January Retail Sales suggest some lost momentum

Summary

The broad-based drop in January retail sales suggests the consumer lost some momentum at the start of the year. Yet, a strong gain in food services sales implies services consumption remains sturdy and likely offset some weakness in goods consumption.

A weak start

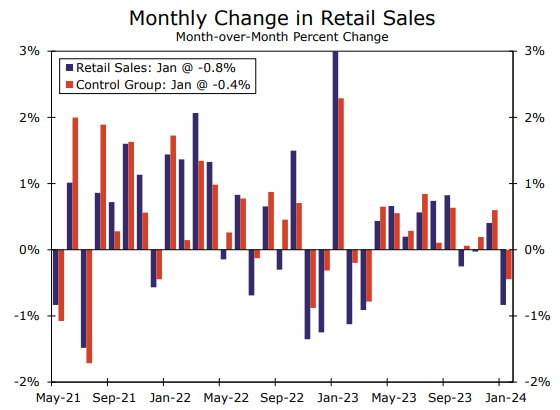

Retail sales started the year with a dud. Overall sales slipped 0.8% in January, and even when excluding the typically-volatile components or the expected weakness from autos, all cuts of this data were down (chart). Excluding autos, sales slipped 0.6%, and the allimportant “control group” figure, which feeds into the Bureau of Economic Analysis (BEA) calculation of GDP, declined 0.4%. In some ways, a weak January is expected and can be chalked up to seasonal behavior coming off the holidays at the end of last year. But the Census Bureau adjusts the data for these seasonal effects, a process that typically boosts January sales, which implies unadjusted sales were even weaker last month.

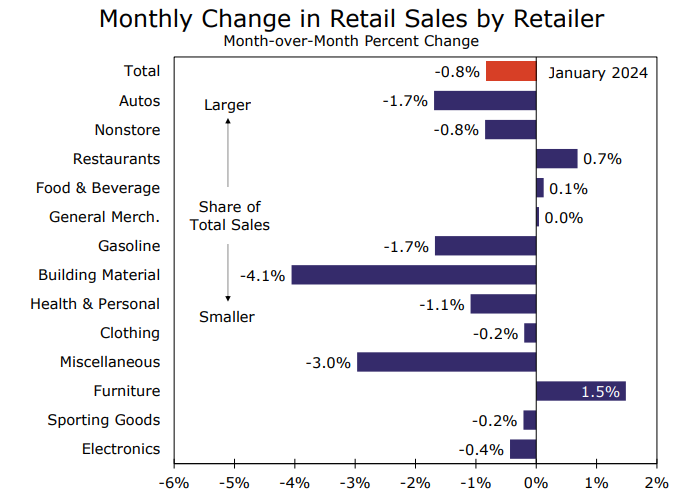

Weak spending was broad based across retailers (chart). The largest decline was at building material & garden stores, where sales slipped 4.1% during the month. Miscellaneous retailers saw sales drop 3.0%, and both auto dealers and gasoline stations sales were off by 1.7%. Furniture store sales leaped 1.5% during the month, but after considering that sales slipped in nine of the 12 months of 2023, this bounce is less exciting.

The one area of strength that stands out to us is the 0.7% gain in sales at food services & drinking places. This is the lone services' category in this release, suggesting service-sector activity held up well at the start of the year. Like control group sales, it also feeds directly into the BEA's calculation of personal spending in the GDP accounts. We'll get a more comprehensive look at January services spending in the personal income & spending report later this month and expect it held up better than the retail side of spending.

The data suggest the consumer lost momentum at the start of the year. On a year-ago basis, control group sales growth slipped to 2.4%, which is the slowest gain since April 2020, when the economy was in the depths of the pandemic. Even as we expect spending will moderate this year, the January slowdown may overstate the near-term pull back in consumption. Households have benefited from a real income tailwind over the past year as inflation is slowing more than wage growth. While the unique factors of excess liquidity and easy access to cheap credit are tales of the past in the story of consumption, a still-sturdy labor market should lead to only a gradual moderation, rather than collapse in spending this year.

Consumer resilience is positive in the sense that it helps ward off economic contraction but could be problematic if it gets in the way of the downtrend in consumer inflation. This week's inflation data showed the consumer price index (CPI) came in hotter than expected, with the core CPI up 0.4% during the month. The data did little to give the FOMC the “greater confidence” it needs to start imminently cutting rates, but the final mile in getting inflation back to the 2% target is expected to be bumpy. How consumer demand evolves will play a key role in continued disinflation and the pullback in January sales suggests some lost momentum.

Author

Wells Fargo Research Team

Wells Fargo