Macro Events & News

FX News

European Outlook: The global sell off in equities continued overnight in Asia. Concern over the problems of the Trump administration has been hitting markets hard and Nikkei and ASX lost more than 1%, after a sharp sell off on Wall Street yesterday. Stronger than expected GDP numbers out of Japan failed to lift sentiment. European markets also closed firmly in the red yesterday, with Eurozone peripherals underperforming as risk aversion spiked higher. The FTSE 100 managed to outperform, but also closed with a 0.25% loss and U.K. futures are heading south, even as U.S. futures are managing to move higher. The good news for Draghi and Co is that Eurozone spreads didn’t widen today and that at least so far the spike in risk aversion hasn’t hit peripherals, but increased volatility, will add to the arguments of the doves at the ECB, who want to tread very carefully as the ECB inches towards exit steps. Today’s calendar has French unemployment, U.K. retail sales and the ECB minutes of the last policy meeting.

FX Update: The dollar steadied after posting fresh lows as the “Trump trade” unwind continued after the New York close. The main equity indices in Asia fell, taking their cue from Wall Street amid concerns that the Trump growth agenda is in jeopardy. USDJPY losses extended for a second day. A three-week low was made at 110.52 in early Asia-Pacific dealings, with the pair subsequently managing to settle back above 111.00. EURJPY reversed recent gains as the yen outperformed, dropping quite sharply to a low of 123.42, putting in some distance from the two-year high the cross saw on Tuesday. The drop-in EURJPY reflects yen outperformance as the Japanese safe haven premium rises, while EUR-USD logged a fresh six-month peak amid dollar outperformance. The high was at 1.1171, with the pair subsequently settling in the lower 1.11s.

UK unemployment dipped to a new 12-year low of 4.6%, which was unexpected as the median forecast had been for an unchanged 4.7% reading for official March data. Average incomes were less encouraging, with the ex-bonus figure in the three-months to March ebbing to 2.1% and the with-bonus figure coming in at 2.4%, up from 2.3% in the previous month, but now below inflation, which in the latest numbers for April rose to 2.7% (the March rate had been 2.3% y/y). The BoE said in its quarterly inflation report last week that it expected wage growth to turn positive again, though on the proviso that the Brexit process goes smoothly.

Eurozone April HICP inflation confirmed at 1.9% y/y as expected. The annual rate bounced back in April, after falling to just 1.5% y/y in March, from 2.0% y/y in February. The zigzag course over the March/April period was mainly due to the Easter effect, with the later timing of Easter translating into a dip in holiday related prices in March, which bounced back with the April number. This also impacted core inflation, which rose to 1.2% y/y from 0.7% y/y in the previous month. Inflation is trending higher as growth strengthens, but less than April numbers suggest as wage growth remains moderate, despite the improving situation on the labour market. Wage moderation in Germany in particular seems puzzling given that the German jobless rate is at record lows and with that in mind the ECB is unlikely to do much more than remove the easing bias in June. Indeed, a stronger EUR and lower oil prices could in fact bring a downward revision to inflation projections with the updated forecasts next month.

Main Macro Events Today

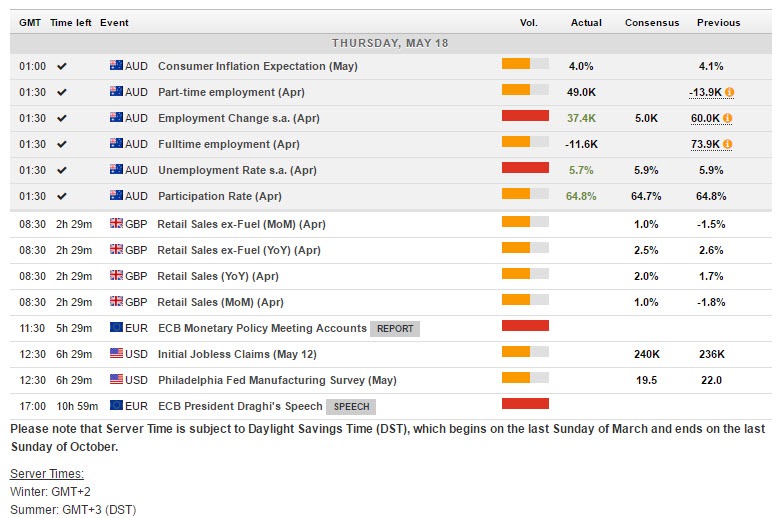

U.K. Retail: Sales Retail sales are seen bouncing 1.0 % after dropping -1.8% in March, while the ex-Fuel figure should rise 1.0% after the disappointing -1.5% previously.

ECB Monetary Meeting Accounts: ECB Monetary Policy Meeting Accounts have be scheduled for 11:30 GMT today, while President Draghi is due to speak at the University of Tel Aviv at 17:00 GMT.

US Unemployment Claims: Initial jobless claims may rebound 4k to 240k for the May 13 week and leading indicators are forecast to rise 0.2% in April vs 0.4% in March.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in