Macro Events & News

FX News

European Outlook: Asian stock markets moved broadly higher, with Chinese equities in particular shrugging off yesterday’s ratings downgrade and the CSI 300 rising more than 1%. A jump in oil prices ahead of a key producers meeting underpinned sentiment. The Fed minutes yesterday were relatively dovish, but still said that recent economic and inflation weakness is expected to pass. U.K. and U.S. stock futures are moving higher and it seems risk appetite has returned to stock markets. Bund futures still climbed in after hour trade yesterday, but this could fade with improving risk appetite. Today’s calendar has second GDP readings for Q1 from Spain and the U.K. as well as U.K. BBA loans for house purchase.

US reports: 2.3% U.S. April existing home sales drop to a 5.57 mln rate from a 5.70 (was 5.71) mln cycle-high slightly undershot estimates, following a February drop to a 5.47 mln clip from a 5.69 mln prior cycle-high in January, as we unwind the winter existing home sales boost from mild weather as also seen with yesterday’s new home sales report. A 3.5% April median price rise to $244,800 left a tiny gap to the $247,600 all-time high last June, while inventories rose 7.2% in April to a still-lean 1.93 mln. Existing home sales are on track for a 5% rise in 2017, following a 3.9% increase in 2016 and a 6.5% rise in 2015, but a 2.9% 2014 post “taper-tantrum” drop.

Bank of Canada: left policy unchanged, as widely expected, though there were some changes in the statement that generated some market volatility. The BoC altered the key final line to say the current degree of monetary stimulus is appropriate “at present” versus April’s “still appropriate.” The Bank of Canada maintained its cautiously constructive outlook for growth and inflation, as expected. An ongoing improvement in domestic and global growth suggests further satisfaction with the evolution of the recovery. A change in verbiage on the current degree of monetary stimulus to “appropriate at present” from “still appropriate” prompted a fresh reading of the tea leaves, but did not change the outlook for monetary policy.

FOMC minutes indicated a hike could be seen “soon.” However, there was a caveat that it “Members generally judged it would be prudent” to wait to ensure the Q1 slowing was temporary before tightening further. The minutes also included a staff outline of a plan on the balance sheet which would showed gradually increasing run-off caps every three months which would eventually hit fully phased in levels which would then be held at that level until the size of the balance sheet was normalized. Nearly all policymakers supported this plan. The minutes indicated that the Q1 slowing was likely “transitory” and participants generally agreed that the medium term outlook on the economy was little changed — but again there was that caveat noted above. We continue to expect a June hike, and another in September, but the outlook over the rate path in 2H is a little more uncertain considering the potential for balance sheet roll off to begin later in 2017.

Main Macro Events Today

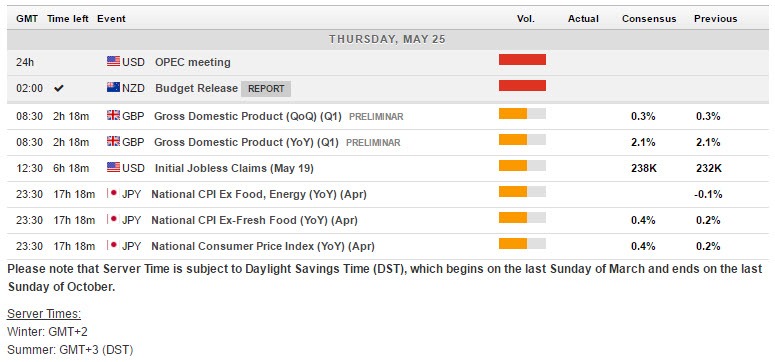

UK Prelim. GDP Q1 – The second estimate of the Q1 GDP report is out today and it is anticipated to come in unrevised at 0.3% q/q and 2.1% y/y.

OPEC – OPEC meets today and is expected to extend its agreement to curtail output.

US Unemployment Claims – Initial claims data for the week of May 20 are out today and an increase is expected in the headline to 238k from 232k last week and 236k in the week prior to that. Claims are poised to average a stronger 236k in May, down from 243k in April and 251k in Marc.

Fedspeak – Fed’s Brainard will participate in a panel discussion on the global economy at 14:00 GMT, in Washington DC.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in