Macro Events & News

FX News Today

European Outlook: Equity markets started to improve and Wall Street managed to close in positive territory, as “Trump anxiety” eased somewhat. Markets were still mixed in Asia overnight, with Hang Seng and Nikkei posting slight gains, while CSI and ASX are slightly in the red. FTSE 100 and U.S. stock futures are moving higher though and it seems European markets may manage to claw back some of the losses seen over the last couple of days as investors put aside the turmoil in the Trump administration. Bund futures already started to come off highs during the PM and after hour session yesterday and with risk aversion unwinding Eurozone peripherals could outperform today and Eurozone spreads come in. ECB officials will be keeping a close eye on spreads and the impact of political uncertainty as comments from ECB officials show differing opinions on the speed with which the ECB should communicate the exit steps expected for next year. Data releases include German PPI numbers at the start of the session as well as Eurozone current account and BoP data and the U.K. CBI industrial trends survey for May, followed by EMU consumer confidence in the afternoon.

US Data: Revealed a surprisingly tight 232k claims reading for the May BLS survey week and a hefty May Philly Fed surge to 38.8 that nearly reached the 33-year high of 43.3 seen in February, alongside a 0.3% leading indicators rise that left an eighth consecutive gain, and an uptick in the Bloomberg consumer comfort index to a lofty 50.2. The employment components of the Philly Fed survey diverged around high levels, leaving upside risk from both this survey and the claims data for our 195k May nonfarm payroll estimate. The solid path for the monthly indicators into Q2, alongside room for an inventory updraft into the second half of 2017 after the big Q1 setback bodes well for GDP, where we expect a growth bounce to 3.2% after a Q1 boost to 0.8% from 0.7%, alongside a robust 6% Q2 clip for industrial production after a 1.8% Q1 pace.

Treasury Secretary Mnuchin believes 3% GDP or better is achievable, in his first testimony before the Senate Banking Committee. The acceleration in growth is possible “if we make historic reforms to both taxes and regulation.” The top U.S. priorities he noted are tax overhaul, housing finance and regulatory reforms, and combating terrorist financing.” And he added we are “committed to rethinking our foreign agreements and trading practices to ensure they are both free and fair to American businesses and workers” (remember earlier today USTR Ross notified Congress that the administration is triggering Nafta negotiations). On taxes, Mnuchin repeated that the objective of tax reform is for a cut for middle income earners. Meanwhile, House Leader Ryan attempted to get back on message about tax and regulatory reform, while expressing support for an independent special counsel to “follow where the facts lead” on the Russian probe. Later a video emerged that seemed to back up the White House’s assertion over Comey and let the president off the hook. Cable lost over 100 pips as the USD recovered.

Fedspeak: Cleveland Fed hawk Mester expects further Fed hikes will be necessary if the economy evolves as expected, while delaying hikes too long would risk a recession. She’s also comfortable with altering the Fed’s balance sheet policy later this year and once that plan is decided the Fed should stick to it and use rates to respond to the economy. This is totally in character and in keeping with the hawkish non-voter’s track record and prior remarks.

Main Macro Events Today

CAD Retail Sales – Canadian retail Sales are expected to gain 0.5% in March retail after the 0.6% pull-back in February. The ex-autos sales aggregate is seen improving 0.3% in March following the 0.1% dip in February. Gasoline prices dipped 1.1% m/m in March after the 4.9% plunge in February, according to the CPI.

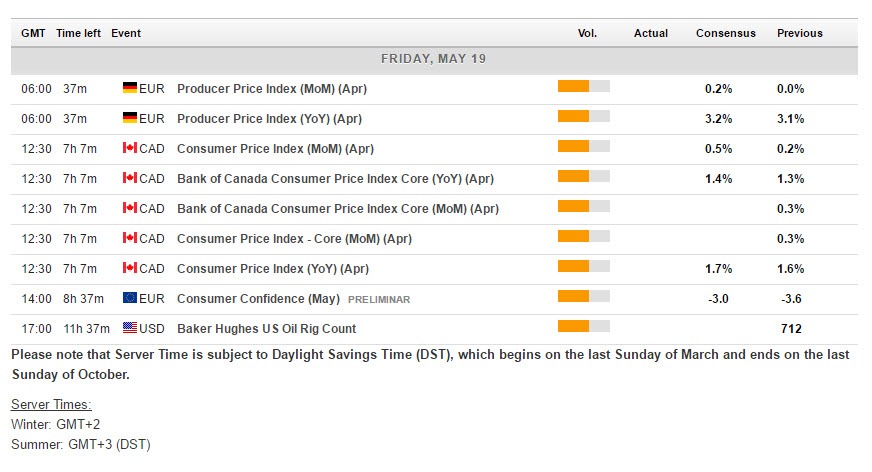

Canada CPI Inflation is expected to expand 0.6% in April versus March after the 0.2% m/m gain in March. Gasoline prices were stronger, shooting 7% higher in April compared to March (average monthly basis). Total CPI is seen accelerating to a 1.8% y/y pace in April from the 1.6% pace in March. The trimmed mean CPI slowed to a 1.4% y/y pace in March from a revised 1.5% rate (was 1.6%) in February. The CPI common grew at a 1.3% y/y rate in March, matching the 1.3% clip in February. The CPI median grew 1.7% y/y following the revised 1.8% (was 1.9%) rate in February.

Author

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, c