ISM Manufacturing PMI Preview: The homeward turn

- Manufacturing PMI predicted for a modest rise

- Trade, global slowdown undermining confidence

- US economic growth may help restore sentiment

The Institute for Supply Management (ISM) will issue its purchasing managers’ index (PMI) for the manufacturing sector for July on Thursday August 1st at 14:00 GMT, 10:00 EDT

Forecast

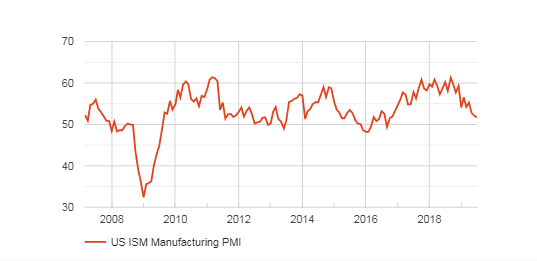

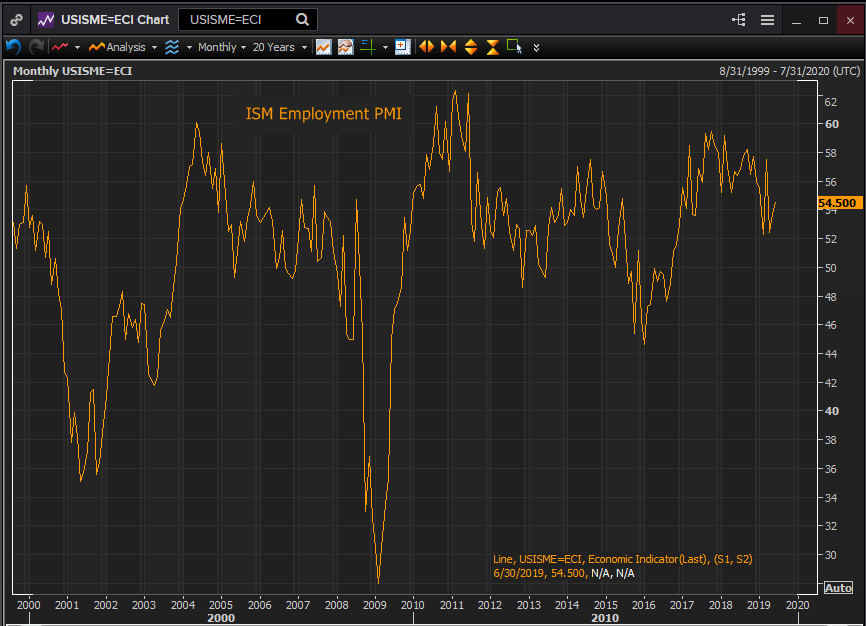

The purchasing managers’ index is expected to move to 52.0 in July from 51.7 in June. The prices index will increase to 49.6 from 47.9. The employment index is projected to fall to 53.4 in July from 54.5. The new orders index was 50.0 in June down from 52.7 the prior month.

US Manufacturing: Two good years

The heady days for the factory sector from mid-2017 to the first quarter of 2019 which saw some of the best sentiment reading in 20 years and the strongest hiring in a generation, have turned circumspect as executives measure the impact of the trade dispute with China, Brexit and other trials of the global economy.

FXStreet

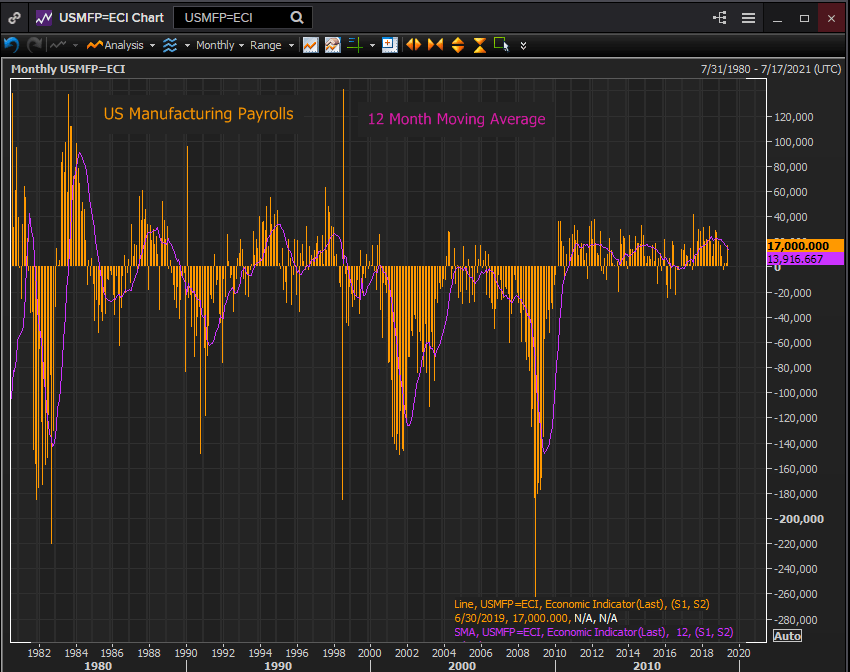

Assumed by most economists to be headed for extinction after losing factories, jobs and revenue for three decades, the unexpected revival in the US manufacturing sector, spurred by the policies of the incoming administration in 2017, reopened plants and brought prosperity back to many small towns across the country.

From January 2017 through June 2019 the economy created 498,000 new factory jobs averaging 16,633 per month. In 2018 the sector saw the most rapid additions to payrolls in two decades.

Reuters

Manufacturing PMI: Frayed confidence

The confidence of the manufacturing sector from the middle of 2017 to the middle of 2018 witnessed the highest sustained PMI averages in a generation. The August 2018 reading of 61.3 was the highest since 2004. Part of the optimism was likely due to the sudden and somewhat unexpected reversal of fortune in factory production as much as to the improvement in long term prospects. The euphoria couldn’t last.

The trade dispute with China, which initially seemed amenable to quick solution has turned into a grinding confrontation in which each side seems to feel that time will strengthen its hand. Beijing may even be waiting for next year’s US Presidential election.

Trade talks have resumed but expectations for a settlement are much lower than last year. Washington and Beijing say they are committed to a trade deal, but the demands from each have not moderated. Businesses must now plan for a prolonged argument with tariffs the new mediator of trade.

Manufacturing confidence slipped sharply in the January government shutdown and has not returned to its pre-closure levels though hiring has retained a greater share of its optimism. Manufacturing payrolls jumped 17,000 in June after three months of lackluster hiring so it likely that the labor market reflects domestic economic growth despite global concerns.

Reuters

Conclusion

American economic growth decreased in the second quarter to a 2.1% annualized pace in the initial estimate from the Bureau of Economic Analysis, giving the first half a 2.6% run. The inventory build that bolstered GDP in the first three months was not repeated but improved consumer spending makes a renewal in the third quarter a possibility. A 5.2% drop in exports subtracted from the final figure and some of that is certainly due to the tariff war with China.

If the US China trade dispute has become the new normal for international trade American manufacturers will gauge how much of their business is affected. That is a different question than measuring sentiment which is unlikely to improve much until there is an agreement.

The US has the world’s largest domestic market. With steady economic growth and booming job creation American manufacturers may soon take heart from their homegrown good fortune rather than looking overseas for inspiration.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.