Little Trouble in Big China

The Day So Far…

No I did not misquote the 1986 classic “Big Trouble in little China”, rather I refer to my feelings as to what the news overnight means for financial markets. Moody’s downgraded the sovereign rating of China for the first time since 1989 due to the growing amount of debt being accumulated in order to maintain the current pace of economic growth. Although the local equity markets and AUD fell overnight the currency has since rebounded and the read across into the European open has been muted. To me this news is unsurprising as the China of 1989 compared to the China in 2017 is a starkly different beast and so a change was warranted sooner or later. Secondly, in the context of the other rating agencies the move to Aa3 at Moody’s puts them on par with where Fitch is already and just one notch below S&P, so in reality the downgrade is not massive news.

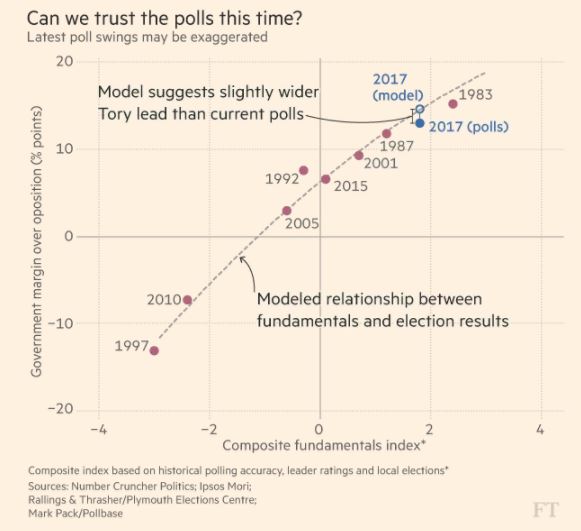

Elsewhere, an interesting statistic I read from the FT this morning is that only once in the last half century have the Tories won a lower share of the vote than the average of final polls suggested. This historic precedence is also in addition to improved poll methodologies since the election in 2015, which now takes into account satisfaction of the party leaders and importantly the performance of the very recent local level elections of which the Conservatives won by a large margin. The net result of this analysis is that despite the polls converging in the last week the likeliest outcome appears to be a Tory lead in the region of the mid-teens.

The Day Ahead…

The Bank of Canada announce their latest interest rate decision and monetary policy report at 1500BST with analysts at Bank of America looking for the Central Bank to hold rates (0.5%) and deliver a neutral statement as growth and inflation diverge. Meanwhile, crude traders will look to the latest DoE crude oil inventory report at 1530BST which follows last nights API data that showed a headline draw of 1.5mln, marking the 7th weekly draw in inventories. Reaction to today’s report could well be muted however as attention starts to turn to Vienna where oil ministers are gathering ahead of the formal talks commencing tomorrow. The latest comments today would suggest a 9-month extension has been approved so with prices firmly above $51/bbl the risk tomorrow would be if this does not materialise or do we simply see a case of ‘buy the rumour sell the fact’ and once the deal gets finalised will some of the fizz from the recent 15% gain in WTI start to fade as US output and compliance issues come back to the forefront of investors minds.

Author

Amplify Trading Team

Amplify

Amplify Trading is a proprietary trading company specialising in the development of new trading talent offering direct experience in financial markets.