Italian Elections: Scenarios, Impacts and Effects on Euro and the Eurozone

Italians are going to vote this Sunday March 4th. And it is going to be messy. Vote is likely going to be inconclusive, as in Italy’s last general election in February 2013. It will be a close-run election with no party able to form a stable government.

Italy is experiencing a sluggish economic growth (averaging 0.4% / year), yet the fastest in more than a decade. However unemployment at around 11%, and roughly 35% for younger workers (50% in certain southern areas), remains very high. Italy has also many other problems dragging it down and preventing a continued recovery, including two big elephants in the room: one of the highest public debt in the world at 132% of GDP, and the critical situation of Italian banks and their NPLs (non-performing loans, where the borrower is late with repayments).

Major Players

The center-left Democratic Party of Matteo Renzi, past prime minister who promised to dismantle the old ways of the political establishment but fell well short and stepped down in 2016 – after the failure of his reform agenda – has slipped to 20% support, down from around 40%. His signature achievement? The legislation to reform Italy’s sclerotic labor markets, hardly a vote-winner.

The center-right coalition will be led by a reborn Berlusconi, often at odds with Matteo Salvini (leader of the Northern League) – who has his own eye on the center-right leadership – and with the group’s third, smaller partner: the right-wing Fratelli D’Italia (Brothers of Italy). Berlusconi’s Forza Italia is polling around 15%, slightly higher than the Northern League’s support, but well below the party’s best at 25%. The three share a political platform and a polled 35% of votes and could win the elections.

The Five Star Movement (M5S), no longer led by founder and comedian Beppe Grillo, but with an official 31-year-old prime ministerial candidate Luigi Di Maio, continued to gain momentum. It has an estimated support of around 26-30% and has matured since its founding 8 years ago. Support at it remains popular despite its poor performance running the council of Italy’s capital, the city of Rome.

Political Platforms

The Democratic Party (PD) following the direction established with the 2017 budget pledges to reduce corporate income tax from 24% to 22% (no estimate given but could cost tenths of billions) and give independent workers a tax deduction of €80 a month (estimated cost: around €1 billion). The PD also would like to have a minimum wage, cut social security contributions on wages from 33% to 29% percent, and introduce open-ended contracts, more convenient than short-term ones. Welfare policies include €400 a month per child for three years, tax deductions of €240 per child until 18, minimum pension at €750 a month (up from around €500 at present). Estimates say this simplification would cost an additional €33 billion a year. Migrant flows is one of Italy’s stinging issues. Bilateral agreements with countries of origin and lobbying to halt EU funding for countries like Hungary and Poland – that have refused to take in any of the 600,000 migrants who reached Italy over the past four years – are the PD responses. As per the European policies, the PD wants more economic and financial integration, with the introduction of joint Eurobonds, a Eurozone economic minister and direct election of the European Commission president, plus an ambitious reduction of Italy’s debt pile from 132% percent of GDP to 100% over a 10-year period.

The center-right wants a flat tax of between 15% and 23% with no taxes for those on the lowest incomes. Economists estimate the flat tax alone would cost around €80 billion, with the entire tax package possibly needing more than €100 billion. The center-right wants to remove the Jobs Act (introduced by Matteo Renzi) which makes both firing and hiring easier, and an “obvious” universal target of full youth employment. Welfare includes subsidies for families proportional to the number of children, hiking the minimum pension to €1,000 a month, plus the immediate removal of a 2011 pension reform, the so called Fornero’s law, which increased the retirement age, and its replacement that would cost around €140 billion. The center right is united in its call for developing Africans migrants back at home, while promoting a tougher stance by reintroducing border controls, blocking arrivals, imposing stricter criteria on granting migrants humanitarian protection and repatriating all migrants who have no right to stay. While Forza Italia has a pro-Europe stance, the Northern League remains firmly skeptic about the Euro and says Italy should leave the EU if fiscal rules are unchanged and if full and legitimate sovereignty is not restored, basically returning to before the Maastricht Treaty.

The M5S want to exempt citizens earning less than €10,000, a reduction in the rate of income tax and a “drastic” cut of a regional tax paid by companies. The income tax reform would cost between €13 to €20 billion. The MS5 want a “Smart Nation” and lots of jobs created through investments in new technology, a bit vague. M5S welfare envisages universal income for all: €780 for Italians below the poverty line, but only for those who actively seek work. The plan would cost an estimated €17 to €29 billion, or more a year, funded by spending cuts and tax hikes on banks, insurances and gambling industry. M5S also want to increase the number of police and strengthen checkpoints (10,000 new jobs) with immediate repatriation of illegal immigrants — but that requires repatriation deals with countries of origin, not yet in place. The M5S promise to make EU partners very unhappy with higher investments financed by higher deficit, while committing to reduce Italy’s massive debt by 40% over 10 years, which seem to pull in opposite directions.

