1% rate, 160 Yen: Why Japan’s historic hike changed little

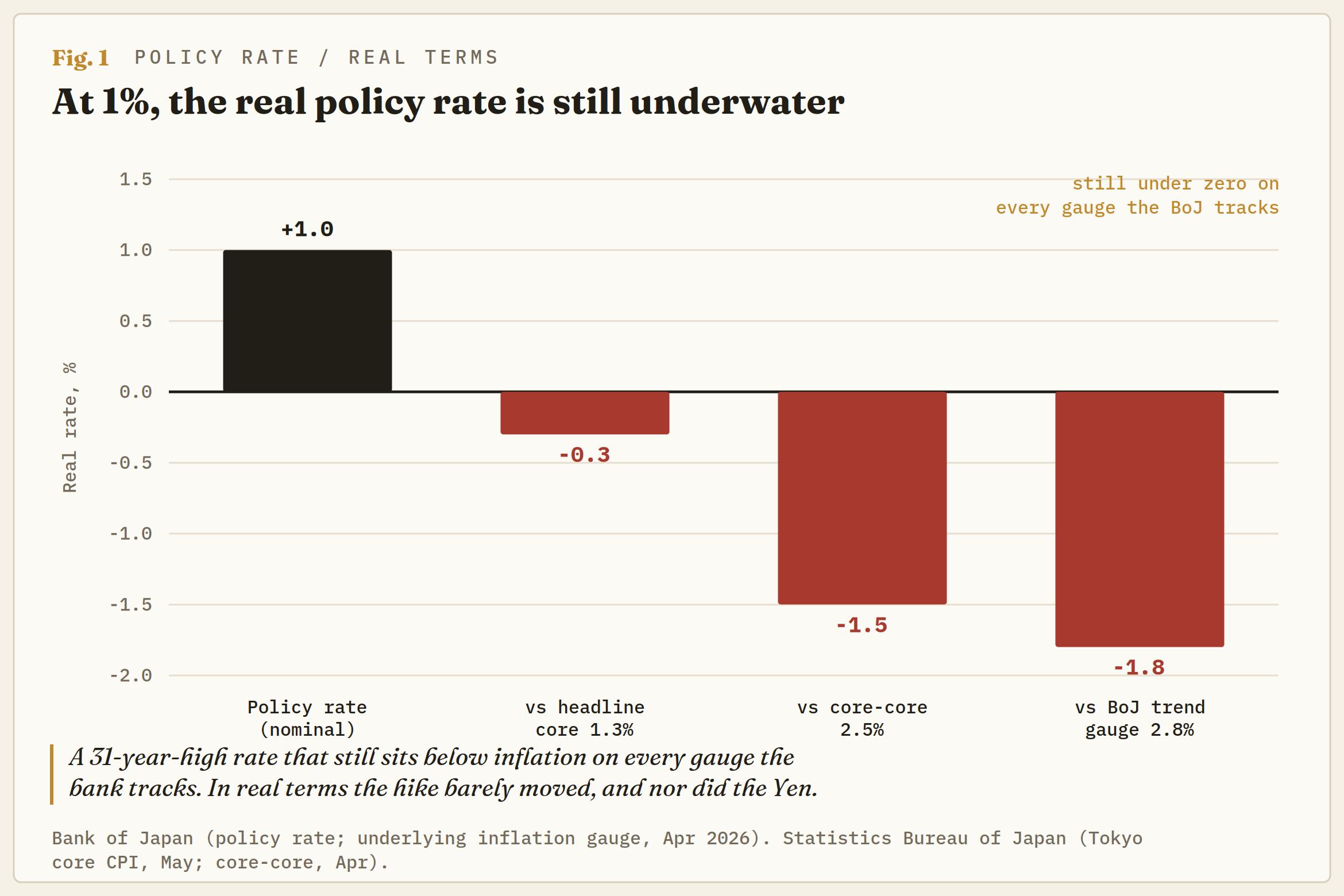

The Bank of Japan (BoJ) pushed its short-term policy rate to 1% on Tuesday, the highest setting since 1995 and a 31-year milestone in a normalization cycle barely two years old. It is the kind of number that should mark a turning point for the Yen, and it did almost nothing. USD/JPY held just above 160.00, because the figure that moves currencies is the real rate, not the nominal one; in real terms, the hike barely registered.

Strip out the headline, and a more awkward truth shows up: the bank tightened into falling consumer prices, justified the move on an inflation gauge the market cannot trade, and still left Japanese real yields underwater. The question is not whether 1% rescues the Yen. It is whether a rate that is negative in real terms can rescue anything.

