Rates can be left on hold for now as data are evaluated. The drop-in inflation has surprised policymakers. The G-7 is in a low growth, low inflation regime. And he’s not too optimistic that price pressure will pick up this year. These aren’t surprising comments from Bullard, who has turned more circumspect on rate hikes, still looks for QT to begin this year, but with a slow, incremental start. Chicago Fed dove Evans on the other hand, sees balance sheet reduction in September as quite a reasonable juncture to start, while a December rate hike is possible, though dependent on inflation. He argues that the Fed “should be very careful” in assessing future hikes, since he wants more evidence that inflation is heading to 2% sooner than later. Evans sees current policy as accommodative, while the economy is doing well and likely to average 2.25-2.50% growth the next few years, which is how long it will take to unwind the balance sheet. He believes there’s reasonable chance inflation could reach 2% in the next few years and he doesn’t see major risks of financial instability, at least certainly not due to Fed policy.

Main Macro Events Today

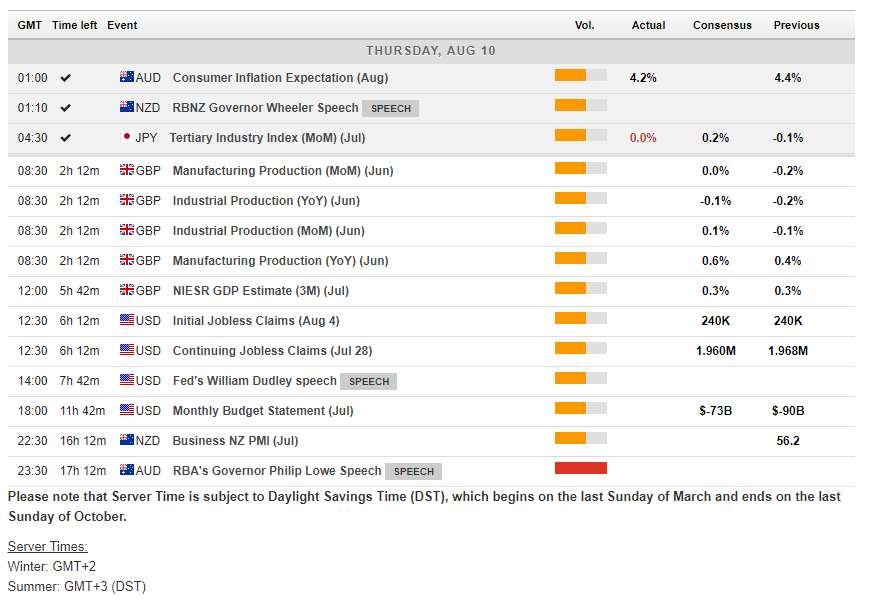

UK Production – Production data for June are up today, where expected at a 0.1% m/m contraction but 0.1% y/y expansion.

U.S. PPI – July PPI is out today and should post a 0.1% headline with the core up 0.2% for the month. This follows June data which had both the headline and core up 0.1% on the month. After a series of declines through the spring, oil prices climbed in July which could help to lift the headline.

U.S. Initial Jobless Claims – Initial claims data for the week of August 5 should tick down to 239k (median 240k) from 240k last week and 245k in the week before that. Initial claims look poised to settle at a 242k average in July that about matches the 243k average from June.

RBA Gov. Lowe – Governor Wheeler holds today his usual press conference after the announcement of inflation rates last night.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in