Is the US Dollar doomed or is a correction looming? [Video]

-

US Dollar wallows near 3-year lows as bearish bets gather pace.

-

Fed rate cut expectations and economic worries weigh.

-

Trade and Trump-related uncertainty casts a shadow over the outlook.

-

But is the gloom overdone?

![Is the US Dollar doomed or is a correction looming? [Video]](https://editorial.fxsstatic.com/images/i/DollarIndex_XtraLarge.png)

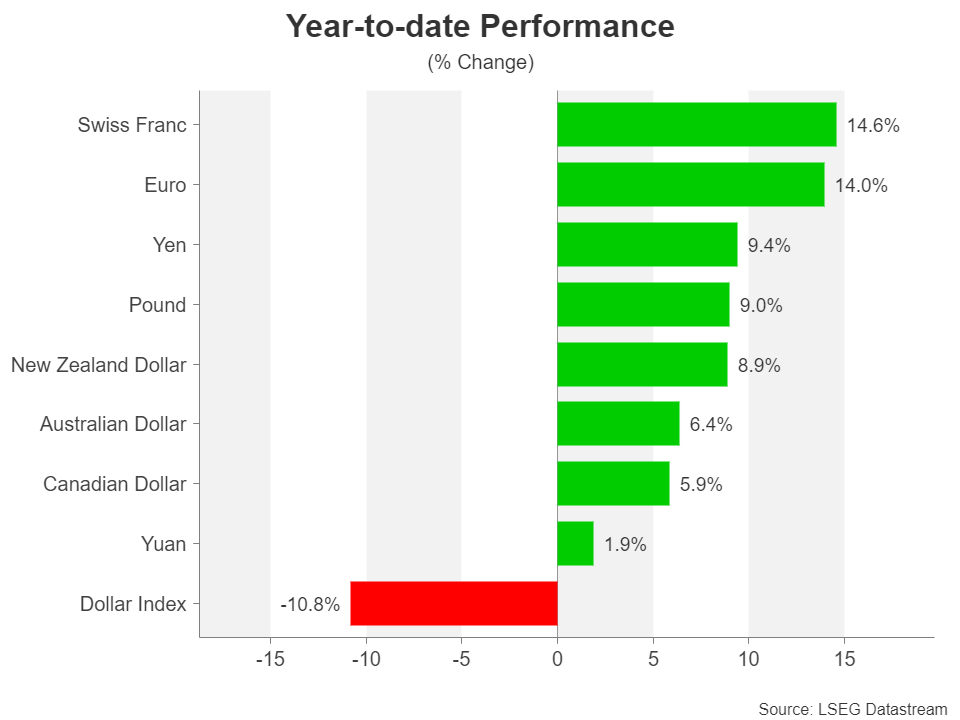

Worst start to year in half a century

The US dollar index (DXY) just had its worst first six months of the year in more than half a century, losing over 10% against a basket of currencies. This closely watched dollar gauge, which measures it against six other major currencies – the euro, Japanese yen, pound, Canadian dollar, Mexican peso and Swedish krona – is currently trading at levels last seen in February 2022 before the Federal Reserve embarked on its aggressive tightening campaign.

Yet Fed policy remains tight, both in comparison to recent times and relative to other countries. So why is the dollar under so much pressure? Well, US politics has a lot to answer for. President Trump’s trade war has taken the shine off the world’s number one reserve currency, as higher tariffs have stoked fears of stagflation and a global recession.

The de-dollarization effect

But that’s not all. Trump’s protectionist and isolationist stance are seen as marking the end of US exceptionalism. Investors have also been spooked by Trump’s various attempts to undermine the rule of law, bypass the courts and overreach his executive powers as president.