Italy’s Most Burning Issues

None of the major parties to share votes on Sunday have directly addressed Italy’s most significant issues. While Italy’s role in the migration crisis has been front and center and has shaken the European Union since 2015, the state of the banking systems remains the biggest of the problems. Italian banks hold more than $220 billion in non-performing loans (NLPs), which impact lending and investment across the economy. Both the European Union and opposition parties have criticized the government’s attempts to rescue some banks using public funds. As consequence, rules against bank bailouts – seen as symptoms of perennial corruption – have been put in place, stipulating that bank investors, mostly middle-class Italians, must take losses before the government can step in.

Some bank analysts put estimate of NPLs held by Italian banks at a much higher €349 billion. Large banks, directly supervised by the ECB, hold the majority of these NLP, or an estimated €267 billion. This numbers have stayed relatively constant in recent years but that thanks to the European Central Bank's aggressive quantitative easing programme providing substantial assistance. Banks are also highly exposed to Italian government debt (around 20% of all BTPs, Italian government bonds with more than a year's duration).

Now, however, the ECB is looking to slowly wind up its Quantitative Easing, with the central bank expected to keep tapering its bond purchases in the coming months and the question becomes: what happens when the rate of purchase from the ECB slows down, the bond start to reverse and interest on debt start rising?

Analysts say that Italy is at risk of a broader financial crisis, if banks begin to fail. Some worry such a crisis could spread to other weak banks around Europe. One of such highly respected voices is that of strategist Jim Reid of Deutsche Bank. Reid’s analysts team said that "[Italy] a country … with high populist party support, with a generationally underperforming economy, a comparatively huge debt burden, and a fragile banking system which continues to have to deal with legacy toxic debt holdings ticks a number of boxes to us for the ingredients of a potential next financial crisis."

Despite the bailout of Monte dei Paschi (the oldest bank in the world and one of Italy’s systemically important banks), the bail-in of four local banks, the liquidation of two regional banks, and the market-led rescue of the banking group Carige, the Italian banking system has yet to be stabilized. Italy GDP is expected to grow 1% within next year and the questions remain: should the recovery be used to clean up banks’ balance sheets, by bundling their NPLs and selling them at a discount? But is such a growth rate sufficient?

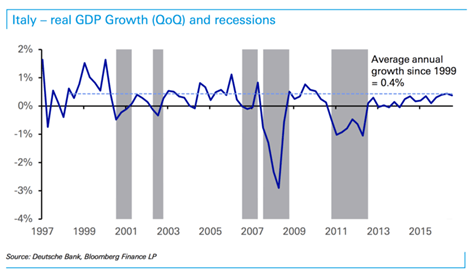

The sluggish Italian economy is, in fact, a connected, burning issue. Italy was hit hard by the 2008–2009 financial crisis, with a reduction of the economy of 9%, and suffered a double-dip recession and a collapse of domestic demand. Policymakers imposed budget cuts to try to control the country’s massive debt—now at about $2.8 trillion. With very small growth since 2014 (Figure 1) and persisting unemployment, many analysts agree on the needs of deeper reforms to promote hiring and investment. Some Italian politicians also blame the Euro common currency and EU budget rules for hindering the recovery.

Economic growth requires a healthy banking system. Italy's domestic banks have suffered greatly over the last few years having been poorly managed and riddled by stories of fraud and scandal.

Any new Italian government could and will likely have repercussions throughout Europe. With the Brexit, Italy is now the third largest economy of the European Union, and its ability—or inability—to manage the major issues, i.e. clean up its banks, return to growth, and put its national debt on a sustainable path will influence the health and the policy of the EU bloc, including military, monetary and banking policy.

Possible Scenarios and Impacts

Luckily (or unluckily?) in 2017 Italy changed its electoral system in a way that makes it harder for any single party to win a majority in parliament. The system has been engineered in a way that the outcome will likely require negotiating a large coalition. Whereas proportional representation will determine two-thirds of seats in the Camera dei Deputati (lower house), one-third will be decided by first-past-the-post voting in single-member constituencies. In such constituencies the M5S is likely to lose out, because it was neither willing nor able to form the electoral alliances needed to secure majorities. The party grouping that will benefit the most from the current electoral system will be the only one that has managed to forge a pre-election pact with other parties: the Berlusconi-led center right.

The system was meant to encourage coalition building (as well as maintain the status quo) but could complicate and delay forming a government which, in turn, could make the markets nervous in the short term. Any party or coalition will likely need more than 40% support to win enough seats to govern and no party is currently polling above that mark. The outcome imposed by the electoral system has pros and cons. On the one hand, a large coalition may be seen as positive by markets, but would likely penalise the M5S. On the other hand, eyebrows could be raised and bring into question the counter-productivity of a muddle-through strategy and reduced effectiveness and ability of a large coalition in tackling Italy’s most important issues.

Jim Reid’s team again notes: "a heterogeneous, ineffectual government would struggle to boost the too low potential GDP growth and a continuation of Italy's deeply unsatisfactory economic performance would ultimately benefit Eurosceptic and populist parties. With that in mind, the longer Italy remains in a muddle-through, the greater the likelihood that Eurosceptic parties could gain an ample majority in the Italian parliament."

