Macro Events & News

FX News

European Outlook: Asian stock markets headed south as oil prices fell amid disappointment over the OPEC’s decision to prolong supply cuts for nine months, with investors hoping for more than an extension of current measures. The front end WTI future is trading at just USD 48.62 per barrel and lower than expected oil prices, coupled with a strong EUR also mean the ECB could well cut back its inflation forecast at the June meeting. More ammunition then for the likes of Constancio, who yesterday evening once again stressed that inflation is not yet on a sustainable path towards desired levels. UK100 futures are little changed, after managing to post a marginal gain yesterday against losses on Eurozone bourses. Today’s calendar remains quiet, with only Italian confidence data and after public holidays in many Eurozone countries yesterday many have taking today off for a long weekend, so that trading conditions may well be quieter again than normal.

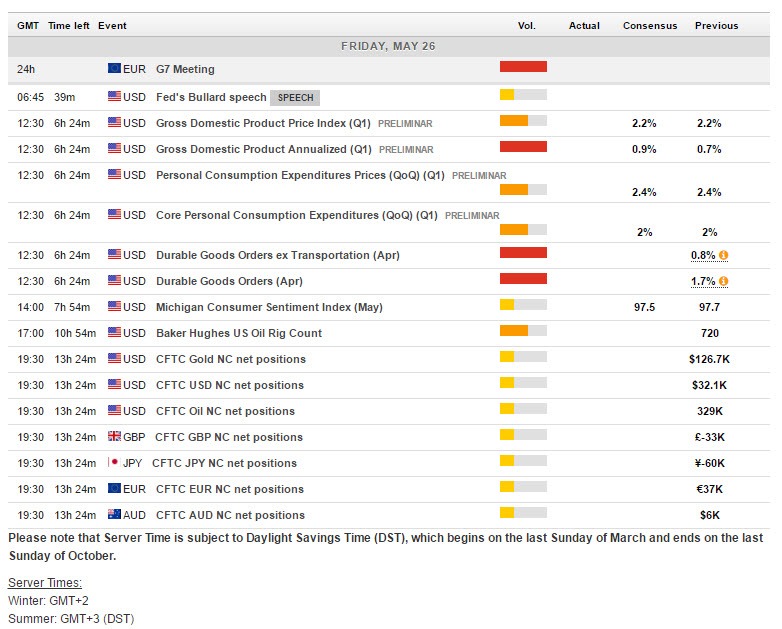

US reports: revealed an array of downside disappointments in the April advance indicators report for the trade deficit, and wholesale and retail inventories, though we also saw another round of super-tight initial claims figures that capped the damage. Inventory revisions in the March data trimmed our Q1 GDP estimate for today’s report to 0.8% from 0.9%, versus a 0.7% advance figure. The tight 234k claims figure for the third week of May suggests upside risk for May nonfarm payroll estimate.

ECB’s Constancio: Overall risks remain tilted to the downside, stressing once again that “monetary stimulus remains important to ensure a sustainable adjustment of the inflation process towards levels consistent with the ECB price stability objective”. The central bank’s Vice President clearly pushed back against calls to start signaling exit steps and stressed that “a sustainable adjustment” of inflation has not yet occurred, even as inflation is starting to adjust towards desired level. At the same time, he suggested that negative rates could become part of the “conventional toolkit of central banks for fighting recessions”

UK Q1 GDP data was unexpectedly revised lower in the second estimate. This compares to the 0.7% q/q growth seen in Q4, and also shows the UK economy to be underperforming the Eurozone’s growth rate of 0.5%. The data shows the UK economy has started the year on a weaker than expected footing, and while April PMI survey data tentatively portended a rebound in early Q2, the backdrop of negative household income growth and a May CBI retail sector survey showing a sharp slowing in consumer activity suggests that the UK is set for a relatively rocky path this year. The BoE has been anticipating weakness, having trimmed its 2017 GDP forecast to 1.9% from 2.0% in its quarterly inflation report in early May.

Main Macro Events Today

US Durable Goods – Durable orders are seen dropping to -1.4%, erasing the 1.7% in March, and ending a string of three straight monthly gains.

UoM Consumer Sentiment – The final reading on May consumer confidence from the University of Michigan survey is seen at 97.5 from, 97.7.

US Prelim. GDP – Q1 GDP is expected to be revised up to a 0.9% rate of growth from the 0.7% Advance report.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in