Janet Yellen's comments spooked traders

Morning notes

-

Kaplan adding to Friday’s hawkish comments yesterday. He said "I think it will make sense to at least start discussing how we would go about adjusting these purchases and start having those discussions sooner rather than later".

-

The market had also taken some comments from Yellen as hawkish when she said “It may be that interest rates will have to rise somewhat to make sure that our economy doesn’t overheat, even though the additional spending is relatively small relative to the size of the economy,”. She later clarified that higher rates were “not something I’m predicting or recommending”.

-

Alberta Canada has implemented stricter virus controls to contain surging covid cases. Stricter measures include confining schools to online learning, ordering workplaces with COVID-19 outbreaks to close for 10 days, closing salons, allowing restaurants to offer takeout service only and reducing the number of people allowed at funerals and religious services. On the bright side Canada has administered at least 1 dose to 35% of the population.

-

Singapore also enacted stricter measures to contain a recent outbreak.

-

Australia March Building Approvals jumped 17.4% vs 3% expected. This comes after a relatively dovish RBA yesterday where they said that a decision will be made on whether to move to targeting the Nov 24 bond for YCC at the July meeting. This is earlier than the August meeting that was expected.

-

New Zealand employment numbers were strong this morning. Participation picking up but the unemployment rate still falling to 4.7% vs 4.9% exp. RBNZ financial stability report noted that they are watching how housing market responds to recent policy changes and if required they will tighten lending conditions further using LVR requirements.

-

BoE Thursday. No changes to policy expected, just some upward revisions to growth forecasts.

-

Little bit of risk off feeding into quiet markets yesterday. Driven mostly by lower US tech stocks. The “sell in May and go away” line may add momentum to any move lower as it becomes self-fulfilling.

-

Feels we may be due a larger bout of risk aversion after such a strong run in asset prices last month. Outside of the US the virus picture has been deteriorating in Canada and Asia, and it is a little surprising that tighter restrictions in Canada, Japan, Taiwan, Singapore, Thailand and India have not fed into Global risk sentiment.

-

Leaning towards being long USD both from a view of US outperformance given the vaccine roll out there and any safe haven USD demand. CAD stays well supported despite tighter restrictions in Canada, helped by higher oil, being short CADJPY against 89.18 high and long USDCAD against 1.2266 low good risk reward trades.

-

VIX volatility index edging back up towards the psychological 20 level. A break through there this week is likely to feed into negative risk sentiment and drive selling in risk proxies such as AUDJPY.

-

Short GBPUSD where the seasonality is particularly strong as well as the added downside risk coming from SNP’s plans for a Scottish Independence Referendum if they win on Thursday as expected. The market is long GBP so there is room for any sell off to build momentum.

