Liberation day arrives, the fight back begins

Investors have been waiting for the announcement of Trump’s reciprocal tariffs, and today it will arrive. The President is set to announce the tariff arrangement at 2000 GMT, after US stock markets have closed. European stocks are lower today, however Japan’s Nikkei eked out a gain. US stock market futures are also pointing to a lower open later today. These pre-announcement moves are worth noting, firstly, they suggest that there is hope in markets that clarity about US tariffs will bring stability, hence the rise in the Nikkei. Secondly, US equities are more in the firing line than elsewhere.

Looking at Europe more closely. The Dax is the weakest performer in Europe so far on Wednesday. It is down more than 1%. This may be because Germany has the largest exposure to US tariffs since it has the highest value of trade to the US at EUR 161bn annually. Healthcare stocks are plummeting in the European session on Wednesday. Pharma exports are expected to get hit hard by Trump’s tariffs, and healthcare exports make up one of the biggest categories of exports to the US, along with cars and machinery.

Divergence to emerge within Europe

Can European stocks continue to outperform US stocks in the era of tariffs? In the short term it could depend on how much clarity we get today on the duration of tariffs and if there is room to negotiate. If President Trump does not deliver that clarity, then stock market could plummet. If Trump hints that some countries could negotiate lower rates of tariffs in the future based on the size of their current trade surplus with the US, then we may see some divergence in European shares. For example, the UK has a small trade deficit with the US, so the UK may be more likely to negotiate a lighter tariff package with the US in time, especially compared to Germany. Thus, UK pharma stocks could outperform their European counterparts in the short and medium term.

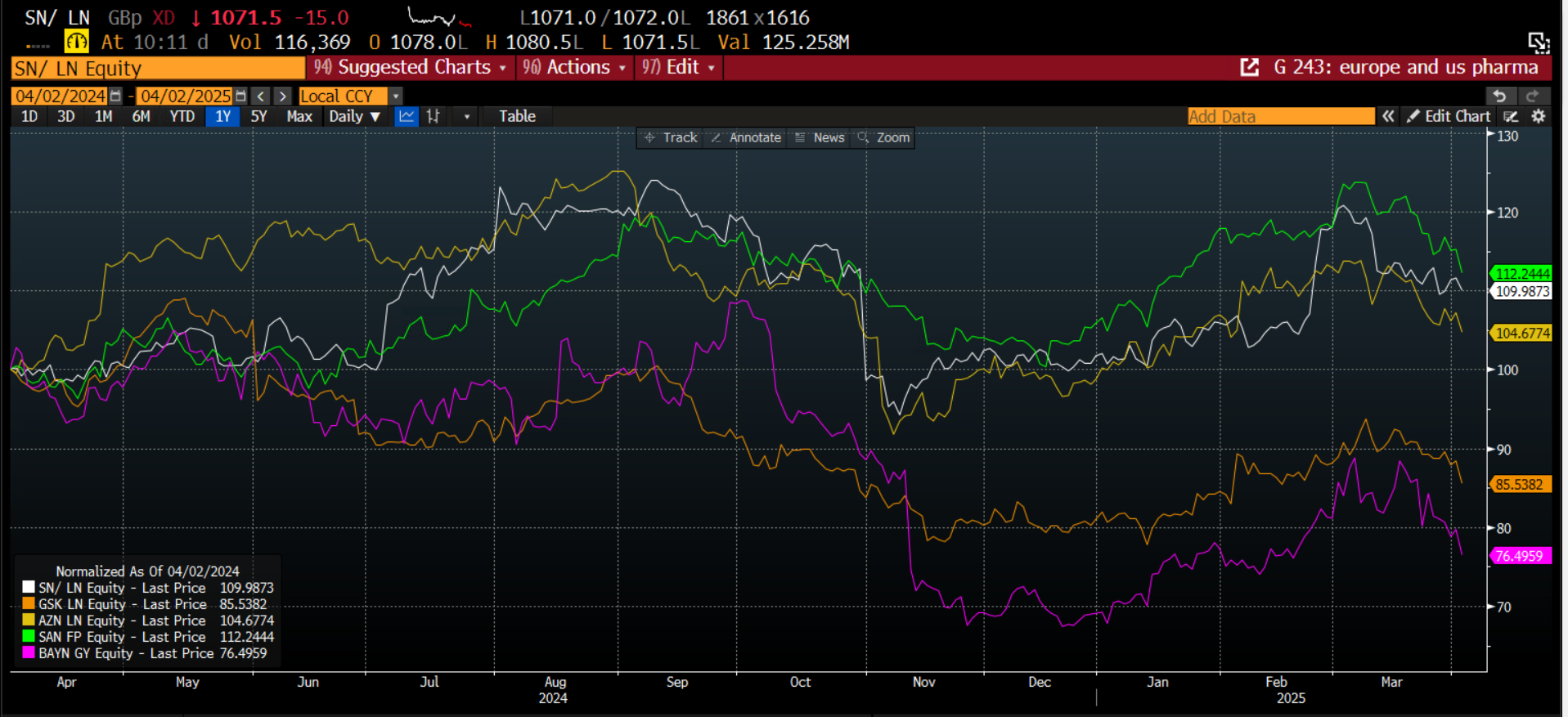

The chart below shows UK pharma giants including Smith and Nephew, GSK and Astra Zeneca, along with European healthcare firms including Sanofi and Bayer. This chart has been normalized to show how they move together over the past year. As you can see, there has been no notable regional dispersion in performance in recent weeks. The weakest pharma companies include GSK and Bayer, although all of the companies in this chart have weakened in March. However, if it starts to look likely that the UK can negotiate a lower tariff rate with the US compared to the EU, then GSK, the UK pharma giant, could be ripe to outperform.

European and UK pharma giants, normalized to show how they move together over the past year

Source: XTB

The fight back begins

Financial markets are also signaling that tariffs may not be as disruptive for global trade as some think. For example, there could be an effective fight back against American protectionism. If all countries that trade with the US face tariffs, some will have tariffs that are higher than others. This means that some countries will have a trade advantage with the US. One of these could be Brazil.

The Ibovespa, the Brazilian stock market, rose by 6.8% last month, compared with a 5% decline for the S&P 500. Likewise, the Brazilian real is higher by 9% YTD vs. the USD, which is another sign that Brazil could be a big winner from President Trump’s tariff policy. For example, the Brazil could have lower tariff rates compared to China. Since it manufacturers some of the same goods, e.g. shoes, if tariff rates are lower in Brazil compared to China, it may protect Brazilian market share in the US. Added to this, Brazil is a commodity heavy economy. If China and the rest of the world turn away from US exports of agricultural products etc., then Brazil could fill the gap.

The outperformance of Brazilian asset prices is a sign of 1, optimism over Brazil’s trade future and 2, a positive sign that just because America is turning inwards, there will still be some winners in the trade war and that should be reflected in the stock market.

Is this a peak for the Gold price?

US durable goods orders are scheduled for release later today; however, the focus is on the tariff update, and we expect financial markets to continue to drift lower until then. Gold has made a fresh intraday record high on Wednesday, which is another sign that gold is the ultimate tariff trade. The gold price will face a big test ahead: if US stock markets start to rally after the tariff announcement is out of the way, can the gold price continue to rally? We think that a lot of the rally in the gold price is linked to US economic policy uncertainty, once this starts to recede, the gold price could follow.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.