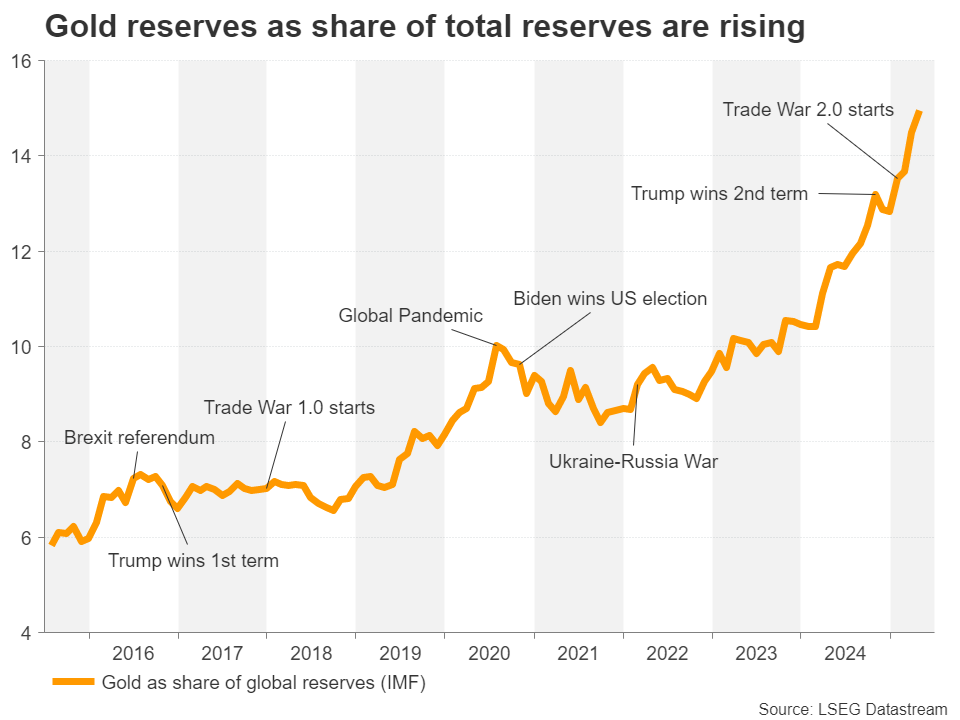

More concerning is the acceleration of de-dollarization by several, mainly emerging market countries, like China and Russia, in an effort to reduce their dependence on the US economy as well as become less vulnerable to sanctions by Washington. The dollar’s share of global reserves has fallen from over 70% at the turn of the century to just under 60% in 2024.

A twin deficit problem

America’s twin deficit problem is another long-running headache for the greenback. The Republican-led Senate just passed a tax and spending bill that looks set to add more than $3 trillion to America’s debt pile. And with investors not hopeful that Trump’s trade policies will slash the country’s massive trade deficit, the dollar is looking like a risky bet right now.

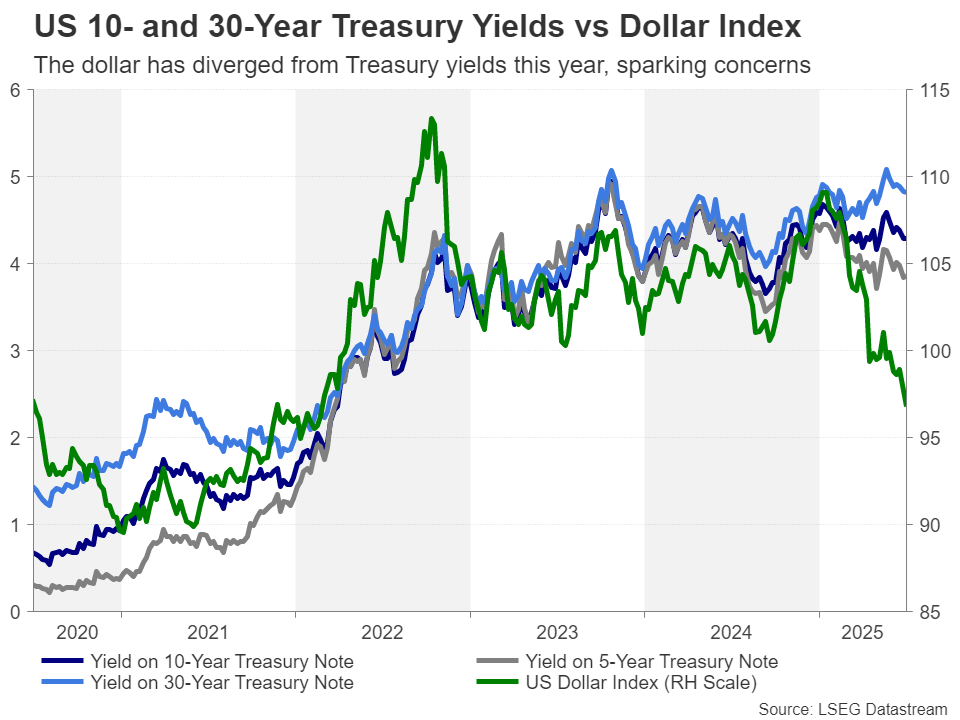

This “risk premium” of Trump’s presidency can be seen quite clearly when looking at the divergence between the US dollar and Treasury yields. The dollar has been in freefall since January, initially tracking the decline in yields. But US yields started to edge up once Trump launched his “Trade War 2.0”, as investors priced in fewer Fed rate cuts on the expectation that higher tariffs will revive inflation. Trump’s radical policies have also dented demand for Treasury bonds, further driving yields higher.

