Macro Events & News

FX News

European Outlook: Asian stock markets mostly headed south, after losses on Wall Street and in Europe yesterday. MSCI finally decided to include 222 large Chinese companies in its 2018 Emerging Markets Index, and the CSI is outperforming with a 0.28% gain, while the Hang Seng is down -0.38% and the Nikkei -0.32%, with the latter weighed down by a stronger Yen. The ASX underperformed and lost more than 1% as oil prices remain under pressure. The DAX rallied to new record highs yesterday, before profit taking and a broad mover lower in global equity markets as commodity supply concerns amid rising oil production in Libya and Nigeria cast fresh doubt on the efficacy of the OPEC oil agreement while a 26% drop in Chinese steel exports added to concerns about the global growth outlook. U.K. and U.S. stock futures are also down and the fresh bout of risk aversion will keep a lid on bond yields. For the Eurozone, the good news though is that peripheral yield spreads over the German benchmark didn’t blow out yesterday. Today’s data calendar remains quiet, with only U.K. public finance data and a German 30-year Bund sale.

London clearing remains bone of contention. After the EU proposal that called for greater EU oversight of clearing houses based in foreign jurisdictions and included the option of enforced relocation, BoE’s Carney yesterday suggested improved cross-border oversight of clearinghouses that should be based on “deep cooperation” between jurisdictions, adding that a clearing deal would help to keep the financial system resilient. ECB’s Coeure meanwhile stressed that the EU’s clearing regime was “never designed to cope” with major clearing houses operating outside of the EU, adding that moving clearing to within the EU’s jurisdiction would be justified if they pose a major risk to stability, as so far, the regime provides “EU authorities with very limited tools for obtaining information and taking action in the event of a crisis”. The ECB has long tried to get London clearing under its own control and while London fought back with backing from a European court, the issue is back on top of the agenda as Brexit draws nearer.

Fedspeak: Yesterday Fed’s Rosengren said low rates pose financial stability issues, in his comments at the Riksbank macroprudential conference. The Boston Fed president (not a voter this year) turned decidedly hawkish about a year ago and has maintained that outlook ever since. He believes low rates put intermediaries and economies at risk, make fighting future recessions more difficult, and make it more likely central banks will have to resort to non-traditional policies. Additionally, Fed Evans was speaking yesterday as well. Chicago Fed dove Evans said inflation needs to rise and the target should not been seen as a cap but a symmetric target, though he’s voted for rate hikes given improvement in the economy. He’s still ambivalent about the timing of the next hike, which could take place later in the year, while the global environment appears to be holding back inflation, which could allow for a shallower path of rate increases. Otherwise the economy bounced back after the election, with “quite good” fundamentals, which give inflation a chance to get back to 2%. He sees 3% growth as achievable in the short-term, but sustaining it given labor and productivity constraints is another thing, while the U.S. is fast approaching its natural rate of unemployment.

Canada: growth maintains momentum but uncertainties lurk, suggesting that while the time frame for rate hikes has been moved ahead, the Bank can maintain the current setting through mid-year at least. Of course, the upbeat (“hawkish”) view of the economy last week moved ahead expectations for lift-off, and even put the announcement next month in play. And the economic data since Wilkins/Poloz have supported the Bank’s view that the run of encouraging broad-based growth will prove sustainable. But other events have highlighted the uncertainties around Canada’s outlook. Most prominently, the plunge in WTI crude oil to a seven month low and the evolution of U.S. trade policy. The key line from Wilkins was that they are “assessing whether all of the considerable monetary stimulus presently in place is still required.” An assessment of the mix of firm economic data but weak oil/commodity and uncertain U.S. trade policy will likely keep them grounded until later this year, if not January of next year. There will be another round of BoC-speak next week (Poloz panel, Patterson speech), which will be looked to for fresh guidance on the policy outlook.

Main Macro Events Today

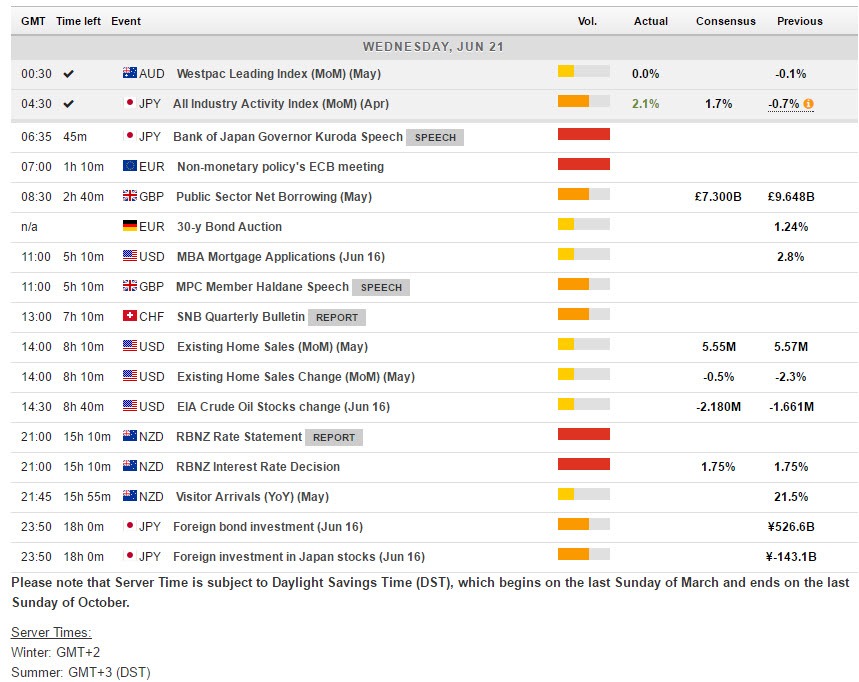

US Existing Home Sales – May existing home sales data is out today and should post a 0.7% increase to a 5.610 mln pace for the month after dropping 2.3% to a 5.570 mln pace in April. The NAHB did tick higher in May with a rise to 69 from 68 in April but housing starts disappointed with a decline in the headline pace to 1.092 mln from 1.156 mln in April.

UK Borrowing data – Monthly government borrowing data are due (today), for which a deduction to £7.3B is expected from £9.6 seen last month.

Speeches – BoE chief Economist Andy Haldane is due to give a speech today in Yorkshire.

RBNZ Meeting – New Zealand’s calendar is highlighted by the Reserve Bank of New Zealand’s meeting today. No change to the current 1.75% rate setting is expected. It’s been at this level since the predicted easing on November 10.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in