Based on the current polls, the most likely scenario is a relative majority for Berlusconi’s bloc, which might be forced to form a left-right alliance with the PD to create a broad, centrist coalition. This has already been happening at the local and even at the regional levels, in many Italian areas. A more radical outcome – based on the actual results obtained – could encourage the Northern League to try forming its own government, as could, potentially, the M5S. M5S has long ruled out forming an alliance with any other party but the new charismatic leader Luigi Di Maio has softened that stance in the lead-up to the polls.

To fix Italy's banking system and related issues, the government that emerges from the general election this Sunday will need a solid majority, a willingness to confront vested interests, corruption and bureaucracy and a comprehensive strategy to boost economic growth. But none of the parties has shown any indication that it can meet any of these criteria, much less a coalition of two of them. There is also some worry among European officials about growing hostility to EU institutions that now animates much of Italian politics. While rallying into the elections tones have been subdued, a government led by the Northern League (or M5S) could see a referendum on Italy’s membership in the Eurozone (temporarily off the table), or a call to renegotiate the EU foundational treaties, or delay plans for deeper European integration.

Finally, most in not all the contenders’ parties hold views on relations with Russia that look like a clear break with the status quo. Berlusconi is a close personal friend of Russian President Vladimir Putin. M5S have spoken in support of Russia’s policy in Syria and criticized EU sanctions on Russia over Crimea annexation, and called for Italy to play a reduced role in the North Atlantic Treaty Organization (NATO). Even Matteo Renzi leader of the normally EU-friendly Democratic Party, was beating the anti-Brussels drum late in 2016.

Technical Review of the Euro and potential impacts

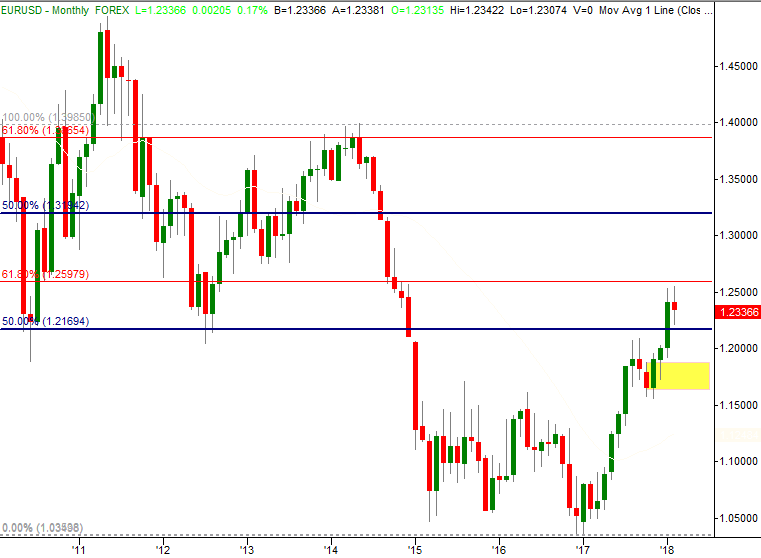

The Euro/Dollar pair, after basing for around 2 years between 2015 and early 2017, has moved higher during 2017 to challenge the first area watched by Smart Money, Program Trading and Algorithms at 1.2170. No short interest was shown by participants in that area. In the meantime Dumb Money (the crowd) is looking for a continuation of the move higher that can clearly be seen on charts.

Above 1.26 the Euro has the potential to continue higher into the 1.32 next resistance area. If fear or worry sets in the markets, after the Italian elections and/or during the negotiations for a new government – or if the M5S wins the elections, we could see a sharp market correction into the 1.1600 – 1.1900 area. If it happens, the extent of the move would also depend on whether the environment of raising interest rates in the US will be able to slow down and reverse the current move lower in the Dollar Index.

On the upside, a surprise vote bringing Berlusconi’s coalition to over 40% and short consultations for the creation of the new Italian government could push the Euro higher very quickly, in few weeks, into the 1.32 area.

In the intermediate and long-term, should the new government demonstrate inability to manage the major issues (banking system, return to growth, indications that debt is being addressed, etc.) and a new crisis affect Italy and the EU, we could see the Euro moving down to the bottom of the 2015-2017 range in the 1.05 area, or below.

Do you trade Forex & Futures and what to learn how we model areas of potential participation from professionals and non-professionals traders, the effects on price of crowd psychology & some classes of algorithms and receive trade ideas? Take advantage of the FXStreet offer for 30 Days now!

Author

Giuseppe Basile, CSTA/IFTA

FibStalker Trading

Swing Trader, Mentor, Technical Analyst and active market researcher and IFTA associate, in the markets since 2001. Publisher of www.fibstalkertrading.com specializing in forex, futures and stocks trading and mentoring.