It is time to act

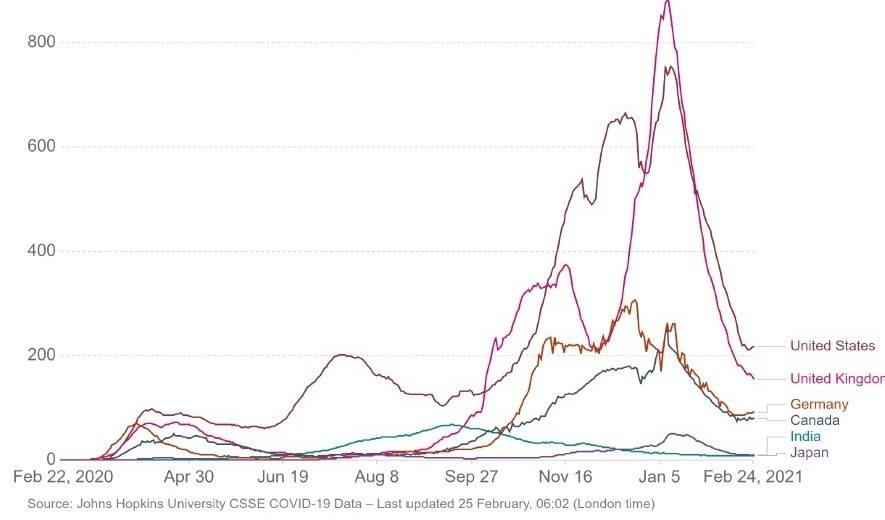

The pandemic, despite the great upsurge of recent months, seems to be declining more and more, both in human and economic terms, as time goes on. The new cases are also reduced with the vaccination of the population, both the cases as shown in the diagram below and the deaths will be reduced.

Daily new confirmed Covid-19 cases per million people

Therefore, the return to normal conditions is coming. Normal conditions that, however, will be new conditions both in human and in business and economic level. After the big drop in GDP, the challenges for a strong and long-term recovery will be many. The fact is that public debt during the pandemic has skyrocketed in many countries. To make these debts manageable and gradually reduce them, interest rates will need to be kept low for many years at least below the level of growth.

Low interest rates will help finance low costs for both companies and households. This will boost economic and business activity and keep markets growing. In the stock markets there was a significant decrease in prices in March 2020, but then prices recovered, some with a large extent and others with a lower intensity.

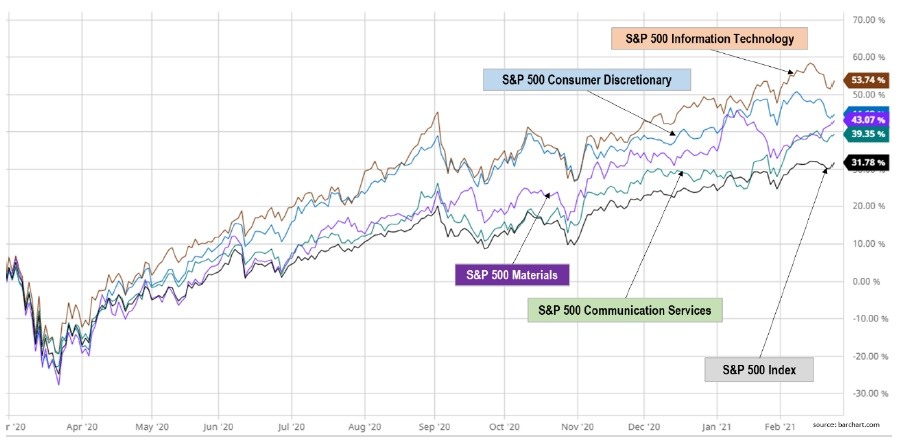

In the US stock markets for the S&P index we observe the following:

As can be seen in following chart, the most important increase and therefore the largest profits in relation to the S&P index is shown in the Information Technology sector. The second most strengthened sector is the one related to the Consumer Discretionary sector while the next most strengthened sectors were the Materials and Communications Services sectors.

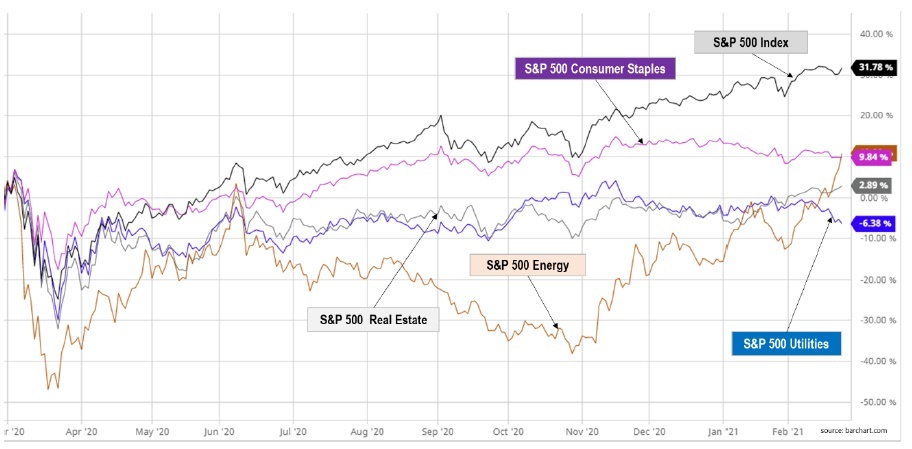

Healthcare, industry, and finance sectors performed slightly lower returns compared to the SP 500, as shown in the chart below:

Finally, the sectors that are lagging behind the performance of the SP500 index, but perhaps these are the sectors that will be of most interest in the future, are the Consumer Goods sector, the Energy sector, the Real Estate sector and Utilities.

As the economy gradually returns to normality the sectors of Value Stocks that were underperformed will tend to converge with overall market returns. The fact is that Growth Stocks once again outperformed value stocks in 2020. However, as markets due to low interest rates and growth will maintain, as a whole, their positive dynamics the recovery in Value Stocks is a possible scenario for the year 2021.

The historically high prices of Growth Stocks inevitably lead to comparisons with the bubble dot.com in the late 1990s. In n the early 2000s, financial, energy and real estate stocks performed better than high-tech stocks. Obviously, times are different, and the fourth industrial revolution is now much more mature and able to maintain the high growth of technology companies. However, valuations for growth stocks are now considered overvalued. Growth stocks now have very high price-to-earnings (P/E) ratios and high price-to-book ratios.

Perhaps a rational strategy would be to restructure trading and portfolio positions from overvalued stocks, which are mainly high-Growth Stocks, to Value Stocks that, due to the pandemic conditions, have recovered at a slower pace but have good fundamentals which give long-term value.

The first signs become apparent from the negative movements of the stock indices that refer to the growth stocks. So, maybe it is time to act.

Author

Nikolaos Akkizidis

LegacyFX

Mr Nikolaos Akkizidis is an economist, with 20+ years of experience in multiple roles in the financial sector.