However, despite some jitters in the bond market, it doesn’t appear that demand for US bonds is about to fall off a cliff and Treasury yields have retreated from their recent highs as bond prices have risen. This underscores the perceived low risk of the US defaulting on its debt despite the recent developments.

Are stablecoins coming to the Dollar’s rescue?

One factor potentially helping US yields to stabilize is the recent surge in stablecoins, which is likely fuelling demand for Treasuries. Most stablecoins that are pegged to the dollar require their issuers to hold a certain reserve of US Treasuries, and this is also supportive of the dollar. But this carries its own risks, for example, in the event that issuers need to liquidate a large portion of their holdings, yields could spike higher.

Nevertheless, aside from the 12-day war between Israel and Iran that sparked a flight to safety, primarily towards the dollar’s way, it’s been unable to catch a break this year. Many investors remain deeply bearish about the US currency, even with the tariff war de-escalating significantly in recent weeks.

Trade deals may not offer much hope to Dollar bulls

A crucial test is coming up on July 9 when the 90-day delay of the reciprocal tariffs is set to expire. Trump’s big gamble to renegotiate better trade terms can only go two ways: the US reaches deals with its key trading partners or there’s enough progress to extend the pause, or, the US fails to agree to any substantive trade deals and reciprocal tariffs are reimposed.

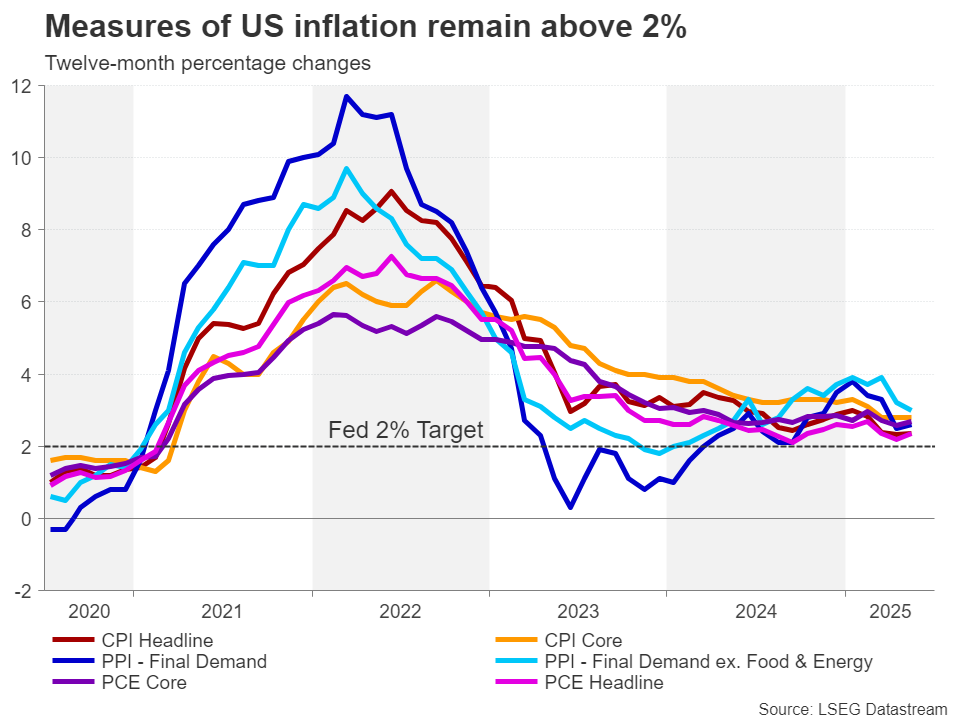

In the first scenario, which is what the markets are betting, trade deals would end the uncertainty regarding future tariffs and in most cases, import duties won’t exceed the universal rate of 10% introduced on ‘Liberation Day’. The Fed has already said that it can overlook the inflation impact of the universal tariffs, as it’s likely to be a one-off temporary increase on goods prices.

Essentially, the upside risks to inflation would recede under this scenario, paving the way for the Fed to resume its rate cuts, and thereby pressuring the dollar. What’s significant here is that the Fed would be unpausing at a time when many other central banks are nearing the end of their easing cycle. Hence, why many investors have turned so bearish on the dollar.

Is stagflation inevitable?

In the second scenario, the absence of trade deals would raise the prospect of tariffs rising significantly above the 10% universal levy on imports from major trading countries, risking a flare up in US inflation. The Fed has already stated that if trade tensions were to escalate again, inflation would be its main priority rather than supporting the labour market.