Our forecasts on currencies and indices

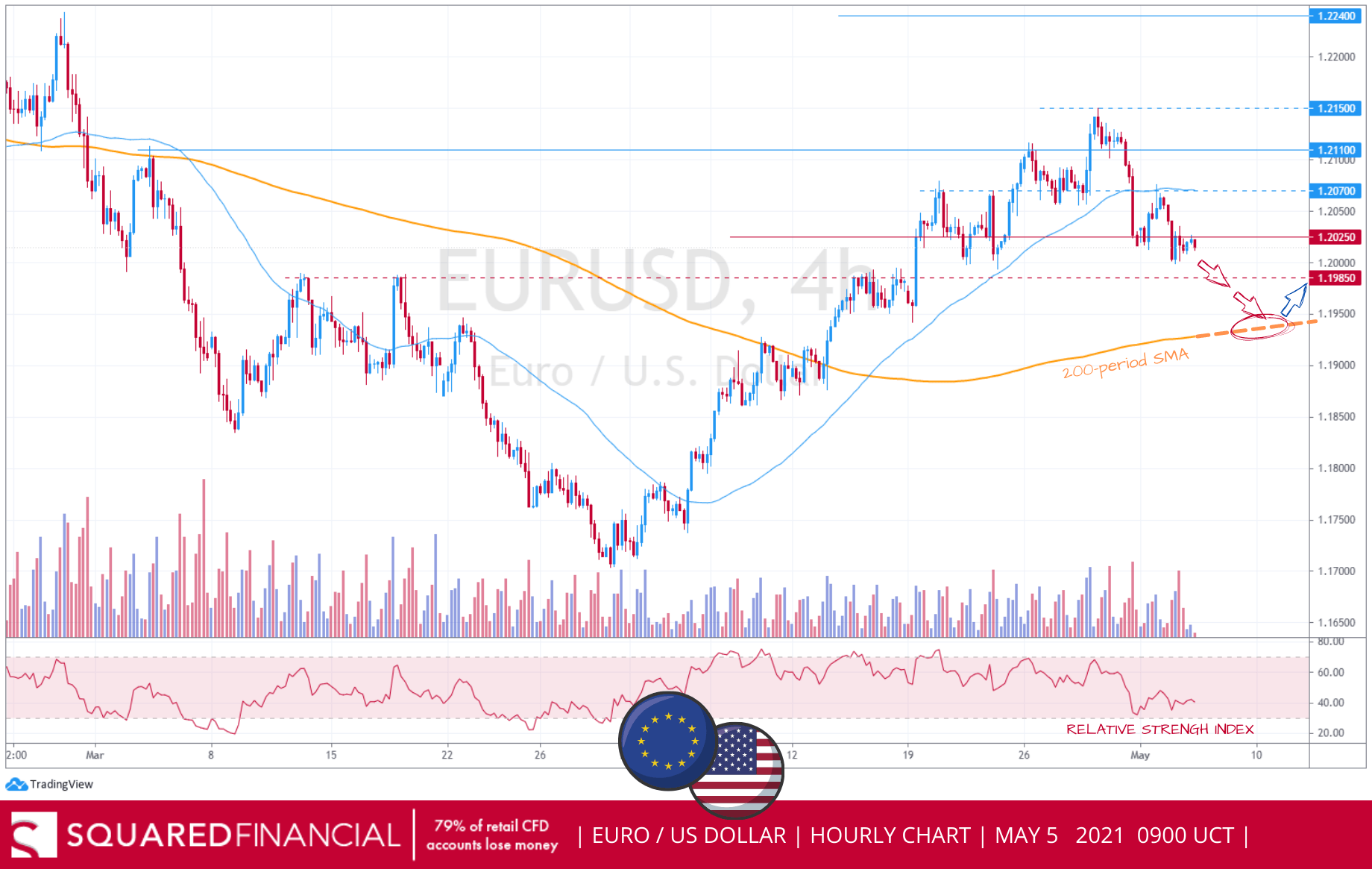

EUR/USD

The Euro is trading lower after a drop in high-risk assets following a sell-off in equities encouraged investors to buy the haven-linked US Dollar. The next EURUSD catalyst will be the Non-Farm Payroll on Friday. Until then, technical indicators favor more selling with a sustained move below 1.2025 to drive prices lower with 1.1985 and the 200-period SMA at 1.1950 as next support levels, ahead of service sector PMIs from the Eurozone due later today.

