January personal income and spending: Signs of resilience beneath volatility

/stock-market-graph-and-office-work-gm538992537-58716016.jpg)

Summary

Real personal spending shot higher in January, and solid growth in discretionary services suggests continued consumer resilience. A clean read on January income is tough; while a jump in wages is supportive of spending, it's a challenge for the Fed if it keeps the heat on inflation. The core PCE deflator rose by the most in six months.

Keep an eye on discretionary services

Since June 2022, we have kept tabs on the uncanny staying power of consumer spending while still warning of an eventual retrenchment. Real consumer income fell in each of the first six months of 2022, but amid a tight labor market and receding inflation, real income was positive in the final six months of the year. Remarkably, real consumer spending held up reasonably well throughout most of 2022; though things were deteriorating as the year came to a close.

A draw-down of excess savings along with increased consumer credit were key factors that allowed real consumer spending to grow even as inflation outpaced income early on in the year. Real spending never posted an outright decline until November, but then fell again in December.

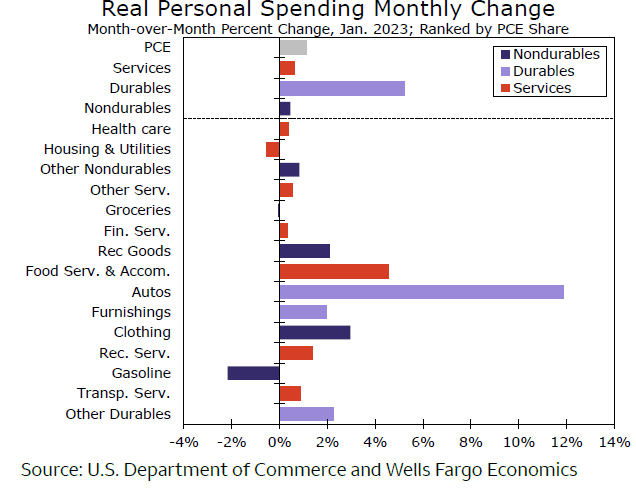

Real personal spending got a lift again to start the year, and in jumping 1.1% in January, growth more than offset weakness at year-end (chart). A blow-out January retail sales report pointed to scope for a rebound to start the year at least in terms of goods outlays. To that end, real goods spending rose 2.2%, due mostly to a 5.2% surge in durable goods spending specifically. Durables were lifted by a jump in auto purchases, but the other major categories like furnishings and recreational goods also posted sizable gains. But we anticipate durables strength is due more to monthly volatility than a renewed interest in goods outlays by consumers.

Today's personal income and spending report also includes spending details on the much larger services category. Spending was strong here too, rising 0.6%, which marks the fastest pace of growth in nearly a year. With services consumption led by discretionary spending categories like food services & accommodations (+4.6%), recreation services (+1.4%) and transportation services (+0.9%), the uptick in consumption suggests households continue to spend at a relatively decent clip.

Author

Wells Fargo Research Team

Wells Fargo