A hawkish hike into a falling headline

The decision itself surprised no one; markets had it fully priced. What should give traders pause is the backdrop the board chose to tighten into. Tokyo's core Consumer Price Index (CPI), the timely gauge that leads the national series, rose just 1.3% in the year to May, a fourth straight month below the 2% target and still slowing. The BoJ raised rates anyway, on a 7-1 vote, with Toichiro Asada dissenting in favour of a hold and Prime Minister Sanae Takaichi, no friend of higher borrowing costs, opposing from the sidelines.

The justification was underlying pressure rather than the headline: officials flagged the risk of trend inflation running above target, nudged up their price outlook for the fiscal year even as they trimmed growth, and left the Japanese government bond (JGB) taper intact, slowing purchases by around 200 billion Yen a quarter into early 2027. A central bank hiking over its own government, against a softening headline, on the strength of a number most of the market does not watch. That tension is the whole story.

The real rate that didn't move

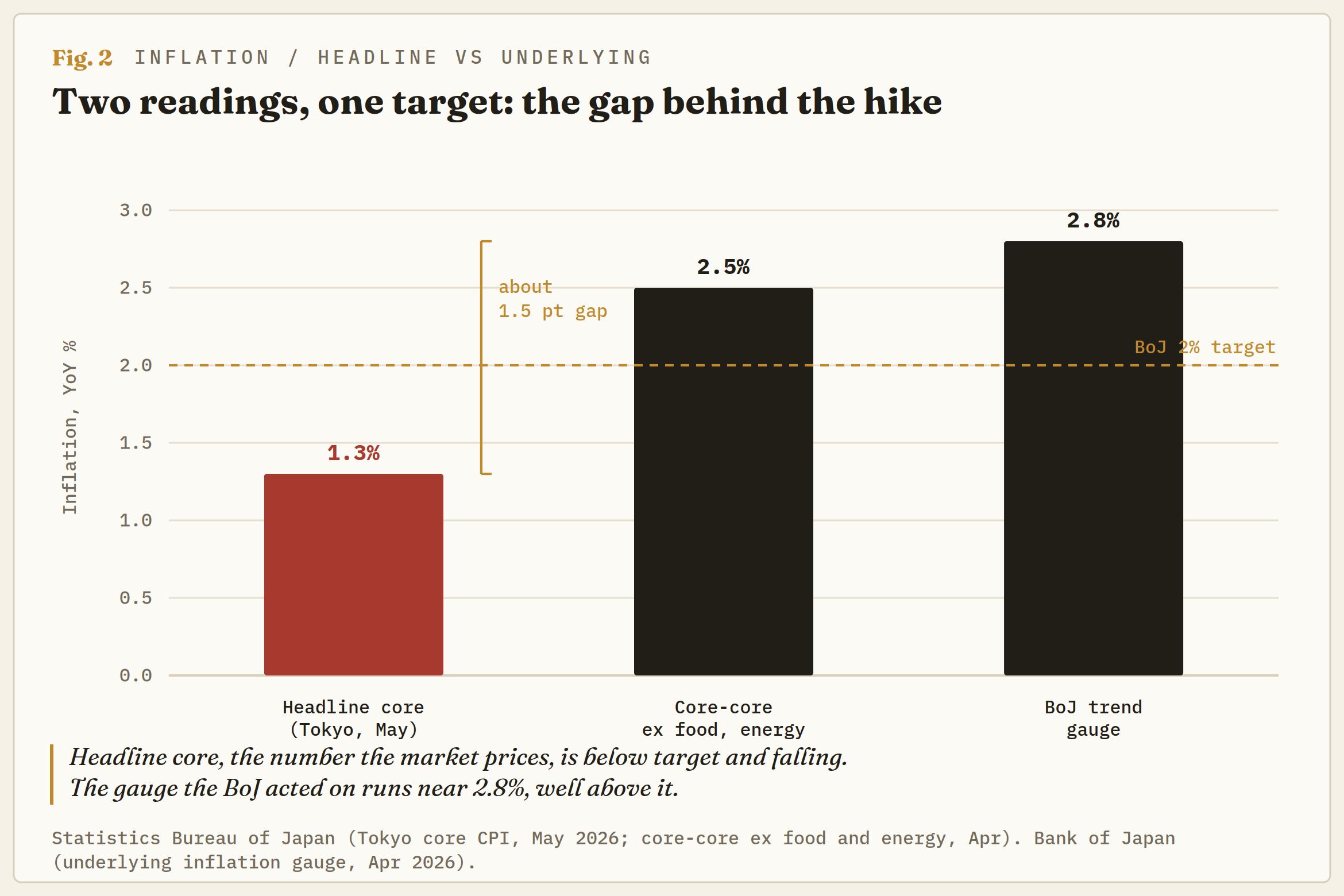

Here is the part the wires skated over. There are effectively two inflation readings in Japan right now, and they point in opposite directions. The headline core sits at 1.3%, dragged down by Takaichi's energy price controls, falling crude, and softer food and rice prices. The BoJ's own trend gauge, built to see through subsidies and temporary distortions, has accelerated to 2.8%, and core-core inflation, stripping both food and energy, runs near 2.5%.

