Macro Events & News

FX News

European Outlook: After modest gains on Wall Street yesterday, Asian markets were hit by the Moody’s ratings downgrade for China, which was cut to A1 from Aa3 and left investors wrong footed and CSI 300 and Hang Seng in negative territory. The ASX is little changed, while Japanese bourses managed to outperform, benefiting from a weaker Yen. U.K. and U.S. futures are heading south, although Eurozone markets already outperformed yesterday amid strong data releases, while the U.K. in particular was hit by a bout of risk aversion following the Manchester terror attack. With pressure on the ECB to lay the ground for tightening measures rising, Bunds are likely to continue to underperform. Today’s local calendar is relatively quiet, with German consumer confidence and the second reading of Spanish GDP, which will leave the focus on the Fed minutes.

U.S. reports: revealed big headline drops for April new home sales and the May Richmond Fed index. Yet, the 11.4% April new home sales plunge to a 569k rate followed annual revisions that lifted the sales data through this year’s mild winter, with a whopping 55k in upward revisions for Q1 alone that left a stronger than expected sales path for 2017. U.S. May Markit manufacturing and services PMIs were 52.5 and 54.0, respectively, for the preliminary reads versus April’s 52.8 and 53.1. The composite hence rose to 53.9 from 53.2 previously. These are all higher than the year ago prints of 50.7 for manufacturing, 51.3 for services, and 50.9 for the composite. Most of the key components in manufacturing dipped to the lowest levels since September, though the services components mostly gained, with input prices rising to the highest level since June 2015. The Richmond Fed plunge to 1.0 in May from 20.0 in April and a 7-year high of 22.0 in March left a larger than expected drop into May however, and the ISM-adjusted measure fell sharply to 51.7 from 57.5 in April and a 7-year high of 59.2 in March.

Strong data puts pressure on ECB. A strong round of May confidence data, which showed the German economy in particular firing at all cylinders, makes the ECB’s very expansionary monetary policy and the implicit easing bias increasingly look out of place. Yesterday, German Ifo surges to highest level since at least 1991, while comments over the past week showed that even at the Executive Board there are now voices calling for a signal to markets that exit steps are underway, so that Praet, who favours a very cautious and extremely gradual move out of the easy policy, will face pressure to move not just to a neutral stance, but to introduce a tightening bias, which would pave the way for an announcement on tapering in September. If the central bank starts to cut back monthly purchase volumes by EUR 10 bln a month starting from early next year, rate hikes could come earlier than many expect, even if the ECB sticks with the current sequence of tweaking rates only after QE has ended.

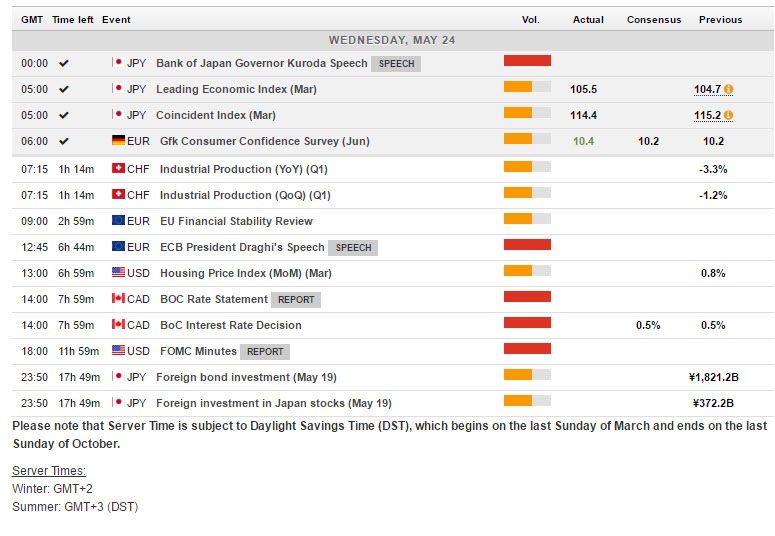

Main Macro Events Today

ECB – ECB’s President Draghi is due to speak at the First Conference on Financial Stability organized by Bank of Spain, in Madrid, at 12:45 GMT.

BoC Rate Decision – The Bank of Canada’s rate announcement is due today, where no change in the 0.50% rate setting and a continuation of the cautious optimism seen in April is projected for today’s announcement. The data since April’s announcement have revealed recovering growth alongside inflation that is still running below the BoC’s target.

FOMC Minutes – The FOMC minutes are due today, while Kaplan will speak at the CD Howe Institute Annual Dinner, in Toronto.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in