Japan: Consumer spending is suffering

The Japanese economy ended 2019 on a negative note.

As has happened before, consumer spending was hit by the VAT hike introduced in October.

Typhoon Hagibis also put a significant dent in domestic demand, particularly in the area of private sector business investment.

The start of 2020 looks difficult given the Coronavirus outbreak and the close economic relations between Japan and China.

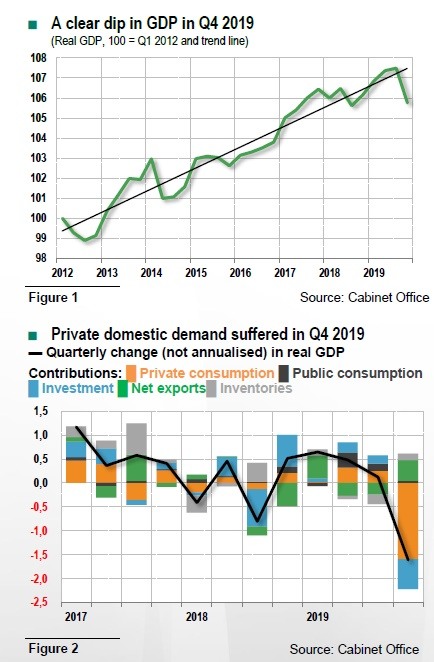

Japan experienced a sharp contraction in GDP in the fourth quarter of 2019 (Figures 1 and 2). GDP fell by -1.6% (quarteron- quarter, non-annualised), its biggest contraction since the - 1.9% fall in the second quarter of 2014. This poor performance was due to falling private domestic demand. Consumer spending was hit particularly hard. Over the year as a whole, the Japanese economy grew by 0.7%.

Collapse in private consumption, significant weakness in business investment

The Japanese economy suffered from two sizeable shocks in the final quarter of 2019.

First, having delayed its implementation, the authorities decided at last to increase VAT from 8% to 10% in October 2019. This was the 3rd increase since the tax was introduced (1997, 2014 and now 2019). The last time the rate was raised, Japanese consumers significantly reduced their spending. The fall in private consumption of around 3% (q/q) in the 4th quarter of 2019 is less than the 4.8% contraction in Q2 2014 when VAT was raised from 5% to 8%.

The fourth quarter was also affected by a typhoon which did significant damage to domestic demand. Against this background, private non-residential investment fell by nearly 4% (q/q) in Q4 2019 relative to Q3. A quiet decent growth of public sector investment came nowhere near offsetting the drop in investment by private companies.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.