Which one you use decides whether Tuesday meant anything. Put the new 1% rate against the headline, and the real rate is roughly -0.4%. Against core-core, it is about -1.5%. Against the BoJ's preferred trend gauge, it is close to -1.8%.

On no underlying measure did the hike turn Japanese real yields positive. Set that beside a US real policy rate that is firmly positive, with the Federal Reserve (Fed) holding 3.50%-3.75% against cooling inflation, and the real differential, the thing that actually anchors a currency over time, scarcely moved on Tuesday.

That is why the Yen sat still. It also points to the one signal worth watching on the data side: the Yen earns a real bid the day the headline starts converging up toward core-core, when the subsidies lapse and the Crude Oil base effects flip, and the BoJ's hand is finally forced. Until then, 160 is sticky by design, not by accident.

The wage round that never reaches wallets

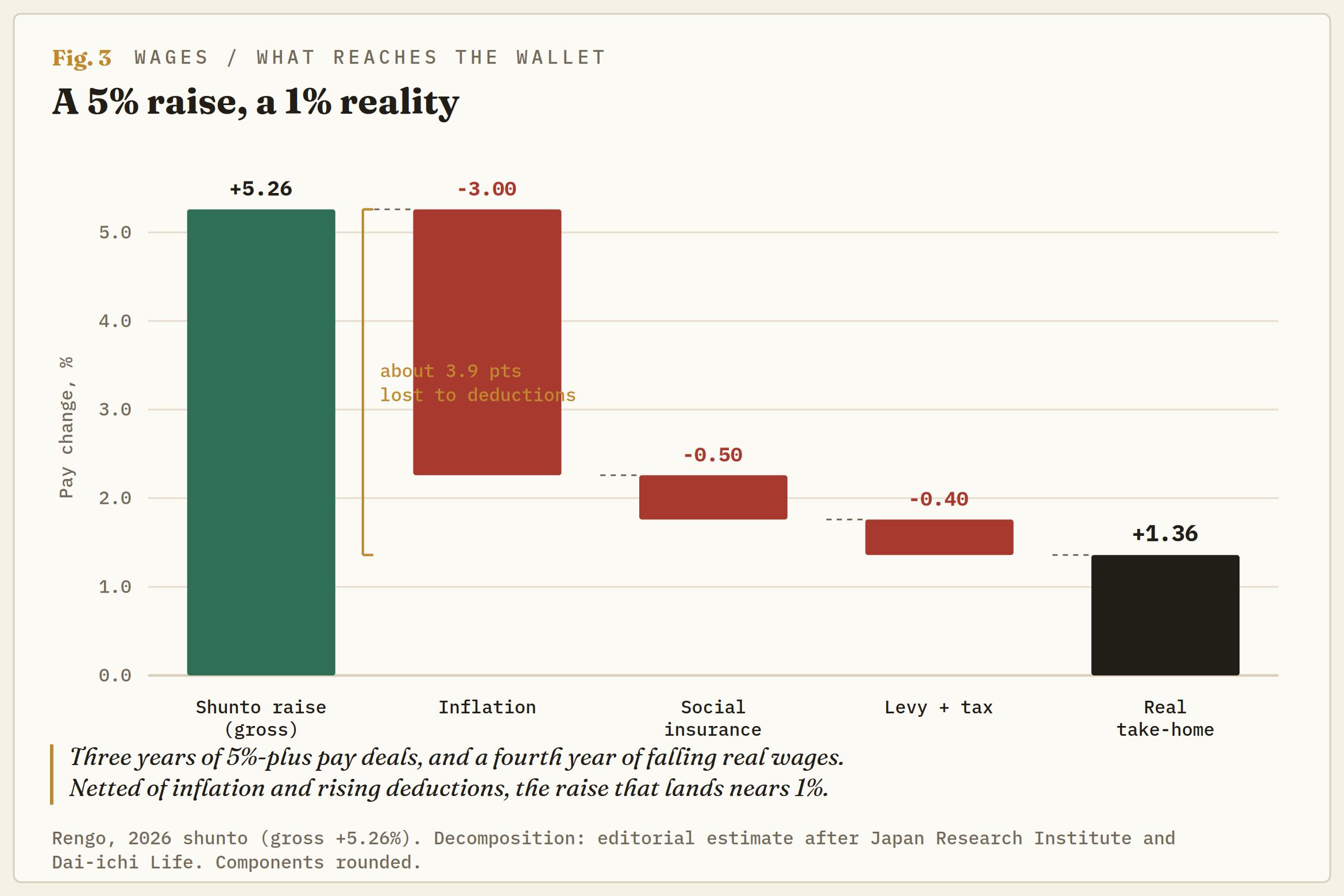

The bull case for a Yen recovery leans hard on wages, and on paper, it looks unanswerable. This spring's Shunto negotiations delivered an average pay rise of 5.26%, a third straight year above 5%, on the heels of a 2025 settlement that was the largest in 34 years.

The trouble is what survives contact with a payslip. Real wages have now fallen for a fourth consecutive year, and even this year's 5.26% shrinks on the way to a payslip. Inflation eats roughly three percentage points of it, with higher social insurance, a new childcare levy and tax taking more, leaving real take-home growth barely above 1%, and that only for the fewer than two in ten workers inside the union framework.

A wage-price cycle that does not reach household spending cannot sustain the run of hikes the Yen would need to close the gap. The strongest number in the bull case is hollow where it counts.

Tokyo already spent big, and 160 held anyway

The fallback for Yen bulls is the Ministry of Finance (MoF), and that is no surer a bet. Tokyo disclosed that it spent roughly 11.73 trillion Yen, about $73 billion, defending the currency between late April and late May, its heaviest stretch of yen-buying in years and on some measures the largest since 2004.

The move pushed the pair lower, but the Yen is right back at 160. Currency chief Atsushi Mimura and Finance Minister Satsuki Katayama have leaned on verbal warnings for weeks, citing speculation in both the Oil and currency markets, but the market now fades the rhetoric and prices only the actual bid.