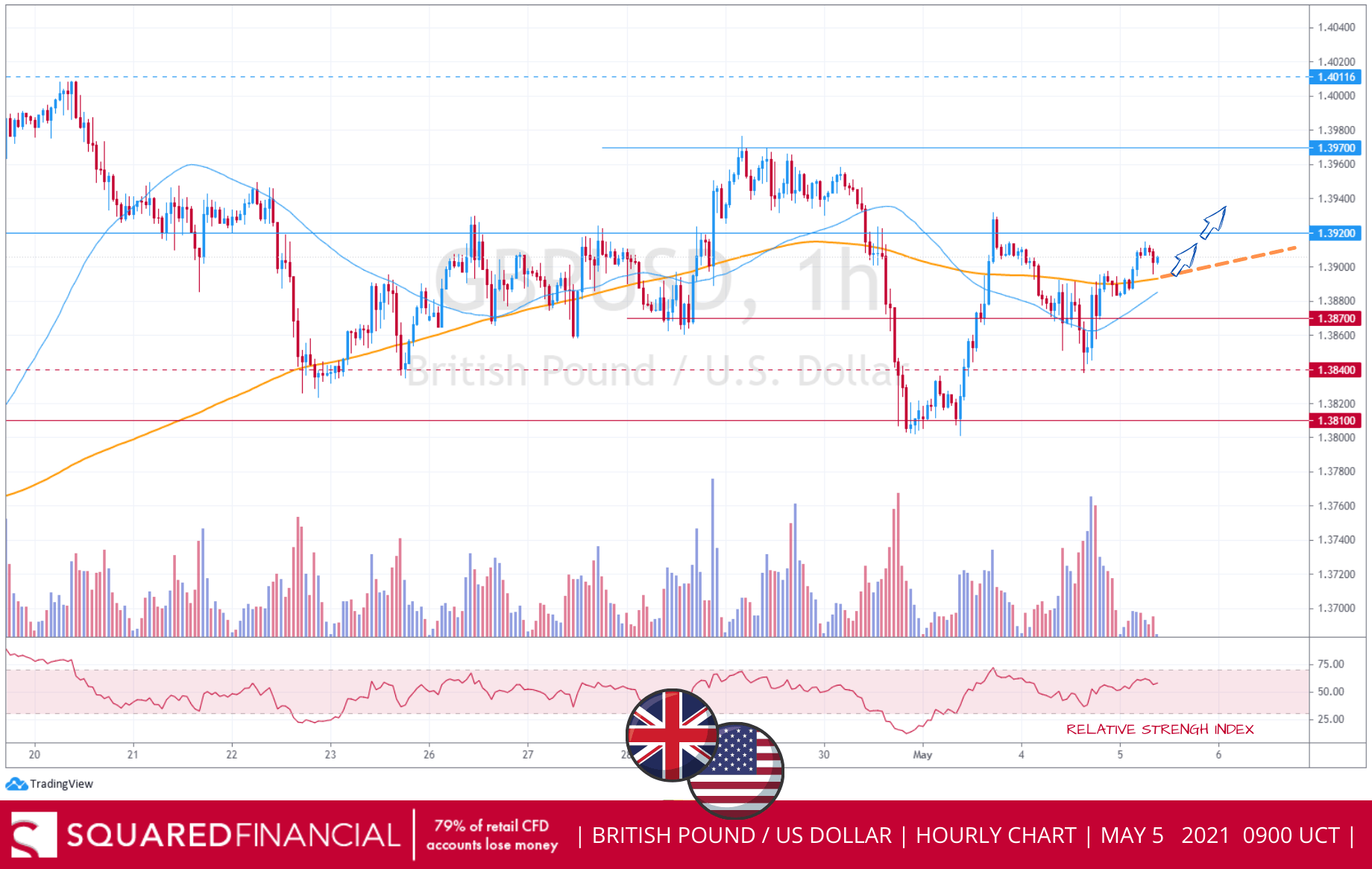

GBP/USD

The British Pound dropped to our support level at 1.3840 before turning around and surging above the trend-defining 200-period moving average as we continue to see buyers on dips. We expect positive pressure to build-up with a break above 1.3920 to trigger an acceleration to the nearest upside target at 1.3970.

