Macro Events & News

FX News

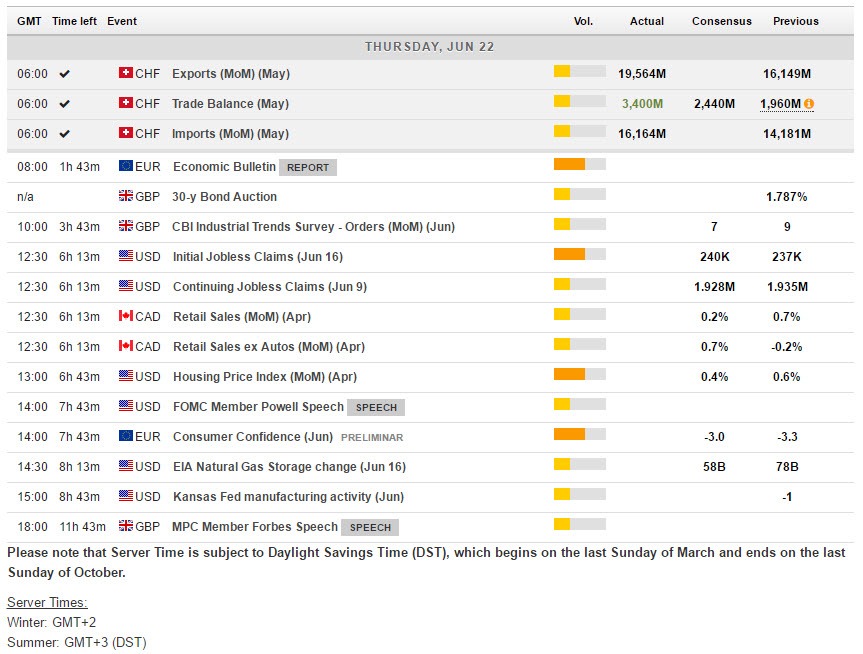

European Outlook: Asian stock markets stabilized in China’s CSI outperformed again helped by the inclusion of 222 mainland equities in the MSSCI index. The ASX, which tanked yesterday with oil also bounced back. The front end WTI future is little changed on the day at USD 42.53, U.K. and U.S. stock futures are also little changed The Reserve Bank of New Zealand held the policy rate unchanged, as expected. Bund and Gilt yields already moved higher yesterday, led by a jump in the 10-year Gilt above the 1% mark after hawkish comments from BoE’s Haldane, which sees a case for raising rates soon. Bunds outperformed, but the 10-year yield also nudged higher, while Eurozone spreads were mixed at the close with Portugal underperforming. Equity markets and oil prices remain in focus although the calendar is starting to pick up with French business confidence indicators as well as the U.K. CBI industrial trends survey and the ECB’s latest economic report. EU leaders will also start to gather for a 2-day Brexit summit, after chief negotiators from both sides met for the first time officially last Monday. The Eurozone also has preliminary consumer confidence data in the afternoon.

US Reports: A 1.1% U.S. May existing home sales bounce to a 5.62 mln rate trimmed the April drop to 5.56 mln from a 5.70 mln cycle-high in March to almost exactly track estimates, as sales gains moderate in Q2 after weather boosts in the prior two quarters. U.S. existing home sales came in on the perky side, but had little impact on forex markets. Existing home sales are on track for a 5% rise in 2017, following a 3.9% increase in 2016 and a 6.5% rise in 2015, but a 2.9% 2014 “taper-tantrum” drop. Additionally, U.S. MBA mortgage market index rose 0.6% in data released yesterday, in addition to a 1.0% drop in the purchase index and a 2.1% rise in the refinancing index for the week ended June 16. Yet the average 30-year fixed mortgage rate was unchanged at a low 4.13% last week after readily absorbing the Fed’s rate hike, projections and balance sheet reduction schedule announcements.

RBNZ: The Reserve Bank of New Zealand held the policy rate at 1.75%, as expected. Low for long remains in place, with Wheeler again saying, “Monetary Policy will remain accommodative for a considerable period.” And a dovish bias was retained, as the Governor concluded that “Numerous uncertainties remain, and policy may need to adjust accordingly.” This was the same as in May. In March he said “Numerous uncertainties remain, particularly in respect to the international outlook, and policy will need to adjust accordingly.” In other words, it looks like they won’t hesitate to add accommodation if downside risks to the economy manifest. The onus remains on the inflation and growth data, with additional undershoots setting the stage for further easing.

UK: The new UK government’s legislative goals have been announced in the Queen’s speech. Eight of the 24 outlined are Brexit related, which include bills to convert EU rules into UK law, and others concerning such issues as trade, immigration, agriculture and sanctions. A number of key manifesto pledges have been axed or delayed as a consequence of the Conservative Party having lost its majority at the elections earlier in the month. Chancellor Hammond on Monday said that the economy would be the priority in Brexit negotiations, which appears to be position shift away from prioritizing immigration. This could potentially be supportive of the pound, though issues about the fragility of the minority government (which is reportedly struggling in negotiations with Northern Ireland’s DUP) are likely to be the overriding concern for markets. BoE Chief Economist Haldane gave a speech as well yesterday in which he said he is ready to vote for a rate hike — notable as he voted to keep policy settings unchanged last week. His vote would bring the hawks in favour of hiking the repo rate by 25bp to four — which is half of the members on the Monetary Policy Committee.

Main Macro Events Today

US Initial Jobless Claims – Initial claims data for the week of June 17 should reveal a slight increase to 240k from 237k in the week prior and 245k in the week before that. Claims have been holding at very tight levels lately and the June average expected to be 236k, down from 241k in May and 243k in April.

Canadian Retail Sales – Retail sales are seen growing 0.9% m/m in April, while the ex-autos sales aggregate gains 0.7%. Higher gasoline prices should support retail sales, but weaker vehicle sales will weigh.

Fedspeak – Governor Powell testifies on fostering economic growth before the Senate Banking Committee.

MPC Forbes Speech – BOE MPC voting member Kristin Forbes is due to give a speech today at the London Business School.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in