Macro Events & News

FX News

European Outlook: The Fed’s reluctance to commit to a time for QT beyond “relatively soon” and the fact that the Fed appeared to be moderately more concerned that the decline in inflation pressures could be a little more durable than previously thought has given bond as well as stock markets a fresh boost. Equities moved mostly higher in Asia overnight (China’s CSI 300) once again a notable exception, with commodities still underpinned as oil prices hold clearly above USD 48 per barrel. Bund futures already jumped higher in after hour trade yesterday and European stock futures are rising in tandem with U.S. futures, pointing to broad gains on European markets at the start. ECB’s Nowotny may have repeated his support for reduced asset purchases again, but that the ECB will start to taper next year is pretty much expected and Nowotny yesterday urged caution when the ECB starts to “take the foot of the gas”. Today’s calendar has Eurozone M3 and the U.K. CBI distributive trade survey.

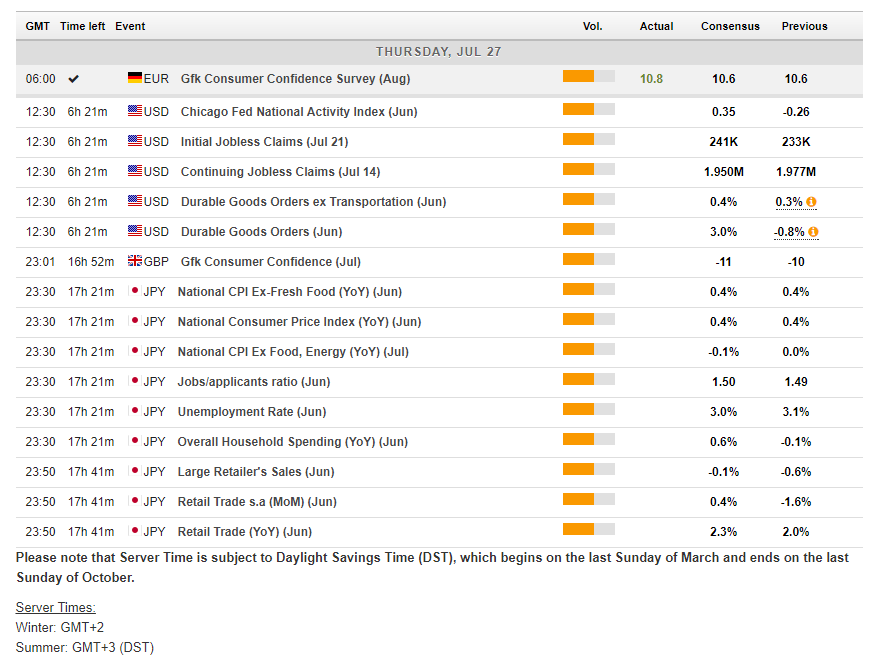

German GfK consumer confidence surges to record high of 10.8 from 10.6 in the previous month. The unexpected jump higher ties in with record Ifo readings and confirms that the German recovery remains firmly on track. More arguments for the ECB to take the “foot off the gas” and reduce monthly asset purchases. The full GfK breakdown, which is only available until July showed also falling price expectations though, alongside improved economic confidence and the willingness to buy dipped despite a sharp drop in the willingness to save. Hence, some mixed signals and somethings for the doves, who continue to fret about low inflation and wage growth.

FOMC: held rates steady and gave no firm date on the balance sheet unwind. However, the policy statement did indicate the run-off will begin “relatively soon,” versus this year in the June statement, though it basically reiterated comments from Fed Chair Yellen in her recent testimony. The decision was unanimous. The Fed said the economy has been rising moderately while job gains have been “solid.” On inflation, the Fed said overall and core prices have “declined and are running below 2 percent; survey-based measures of longer-term inflation expectations are little changed, on balance.” Inflation developments will continue to be monitored “closely.” One important change versus the June statement was the elimination of word “recently,” referring to the decline in inflation, suggesting there’s some concern the weakening will be more long lasting.

U.S. reports: revealed rise in MBA mortgage market index at 0.4%, alongside a 2.2% drop in the purchase index and a 3.4% rise in the refinancing index for the week ended July 21. The average 30-year fixed mortgage rate sank 5 basis points to 4.17% after yields drifted lower last week with Europe. Also, U.S. new home sales edged up 0.8% to 0.610 mln in June. That follows the 4.9% rebound to 0.605 mln in May after the 9.6% April drop to 0.577, for a net -27k revision. New home sales hit a cycle high of 0.638 mln in March amid mild winter weather and hopes for Trump stimulus. The months’ supply of homes moved up to 5.4 from 5.3. The median sales price declined 4.2% to $310,800 following the 4.8% rise to $324,300 in May. Prices are down 3.4% y/y in June versus a 9.6% y/y gain previously.

Main Macro Events Today

US Durable goods, Jobless claims – Durable goods orders are forecast to snap back 3.0% in June vs -0.8% in May, while the advanced trade gap may narrow to-$65 bln from -$66.3 bln and initial jobless claims are set to rebound 8k to 241k for the week ended July-22.

UK CBI distributive trade & Gfk – The distributive trades report is expected to fall to a reading of 10% in the headline realized sales figure after 12% in June.The GfK Group Consumer Confidence index is expected to fall to a reading of -11 after -10 in June.

Japanese Data – The calendar features the CPI data. June national prices are seen unchanged at 0.4% overall, and same for a core basis. June unemployment is seen falling a tenth to 3.0%, while the job offers/seekers ratio is expected at 1.50 from 1.49. June personal income and PCE are due, with the latter forecast to have risen 0.6% y/y from -0.1% previously. Lastly, June retail sales are penciled in at a 0.1% y/y rate from -0.6% for larger retailers, and up 2.3% y/y from 2.1% overall.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in