ISM Services smashes estimates to the upside, S&P services is deeply negative

Once again we have huge divergences regarding the strength of services. Let's compare two reports, supposedly measuring the same thing.

ISM® table and quotes below by permission from the Institute for Supply Management.

Unexpected services rise

For June the ISM® Services index was 55.3. Bloomberg Econoday economists expected the index to drop to 53.0.

Econoday posted "The ISM services index has been slowing and is expected to slow noticeably in July, to a consensus 53.0 from June's 55.3."

July 2022 services ISM® report on business®

Please consider the July 2022 Services ISM® Report On Business®

The report was issued today by Anthony Nieves, CPSM, C.P.M., A.P.P., CFPM, Chair of the Institute for Supply Management®.

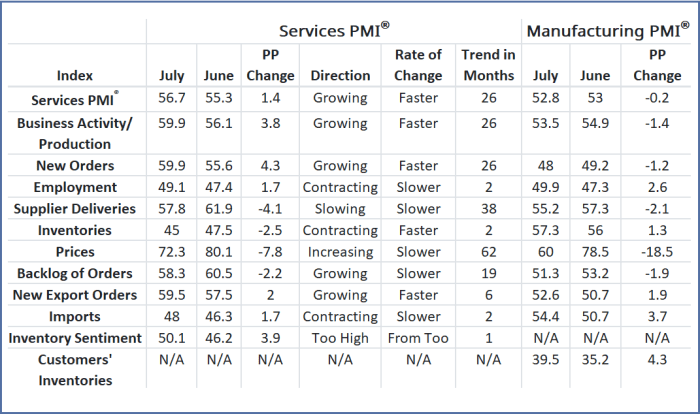

In July, the Services PMI® registered 56.7 percent, a 1.4-percentage point increase compared to the June reading of 55.3 percent. The 12-month average is 60.2 percent, reflecting consistently strong growth in the services sector, which has expanded for 26 consecutive months. A reading above 50 percent indicates the services sector economy is generally expanding; below 50 percent indicates the services sector is generally contracting.

A Services PMI® above 50.1 percent, over time, generally indicates an expansion of the overall economy. Therefore, the July Services PMI® indicates the overall economy has followed the same path as the services sector: expansion for 26 straight months following two months of contraction and a preceding period of 122 months of growth. Nieves says, “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for July (56.7 percent) corresponds to a 2.4-percent increase in real gross domestic product (GDP) on an annualized basis.”

Mixed bag from ISM® respondents (Emphasis Mine)

-

“Restaurant sales have softened the past few weeks (due to) post-holiday and seasonality factors, but we’re also hearing because of consumer pressures, particularly fuel and food prices. Staffing remains a challenge in some markets. Many of our locations in (Los Angeles County) received news that there could be a return to (indoor) mask mandates.” [Accommodation & Food Services].

-

“Interest rates have significantly impacted the homebuilding market. Cancellation rates have increased, as homebuyers can no longer afford the monthly payment. Traffic to our communities is down. Inflation has sidelined many would-be buyers.” [Construction].

-

“Strengthening market overall and signs of improvement. Increased prices putting a strain on fixed budgets. There has been a shift from driving down costs to securing continuity of supply. Higher education is growing, with an increase in applicants.” [Educational Services].

-

“Business continues to remain below pre-pandemic levels. (Patient) census and visits have increased but seem to have plateaued in the last six-month period.” [Health Care & Social Assistance].

-

“Can feel the economy weakening. Clients are making appropriate moves in anticipation of a recession.” [Management of Companies & Support Services].

-

“Hiring demand remains robust in most industry sectors. Tech has had a slowdown in hiring and layoffs. It’s still a candidate’s market, as the number of job openings across all skill levels and positions remains far greater than the number of candidates for those roles.” [Professional, Scientific & Technical Services].

-

“Rising costs across the board seems to be the big focus now. Fuel and food are the most common focus but it is across the board, and there is pressure of a job market shortage for qualified workers to increase wages and other benefits.” [Public Administration].

-

“(We are) in inventory reduction mode, attempting to match inventory levels to current lower sales trends.” [Retail Trade].

