Is the US stock market headed for new lows?

Stock markets have taken heavy damage this year, suffering at the hands of rapidly rising interest rates. Valuations have compressed but are still not cheap enough to lure in bargain hunters, and there is a clear risk that earnings estimates are revised lower as the data pulse slows, especially in Europe and China. While this could spell more trouble for equities, investors should not lose sight of the big picture - every crisis passes.

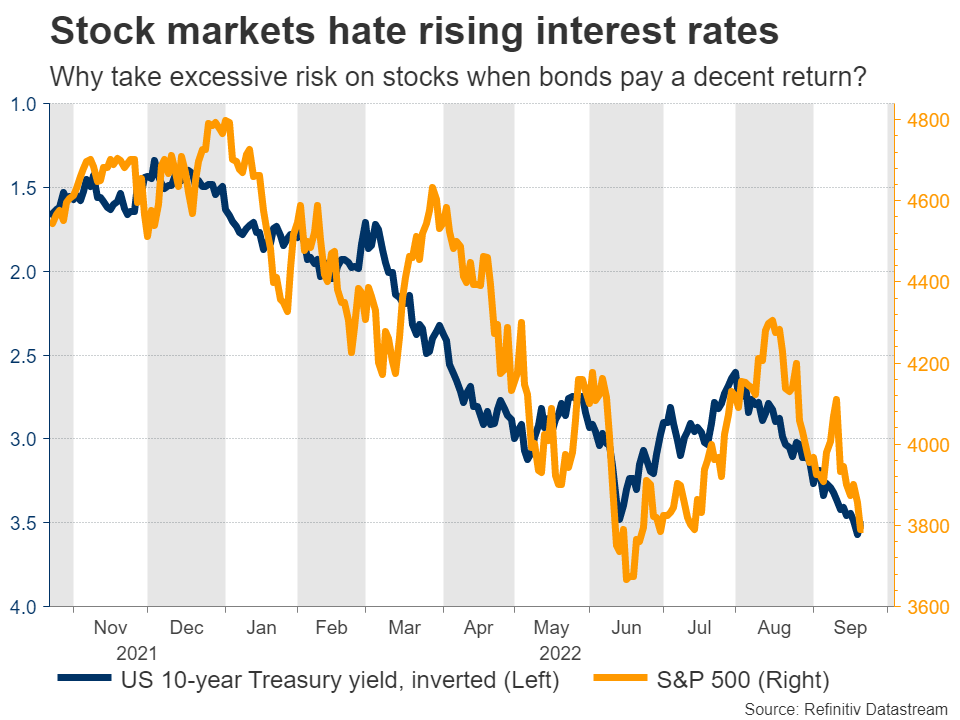

Fed hangover

For more than a decade after the financial crisis, central banks and equity markets were best friends. It was a period of very low inflation, so every time the economy faced some problem, investors could count on central banks to ride to the rescue by lowering interest rates or doing quantitative easing.

This recipe is rocket fuel for stocks. In a regime of low or negative interest rates, returns on bonds are miniscule, which naturally pushes investors towards riskier assets. With money managers raising their exposure to stocks and companies enjoying easier access to capital, valuations usually expand and markets thrive.

Enter inflation. An overload of public spending during the pandemic coupled with supply chain disruptions and the Ukraine war came together to generate the greatest inflation shock in four decades. Central banks spearheaded by the Federal Reserve decided they had to extinguish this firestorm at all costs, so they started raising rates at an incredible pace.

Policymakers hope that higher rates will lead to an economic slowdown, initially in sectors such as housing that are more sensitive to higher borrowing costs and ultimately in the broader economy. Once unemployment begins to rise, that will hopefully reduce demand enough to cool inflation. In other words, the plan is to engineer a recession in order to fight inflation.