Japan moves against disorder and speed, not against a level, which is why a slow drift to 160 draws words while a violent spike draws the desk. The reserves are deep, near $1.2 trillion, but they are financed by selling US Treasuries; they are finite, and each round is a harder sell in a cabinet that never wanted the hike. History is the warning: the heavy 2024 intervention shifted the pair for days, not weeks, and what actually turned the Yen that summer was a carry-trade unwind on US growth fears, not Tokyo's money.

The Oil tailwind is rolling over

The timing only sharpens the bind. The case for hiking leaned on imported inflation, with Brent and WTI pushed up by the Strait of Hormuz crisis. That prop is sliding. A US-Iran deal struck over the weekend, and the prospect of Hormuz reopening have knocked Crude Oil back toward the low $80s.

Cheaper energy cuts two ways for the Yen. It trims Japan's import bill, a slow positive, but it also deepens the drag on the headline, widening the gap to underlying inflation and weakening the case for the next hike. The BoJ tightened into an inflation peak it may already be past, and the data flow from here is more likely to argue for patience than for pace.

The lean

For levels, 160.00 is the line in the sand, both the psychological handle and the zone Tokyo has shown it will defend with real money. Above it, the cycle highs near 161.00 are the barrier, and a clean break toward 162.00 is the fast, one-sided move that brings the MoF off the bench.

On the downside, 158.00 is the first shelf, with 155.00 the next if the Fed leans dovish on Wednesday or Oil keeps bleeding. The bigger Yen catalyst this week is the Fed and its dot plot, not the hike already in the book.

The tape sits with the bears on the Yen near-term: The bid is intact above 160.00 while the real gap stays this wide, and the lean is to fade Yen strength back toward 158.00 unless Warsh surprises dovish or Tokyo steps in. This is a range propped up by reserves and a negative real rate, not a trend the BoJ has earned the right to reverse, and the risk-reward stays skewed toward more of the same.

The 1% handle is real on paper and hollow in real terms, and the contradictions stack up from there. A government suppressing the headline with subsidies while opposing the hike that the print supposedly justified. A wage round that reads historic and lands negative. A central bank tightening on a gauge its own market cannot price. The milestone buys the BoJ a measure of credibility it has chased for two years.

What it does not buy, on Tuesday's evidence, is a stronger Yen. That still rests with the Fed, Oil prices, the day Tokyo's subsidies lapse, and with the MoF's appetite for writing very large cheques. 160.00 is holding, and nobody in Tokyo looks comfortable about how.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.