This would inevitably give rise to stagflationary conditions, where interest rates are kept high to keep a lid on inflationary pressures even as the economy struggles to grow or enters an outright recession.

Historically, currencies don’t tend to benefit from comparatively higher interest rates during periods of stagflation as the benefits are offset by the negative outlook on the economy, making the case for a bearish dollar.

However, this isn’t the only worst-case scenario for the dollar. It’s also possible, although not very likely, that stagflation can’t be avoided even in the situation where trade deals are struck, as the US economy continues to experience sticky price pressures. There are some worries that the Trump administration’s tough crackdown on migrants will generate labour shortages just as the economy is slowing down, pushing up wages, and in turn, inflation.

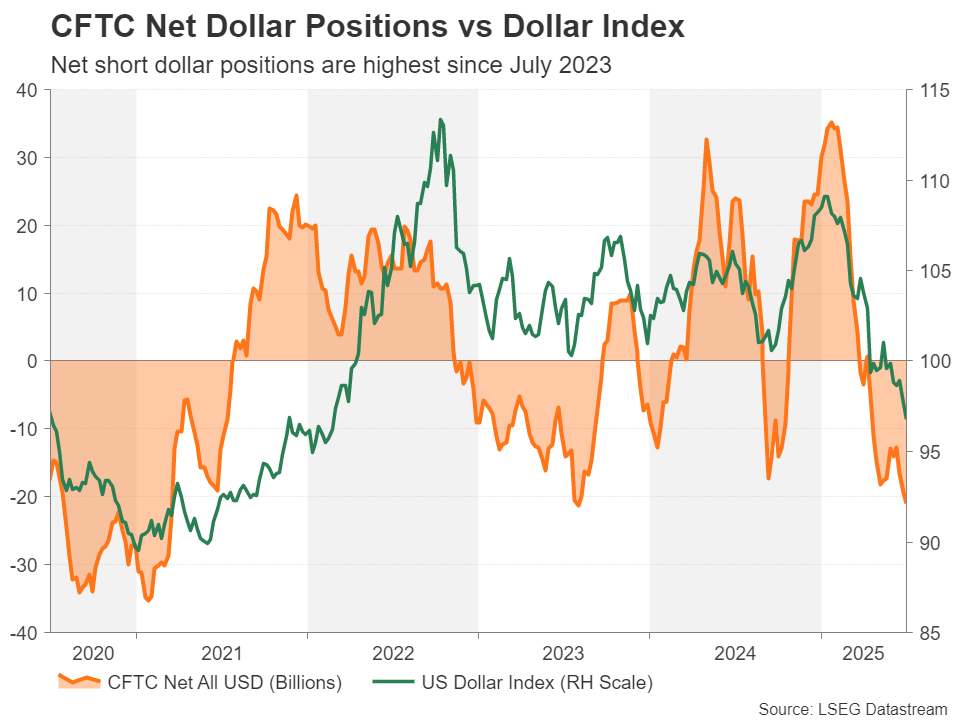

Dollar net short positions highest since 2023

So, it’s an all-round bearish picture for the dollar, whichever way the trade war plays out. The key question now is, how much lower can the dollar go? Large traders are the most bearish on the dollar since July 2023 according to CFTC data, suggesting that the downtrend may be nearing its end. Although historically, the net short positions don’t look too overcrowded.

From a purely technical perspective, the dollar index is displaying some signs of bottoming out, but only in the daily timeframe. In the weekly timeframe, which provides a more longer-term view, the rebound signals are much weaker and there could be a further downward wave to come before it reaches extremely oversold conditions, as the 50-day moving average (MA) is on path for a death cross with the 200-day MA. If the index were to suffer another round of selling, it could go as low as 94.60.

Dollar devaluation may be part of Trump’s plan

The risk going forward for traders who are waiting for a trend reversal will be trying to differentiate between a short squeeze brought on by short covering, and a genuine rebound. The scale of the dollar’s pullback makes it vulnerable to a short squeeze episode, potentially creating a false breakout.

At the same time, those investors who are overly bearish need to consider the fact there are several countries that a too weak dollar would cause significant problems for their own economies. Export-dependent economies such as the Eurozone, Japan, China and South Korea could struggle if the dollar index were to weaken beyond the 90.0 level, potentially prompting some intervention from their part.

Should the greenback continue to slide, it will be interesting to see whether the White House will try to talk up the currency at any point, or keep pressing the Fed to lower interest rates, amid speculation that the Trump administration is deliberately targeting a weaker dollar.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl