Land-Line vs. Cell Phones: A U.S. Consumer View

Executive Summary

Once upon a time there was a very boring thing called the land-line telephone with about one rotary telephone per household. Then, land-line telephone services prices started to go down while incomes continued to rise and U.S. consumers started to buy more than one telephone per household, perhaps helped by the growing influence and the coming of age of the Baby Boom generation. After that, telephone consumption by households became a bit more interesting as households got the touch-tone phone, call waiting, then caller I.D., etc. When consumers started to get excited about the changes in the land-line telephone, the market transformed radically with the introduction of the cellular telephone and then with the introduction of the Internet and the smart phone. Since then, the consumer market for telephones has never looked back. The rest is history: a good history for cellular telephone consumption and a not so bright history for land-line telephone consumption.

In this report we take a look at what has happened over the last several decades to personal consumption expenditures (PCE) of land-line telephone service and cellular telephone service from the perspective of the U.S. consumer. Our conclusion is that land-line telephone services consumption is bound to get close to zero or to hit a lower bound that may not be much different from zero, especially if the industry can keep the bundling strategy together. However, while older generations may be enticed by the bundling strategy from the industry, it is not clear that newer generations may have the same predisposition to this strategy.1

Furthermore, consumers that hold to their land-line telephone services seem to accept, at least for now, paying more and more for land-line telephone services, for both local calls as well as longdistance calls as reflected by the ever increasing price for those two services while the price for cellular phone services has continued to decline. However, the downward trend for the consumption of land-line telephone services does not augur a promising future for that strategy. At the same time, we point to statistical relationships that tend to point to price sensibilities that have made possible such pricing strategies.

Some Americans are Still Holding Tight to Their Land-Lines2

The telephone communication industry has seen an impressive transformation over the last several decades with consumers massively picking to use a cellular phone instead of the more "traditional" land-line telephone, according to a view from analyzing PCE data. In this report we look at the consumption of land-line and cellular telephone services over time by analyzing data from personal consumption expenditures. That is, we look at demand for cellular and land-line telephone services from the consumer point of view and will not attempt to untangle or even attempt to propose changes in industry strategy of any kind. Having said this, we may, at different points in the report, infer some already known and heavily researched facts regarding the trends in the telephone industry.

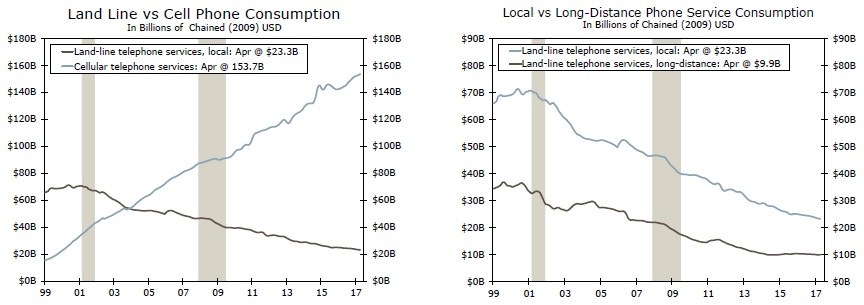

By looking at telephone service consumption from PCE data, both from land-lines as well as cellular telephone services, it is clear that traditional land-line telephone service consumption continues to unravel. That is, according to data from PCE over the last several decades' consumers continue to shun land-line telephone services in favor of cellular telephone services at a pace that, if sustained into the future, would imply that consumers will stop consuming land-line telephone services during the next several decades.

It is possible, however, that land-line consumption levels probably have a lower bound (see Footnote 1), that is, they may never go to zero, but this lower bound is probably very low and is probably a consequence of some of the characteristics of today's consumption of land-line telephone services. One of these characteristics is the fact that many homes across the country are also used as businesses and households may keep their land line so they are able to send/receive faxes or use the land-line telephones as office phones for their home business. However, if those land-lines used for business purposes are reported as only business expenditures, then those land-lines will not be included in the PCE data. If consumers, on the other hand, report their land line usage as 50 percent for personal use and 50 percent (or a different combination between them) for business purposes, then 50 percent of this consumption of land-line telephone services corresponds to PCE land-line services consumption.

It is also possible that the "bundling" strategy by the cable industry may have slowed down the downward path or the "demise" of land-line telephone service consumption. However, the longterm trend continues to be that of a slow and protracted disappearance of land-line telephone service consumption (see Figure 1 above). It may also be the case that Americans are holding to land-line telephone services so they can make long-distance calls, as real consumption of long-distance services by land-line telephone holders is low but has stabilized during the last several years (see Figure 2 above).

Portability and Functionality of Cell Phones versus Land-Lines

Perhaps one of the most important characteristics of the early-days' cellular telephone versus a land-line telephone was the former's portability. However, as cellular phone technology advanced it became clear that another, perhaps even more important characteristic, was the irruption of the Internet and the introduction of the smart-phone a little more than 20 years ago. Looking back, the history of the smart phone probably had different paths in two different markets. For the business community, smart phone usage took off after the introduction of the BlackBerry in 2003, which made business e-mail and some internet connectivity accessible for business purposes.3 However, for the personal consumer/household market the product that pushed the smart phones into the mainstream was the launch of the iPhone in 2007.4 Today, these different paths are not as clear cut as they used to be as any original differences between business and personal/household use of smart phones seems to have been blurred by the evolution of the smart phone and the increasingly similar needs among business people and personal/household customers. That is, what were very different markets at the beginning of this century has given way to strategies that include BYOD (Bring your own device) policies within the business community.

However, the PCE data that we are using to look at the land-line telephone service versus cellular telephone service usage only include phone usage for personal/household usage. Having said this, it is probably almost impossible today to be sure that the PCE data used here do not include some part of business telephone usage, especially in the cellular telephone consumption market side as many firms, as we said before, have been moving to some type of BYOD system by which workers use their personal cellular telephones for conducting business and in many cases do not get reimbursed by the firms for the partial use of those personal cellular telephones.

Who Needs (Costly) Land-Line Telephone Services Anyway?5

This is, perhaps, the question many firms that market and sell land-line telephone services asked themselves when cellular telephone service and internet consumption started to outpace land-line telephone service consumption. And the answer was probably the following: very few, which meant that selling land-line telephone services wasn't going to be a good business anymore. However, with the advent of the Internet and help from very fluid mergers and acquisitions the industry has been transformed to one that sells not only land-line telephone services but also internet services, cable TV services, etc. The addition of these services has allowed the industry to continue to sell land-line telephone services by, as we argued above, "bundling" telephone services with the other services together so customers can get a "better price," i.e., lower price for the other services, but especially for internet access.

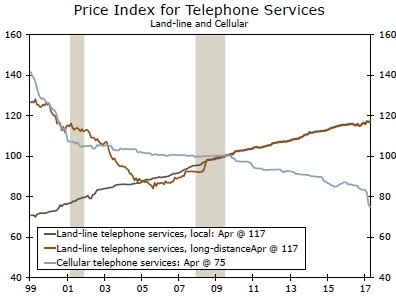

Furthermore, this strategy has also allowed these companies to use a very different price strategy than the one being used by companies that sell cellular telephone services (see Figure 3 above). That is, this strategy has allowed them to keep increasing prices for land-line telephone services, on both local as well as long-distance service charges, compared to what has happened to services sold by companies that sell cellular telephone services. That is, our analysis confirms that there is more competition for cellular telephone services than for land-line telephone services, which is probably a consequence of the bundling strategy followed by land-line telephone service providers.

Thus, although consumption of land-line telephone services has continued to decline, it seems that the bundling strategy has been working for these companies as they have continued to increase prices on those services. That is, prices for land-line telephone services have been going up unabated over the last several decades and this has helped to prevent expenditures from landland telephone services, both local charges as well as long-distance charges, from completely collapsing.

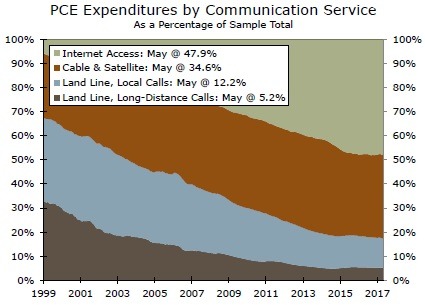

The changes that have occurred during the last several decades in this industry are impressive, with the largest component of expenditures generated by PCE consumption of these services coming from the consumption of internet access (almost 50 percent versus less than 10 percent in 1999). Cable & satellite services come in second, with about 35 percent, and then domestic calls services charges (12 percent versus more than 35 percent in 1999) and land-line long distance services charges (only about 5 percent versus a bit more than 30 percent in 1999), figure 5.

However, at this rate, as we said before, the durable life of land-line telephones is in peril. Furthermore, how much more can consumers continue to experience land-line telephone services price increases without reacting more forcefully and quitting these services altogether? Perhaps customers know that this is the "cost" to pay for having internet services and they accept it as it. However, our guess is that there is a younger generation that doesn't care for land-line telephone services and once they become the majority then land-line telephone services will disappear.

Thus, if land-line telephone consumption finally goes to zero in the not-so-distant future then this pricing strategy will have to change very fast, with customers experiencing a transition period in which internet access prices (or other services prices like cable TV services) will probably need to increase so that these companies can recapture revenues lost by not being able to charge for landline telephone services consumption, both domestic and long-distance.

Once again, we are not telephone industry analysts so we leave the alternative scenarios of how any transitions may happen to those that know. We are only looking at the industry indirectly by using personal consumption expenditure data over time and although the picture does not look good for companies selling land-line telephone services, the alternatives these companies may need to use to adapt to the new consumer scenario may be easier and much simpler than what it is implied by just looking at PCE data.

That is, the merger and acquisition process that continues to occur within this industry and between this industry and other, highly interrelated industries is a clear example of how these companies are preparing for, what today seems to be, the probably inevitable disappearance of consumption of land-line telephone service.

Econometric Results and Conclusions6

In order to look at some of the statistical relationships between these different services and try to make sense of what has been happening from the consumer side, we ran several regression equations on land-line as well as cellular telephone consumption. The results shed some light on some of the characteristics of the consumption market for these services.

Our econometric results show that land-line telephone services consumption is slightly responsive to its own price and has the correct sign, i.e., if there is an increase in price for the land-line telephone service then the quantity demanded of land-line telephone services declines. However, this responsiveness is very low; in economic parlance, land-line telephone services consumption is highly inelastic. This could explain why land-line telephone services prices have continued to go up over the years and quantity consumed of land-line telephone services has gone down but at a very slow pace. At the same time, this low sensitivity to price increases gives some credence to the ever-increasing price strategy implemented by the industry over the last several years and supports the bundling strategy chosen.

Meanwhile, although cellular telephone services consumption is also not very responsive to price changes, it is more responsive to increases in cellular telephone services prices than land-line telephone services. Furthermore, land-line local telephone services consumption is not responsive to the price of cellular phone services, according to our econometric results. At the same time, land-line telephone service consumption is not responsive to the price of cable TV services and/or to the price of internet access services. We measured this relationship just to confirm the relationship between land-line telephone services and cable TV and internet access services as part of the bundling strategy by land-line telephone service firms.

However, we found that consumption of cellular telephone services is somewhat responsive to the price of internet access services. That is, the higher the price of internet access services the lower the demand for cellular telephone services consumption. This is intuitively appealing for a consumer concerned with keeping their cellular telephone bill in check. It is also a very appealing characteristic for an industry that, until recently, charged more for more usage of the cellular telephone capabilities in terms of bandwidth.

All these results point to a very dismal future for land-line telephone consumption. The fact that the price of land-line telephone services continue to increase implies that, in the long run, telephone service consumption will likely approach zero. Having said this, we indicated that this may not be completely true if some of the characteristics of the market remain as effective as they are today, i.e. bundling. That is, we understand that consumption of land-line telephone services may have a lower bound that may differ from zero.

We did not measure, however, the effect of the new generations in terms of their attitude against the land-line telephone consumption, i.e., the attitudes of millennials for land-line telephone services consumption. The truth is that the new generations don't seem to need land-line telephones because cellular telephones and the Internet provide all of the needs for their generation. Thus, even if there is a lower bound for the consumption of land-line telephone services, and this lower bound is different from zero, generational characteristics may push consumption of land-line below that lower bound created by the industry with the bundling strategy. Again, we did not control for this variable but we think that it is an important aspect and difference between previous generations and the current ones.

Author

Wells Fargo Research Team

Wells Fargo