Macro Events & News

FX News

European Outlook: Asian stock markets were mixed, with Chinese stocks under pressure as financial and developers headed south. The CSI 300 lost more than 1% and the Hang Seng is down 0.2%, while Nikkei and ASX are moving higher. Financials also weighed on Japan’s stock markets, while defensive stocks gained ahead of the FOMC announcement, leaving the Nikkei up a modest 0.2%, while the ASX 200 gained 0.8%. FTSE 100 futures are up, as Sterling is under pressure again, while U.S. futures are down ahead. All eyes are on the Fed which is expected to hike rates by 25 bp, but may not give details on balance sheet normalization yet. There is speculation that China’s central bank may follow, which is adding to pressure on Chinese markets. China industrial production and retail sales growth were unchanged from the previous month. The European calendar has U.K. labour market data and EMU production numbers.

FX Update: The dollar majors have been settled in narrow ranges into the Fed’s policy announcement and statement. EURUSD has been orbiting 1.1200 and USDJPY has continued to oscillate around the 110.00 level. Sterling has steadied after rebounding some of the ground lost since last week’s UK election, with markets buoyed by prospects for a softer Brexit stance, though concerns about the viability of the new, fragile minority government, along with the prime minister’s future, remain. As for the Fed, a 25bp hike is widely expected while there is a degree of uncertainty about what tone the central bank’s guidance will take. The Fed expected to stick with its tightening bias but may signal a lowered pace of policy normalization, which will be accompanied with reduced growth forecasts. Overall, much of this will have been discounted by markets, though we see some risk for dollar gains on the view that the Fed leaves the door open for another 25bo rate hike before year-end.

U.S. reports: Flat May U.S. PPI headline with a 0.3% core price increase beat estimates with a largely expected 3.0% drop for the goods component. There were no revisions to April’s 0.5% headline jump and the 0.7% surge in the ex-food and energy component. On an annual basis, PPI slowed to 2.4% y/y compared to 2.5% y/y for April. But the core rate rose to 2.1% y/y versus 1.9% y/y. Goods prices declined 0.5% on the month, versus the prior 0.5% rise, with energy tumbling 3.0% and food costs dipping 0.2%. Services prices rose 0.3% following the 0.4% April gain, with trade prices climbing 1.1% and transportation/warehousing costs falling 0.5%. The PPI report isn’t usually a market mover, however U.S. equities have recovered somewhat to start the session in the wake of the 0.3% core PPI rise, following a shallow recovery in global stocks after two days of U.S. tech sector liquidation.

Final May German HICP inflation was confirmed at 1.4% y/y, as expected and down from 2.0% y/y in April. The Easter effect was largely to blame for the sharp swings over the past months, with holiday related prices spiking in April only to fall back again after the end of the Easter holidays. Energy prices increases also fell back again in May and added to the drop in the annual rate, as gas prices declined -3.4% y/y and prices for heading rose 11.7% y/y, down from 30.1% y/y in the previous month. The German economy may be steaming ahead and the labour market looking increasingly tight, but so far at least that has not led to a substantial uptick in wages, which is what is also keeping the ECB on hold, despite stronger growth numbers.

Main Macro Events Today

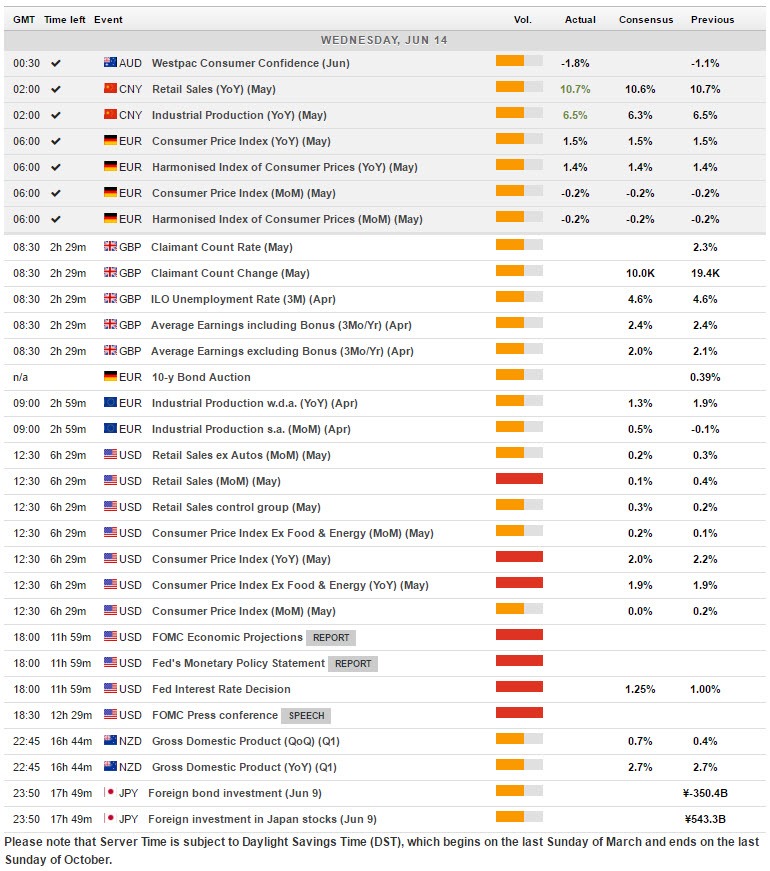

- US CPI – May CPI data should reveal a -0.1% headline with the core rate up 0.2%. This follows April figures which had the headline up 0.2% and the core up 0.1%. If data in line with forecast would leave the headline y/y rate slowing to 1.9% from 2.2% in April and the core y/y rate ticking down to 1.8% from 1.9% in the month prior.

- US Retail Sales – May retail sales data is out today and should post a 0.1% headline decline a flat ex-autos figure. This follow the April report which revealed a 0.4% headline and a 0.3% core pace. The report faces downside risks from the weak auto sales data and an anticipated decline in gasoline prices which could weigh on gas station sales.

- FOMC Meeting – The Fed began its 2-day meeting, with widespread expectations for a 25 bp increase in the rate band to 1.0% to 1.25%. What will be crucial for the markets is the tone of the statement and what policymakers suggest about the path of normalization. The Committee is likely to leave its dot forecast of three tightenings this year unchanged, as the tight labor market should offset the slowing in Q1 growth and the softening in inflation. While the risks to the economy should remain balanced, it will be interesting if the tone is a little more dovish given the slowing in Q1 and other more recent data.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in