-

“Holding steady, but some headwinds are definitely ahead on the economic front. However, supply chain issues appear to be easing, though still not great.” [Utilities].

-

“Food service remains strong. Retail is softening as the mass is overly concerned about inventory and consumer spending.” [Wholesale Trade].

The ISM® respondent comments don't match the strength in the overall numbers.

There were only a few positive comments out of ten. I emphasized the negative one. Only point three was unilaterally positive. Point six was mostly positive and point 10 was mixed.

S&P global US services PMI™

It's very confusing because both the S&P and ISM® use the term PMI.

With that in mind, please consider the S&P Global US Services PMI™

Key findings

-

Business activity declines for first time in over two years amid soft demand conditions.

-

Fastest fall in output since May 2020.

-

Cost pressures ease further.

-

Business confidence slumps to lowest in almost two years.

Business activity across the US service sector decreased at a solid pace during July, according to the latest PMI™ data. The fall in output was the fastest since May 2020. Although new orders returned to growth, the rate of expansion was historically subdued and much slower than those seen earlier in the year. Subsequently, service providers registered weaker expectations regarding the outlook for output, as confidence dropped to a 22-month low. Nevertheless, companies expanded workforce numbers at a solid pace, with sufficient capacity allowing firms to work through backlogs of work effectively.

Inflationary pressures remained historically elevated during July, but eased further. Input costs and output charges increased at the slowest paces for five and 16 months, respectively.

The seasonally adjusted final S&P Global US Services PMI Business Activity Index registered 47.3 in July, up slightly from the earlier released 'flash' estimate of 47.0, but down from 52.7 in June. The latest headline reading signalled the fourth successive decline in the seasonally adjusted index, marking a notable contrast seen from the steep expansions earlier in the year. The decrease in business activity was the first since June 2020 and solid overall. Where firms reported a contraction in output, this was linked to relatively subdued demand, worsening financial conditions and higher prices

Chris Williamson, Chief Business economist at S&P global market intelligence

"US economic conditions worsened markedly in July, with business activity falling across both the manufacturing and service sectors. Excluding pandemic lockdown months, the overall fall in output was the largest recorded since the global financial crisis and signals a strong likelihood that the economy will contract for a third consecutive quarter."

S&P global US composite PMI™

The S&P also reports private sector output contracts at fastest pace for over two years.

The S&P Global US Composite PMI Output Index posted 47.7 in July, down from 52.3 in June to signal a renewed contraction in private sector business activity. The decline in output was the first since June 2020 and broad-based.

The composite is a blend of manufacturing and services.

Venus vs Mars

One of these reports appears to be a survey taken on Mars. The other appears to be from Venus.

Both are diffusion indexes. That means direction is more important than magnitude.

For example, one firm hiring 2 people and a second firm firing 2,000 balance out to zero.

If one survey is more weighted to food service and the other construction, that also will change the mix of answers.

We have seen these divergences before. I expect resolution to the downside.

Hello recession deniers, It's already time to ponder a third quarter of negative GDP

On August 1, I commented Hello Recession Deniers, It's Already Time to Ponder a Third Quarter of Negative GDP

I think Chris Williamson has this one correct regarding the "strong likelihood that the economy will contract for a third consecutive quarter."

Looking ahead

Much of GDP changes very little throughout the quarter (military spending, Medicare, Social Security, food stamps, etc.)

It's cyclicals (durable goods and housing) that tend to drive expansions and recessions.

July may see improvement on inflation based on energy. But rent (over 31 percent of the CPI) is still rising. Consumer sentiment is poor and inflation-adjusted retail sales do not rate to be good for the entire quarter.

Cyclical discussion

-

July 12, 2022: Cyclical Components of GDP, the Most Important Chart in Macro.

-

July 14, 2022: A Big Housing Bust is the Key to Understanding This Recession.

Housing will be another big bust this quarter. And durable goods rate to follow housing. Manufacturing rates to be negative.

Hopes for the quarter rest solely on consumer spending and falling inflation. But don't count on strong retail sales.

Add it all up and you have a third quarter of negative GDP.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc