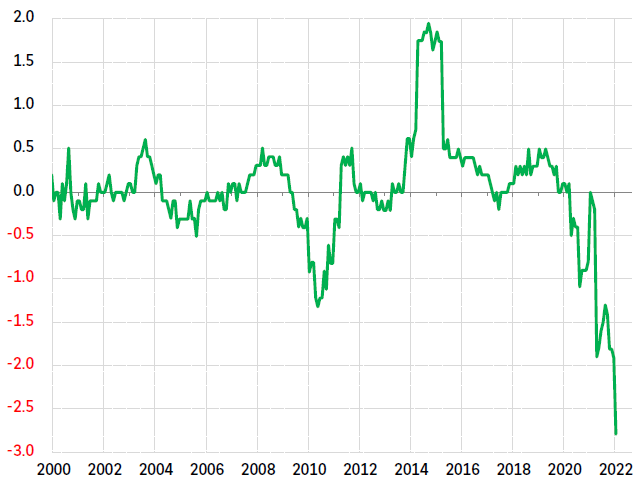

Japan: Deflation intensifies in the services sector

In Japan, possibly more than anywhere else, it is important to distinguish the dynamics between headline and core inflation. Headline inflation – at 0.5% in January – is bound to rise further, led by higher energy prices. By contrast, core inflation is still deeply in deflationary territory, and this trend is amplifying. Excluding perishable food products and energy, the consumer price index (CPI) declined by 1.2% year-on-year in January, the biggest decline since March 2011. The services sector even has reported the strongest deflation since 1970 (-2,8%), mainly due to the sharp drop in mobile phone charges, down more than 50% since March 2021. Medical services were also down (-0.8% y/y), as was durable household goods (-3,0% y/y), and leisure goods (-1.1% y/y).

Even so, the Japanese economy has not been spared an upturn in long-term rates: 10-year JGB yields are now close to the upper range of 0.25% set by the Bank of Japan (BoJ). On February 10th, the central bank has strengthened its policy levers by announcing unlimited purchases of 10-year bonds, if necessary, at a fixed rate of 0.25%1. Unlike the other central banks of the developed countries, which are beginning to normalise monetary policy to counter much higher inflationary pressures, the decline in service prices gives the BoJ more leeway to pursue its accommodating monetary policy.

Japan: Consumer price index in the services sector (y/y % change)

Source: Statistics Bureau of Japan, BNP Paribas

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.