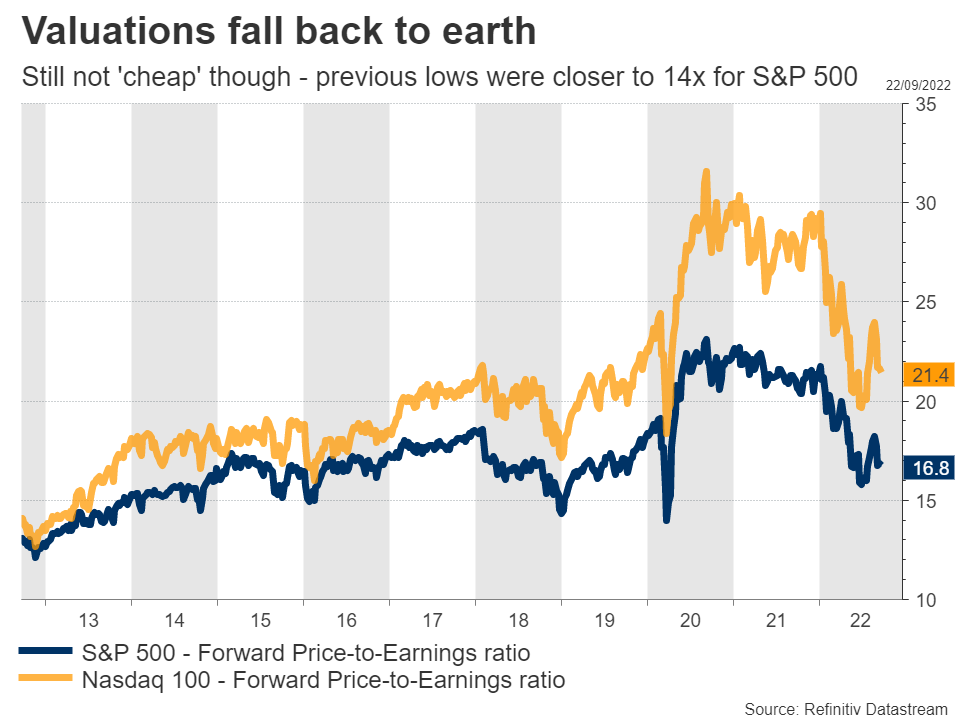

Still not cheap

Over time, rising interest rates translate into lower valuations for riskier assets as traders dial back excessive risk-taking in favor of safer plays. This is precisely what happened this time - most of the selloff in stock markets boiled down to a compression in valuation multiples.

Since the beginning of the year, the S&P 500 index has lost 21% of its value. Over the same timeframe, its valuation from a price-to-earnings perspective has declined by around 25%. Despite this massive correction though, the market is still not cheap from a historical perspective.

The price-to-earnings multiple denotes the dollar amount someone would need to invest to receive back one dollar in annual earnings. As such, the lower this number is, the ‘cheaper’ the market is considered. The S&P is still trading at a forward multiple of 16.8x, while most of the selloffs over the last decade - for instance in 2020, 2018, 2016, and 2015 - ended with a multiple closer to 14x or 15x earnings.

In fact, that may be too optimistic since the last decade was characterized by ultra-low interest rates, and therefore elevated valuation multiples. With rates much higher now and the Fed’s quantitative tightening process doubling in speed this month, this bear market might conclude with an even lower valuation multiple, leaving ample scope for further downside.

Even more so if earnings estimates are revised lower. The Fed is actively trying to weaken the US economy and the bond market is screaming it will get its wish, with the yield curve inversion deepening lately. That’s bond traders betting on the economy going downhill, and it has preceded recessions with terrifying accuracy.

Additionally, consider what is happening around the world. Companies in the S&P 500 receive some 40% of their revenue from overseas, increasing to almost 60% in the tech sector. Those revenues will come under pressure from two sources - a stronger US dollar and the twin crises tormenting Europe and China.

Winter in Europe could be harsh considering the dramatic spike in energy prices. Authorities have rolled out several measures to spread the burden, but the consumer will still take a heavy hit. The situation in China is even worse, with the property sector melting down and strict covid lockdowns in major cities - a combination that has brought the economy to its knees.

Don’t panic

All told, there’s likely some more downside left for equities, especially in case a recession does materialize. There is a long lag between raising interest rates and the time it impacts economic activity, so the real effects of the forceful tightening today might only show up next year.