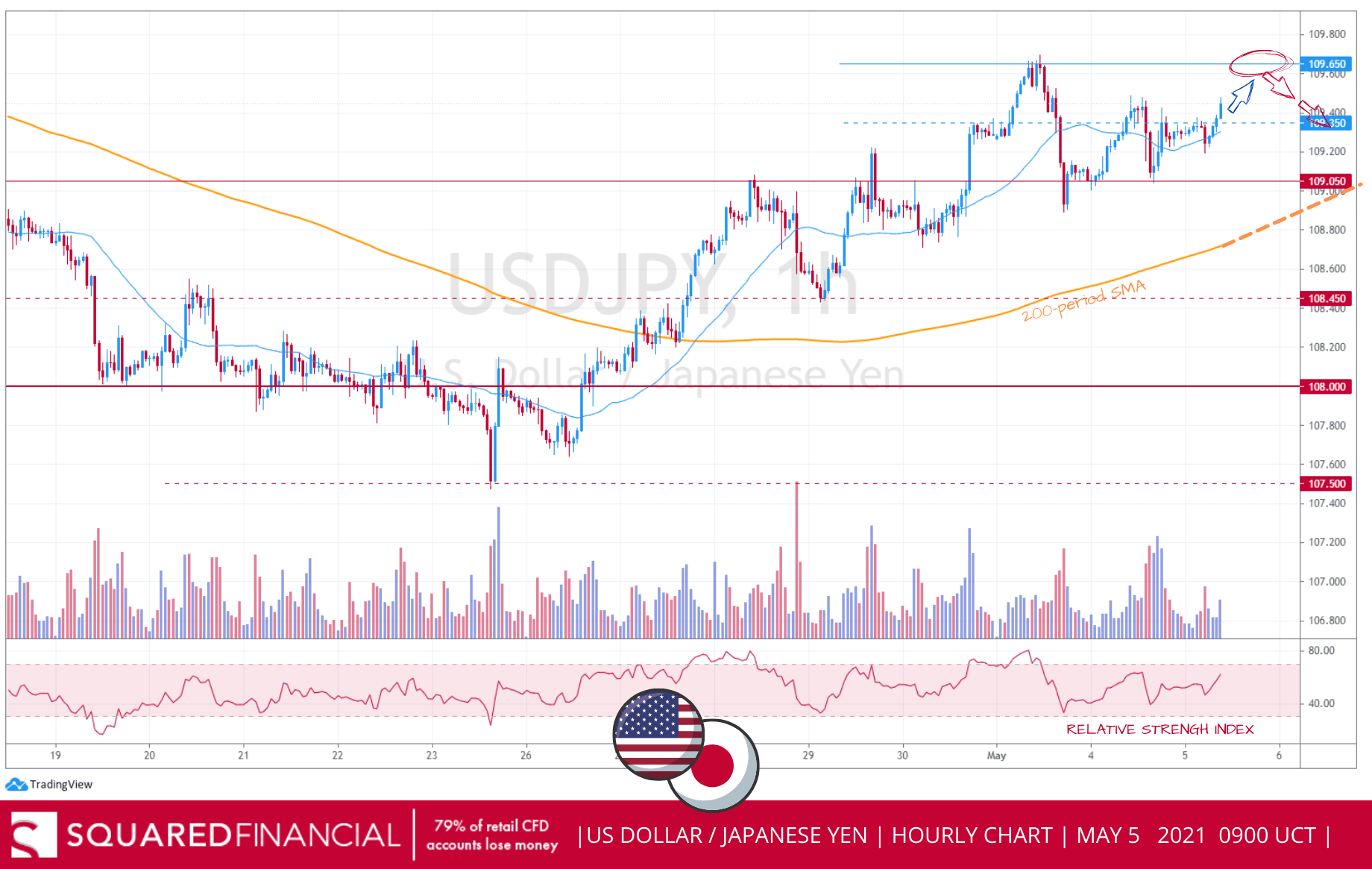

USD/JPY

USDJPY surged past our resistance at ¥109.35 driven mainly by a slight rise in US Treasury yields. Looking ahead, Japan is still on holiday for the second day and therefore thin trading conditions could lead to another day of volatile price action capped by ¥109.65 on the upside and supported by the key ¥109.05 level.

FTSE 100

The FTSE100 suffered heavy losses yesterday following a suggestion that US interest rates might need to be hiked if the economy heats up. Today, stocks in London seem to be opening higher in early morning trade as investors look ahead to a busy day of economic data with the 7000 level as nearest target, only if strong momentum persists and the UK index stays above the 200-period moving average.

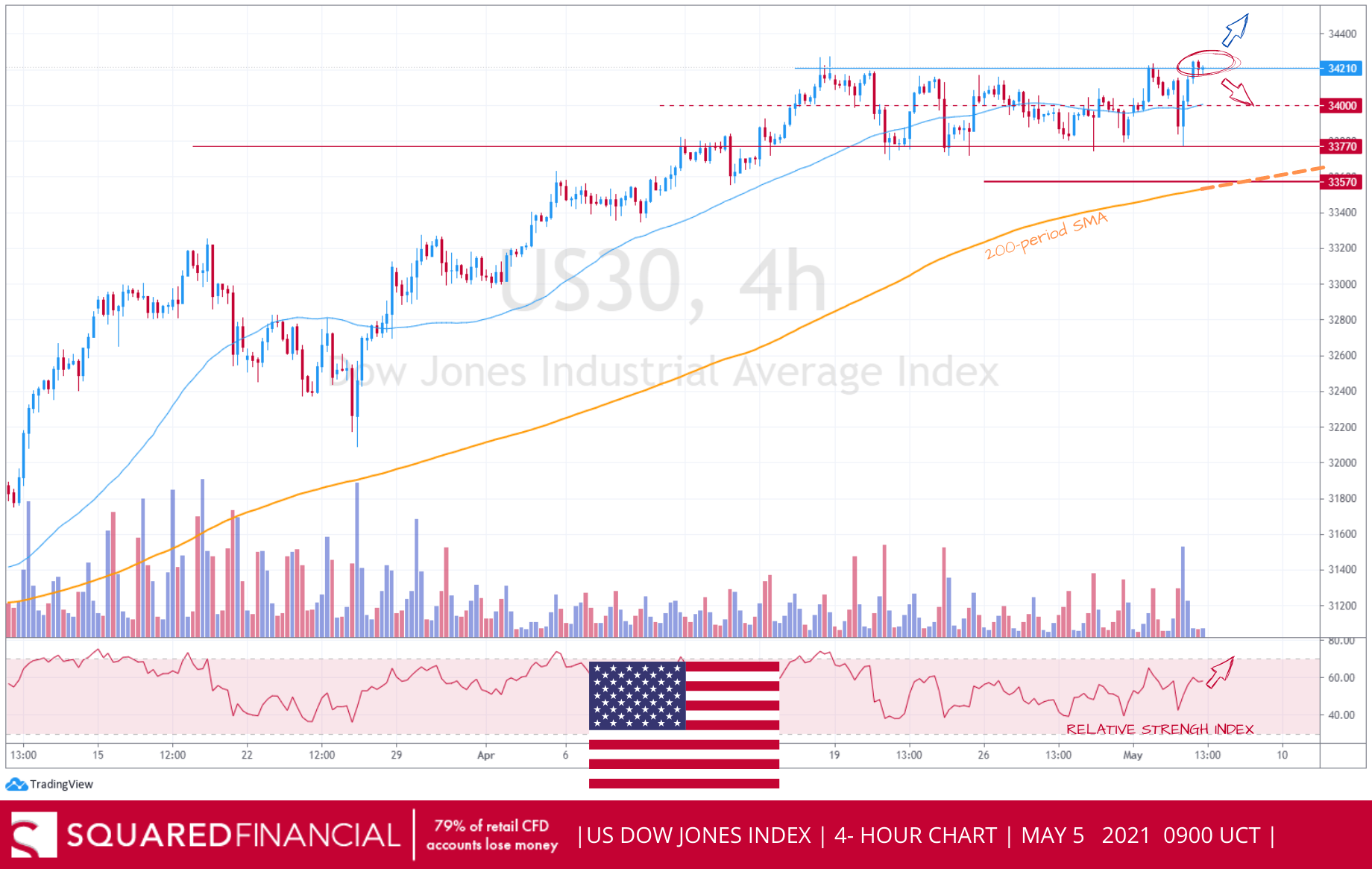

DOW JONES

Wall Street ended mostly lower yesterday with the Nasdaq plunging on valuation concerns after US Treasury Secretary Janet Yellen said interest rates could rise soon. The Dow Jones index on the other hand did manage to rebound back above 34000 from our support level at 33770, and the benchmark could be poised to continue pushing higher in the coming days ahead of the Non-Farm Payroll figure due Friday. However first we will need to move above the persistent resistance at 34210.

DAX 30

German stocks dropped, after a selloff in big US tech stocks, dragging European indices lower with the DAX-30 shedding more than 2% in yesterday’s session, to close below the 15000-mark. PMI data expected out of the Eurozone and Germany today, with a strong print to strengthen risk on sentiment. Technically, a breach of 15000 resistance level will favor further upside with 15100 as next resistance target.

GOLD

Gold ended yesterday’s session in the red as investors got spooked by Treasury Secretary Yellen’s remarks around interest rates “it may be that interest rates will have to rise somewhat...” which she later clarified, saying she was neither predicting nor recommending a rate hike. Technically, the yellow metal is in a short-term downtrend, printing below the 200 period SMA with $1773 and $1767 as the next support targets in extension.

US OIL

WTI Crude ended yesterday’s session in the green, above the $66 mark, rising by more than 2.50% after API inventory data came in at 7.70Mb, registering a build-up three times less than what analysts were expecting. All eyes today on official EIA data as investors await a confirmation on inventory drawdown, with consensus standing at -2.191Mb vs. a previous of 0.09Mb. Technically, an hourly close above $66.66 resistance level is needed to open the door to further upside.

Author

Rony Nehme

SquaredFinancial

Rony has over twenty years of experience in financial planning and professional proprietary trading in the equity and currency markets.