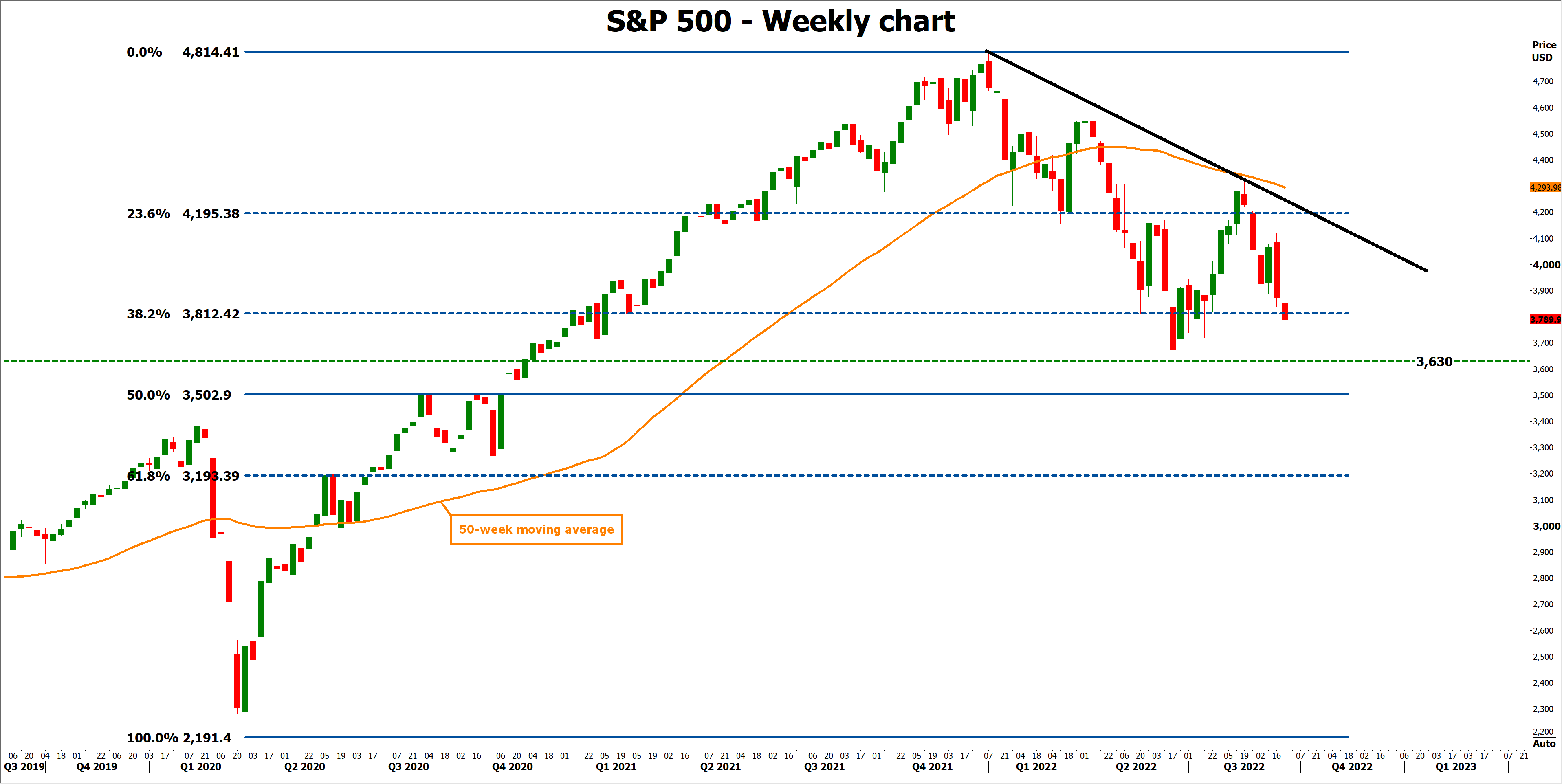

Business surveys and other leading economic indicators already paint a grim picture of what comes next and the charts concur, with the S&P 500 trading below a downtrend line and its key moving averages. If it does break to new lows, a fierce battle could take place around 3,500, which is the 50% retracement of the rally from covid lows to record highs.

The good news? Even if there is a recession, it is likely to be shallow since it will be caused by the Fed itself, not some external shock. Once the economy is in real trouble, the Fed can turn the ship around, assuming the inflation problem is cured by then.

Don’t miss the forest for the trees - every crisis passes and markets move higher over the years. This storm might simply offer patient investors better entry points.

Author

Marios graduated from the University of Reading in 2015 with a BSc in Economics and Econometrics. Prior to joining XM as an Investment Analyst in December 2017, he was providing financial analysis, reporting and consulting service