Is it time for markets to recover?

US equity markets were notably less volatile on Wednesday and managed to eke out a gain. Although this has not persisted, and US equity market future are pointing to a lower open today, this has led to a subtle shift in the narrative about the state of risky assets. Some investment banks are now calling a bottom in US markets. This is to be expected, it’s been a brutal month for US stock markets. In the past 4 weeks, the Nasdaq is down 11.5%, which is correction territory, and the S&P 500 is down 8%. Mid cap stocks in the US were hit as hard as the Nasdaq, the Russell 2000 is also lower by more than 11%. Key US indices are looking oversold, after breaking through their 200-day smas in recent weeks, which could mean that the end is in sight.

Are recession risks overdone?

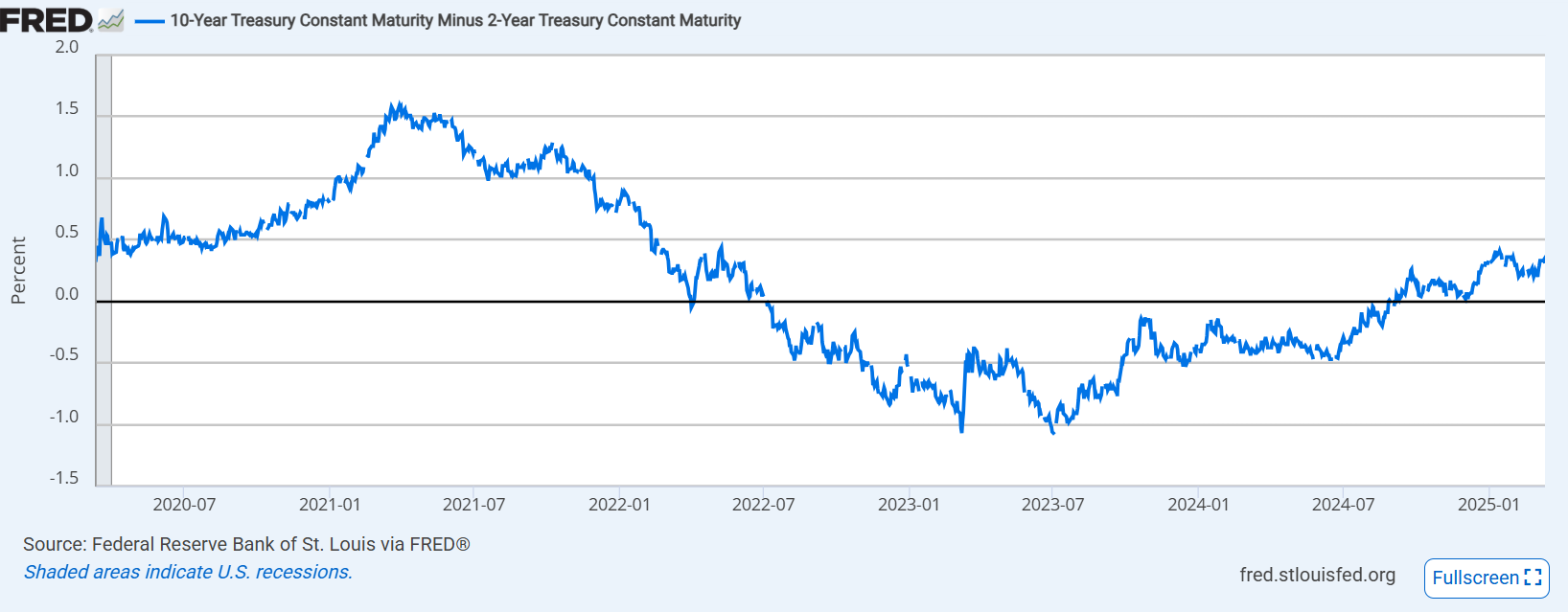

Stocks sold off on the back of tariff fears and rising global uncertainty, but the main driver of the sell off was recession risks. However, although analysts have revised up their probabilities of a recession, the credit market continues to maintain only a small chance of a recession. The US yield curve, which measures the relationship between US bond yields of different maturities, is not flashing a warning signal for recession. The 10-year – 2-year yield curve has been steepening since December 2024. Typically, an inverted yield curve is a sign that a recession could be on the cards. The 10-year – 2-year yield curve is currently at 0.31%, this means that 10-year yields are marginally higher than 2-year yields, which is traditionally a sign of a healthy economy. This is close to the steepest level since 2022, and suggests that bond investors, who are considered the wise owls of the investment world, do not foresee a recession right now.

This is the premise of the view that markets will reach a bottom soon, and the sell off will come to an end. Stock market futures are marginally lower today, which suggests that equity investors remain skittish. However, after heavy losses in February, some big hitters in the market may have been forced to reduce risk in the opening weeks of March, which may have exacerbated the sell off. If the sell off is coming to an end, and recession risks in the US are overblown, we may see the recovery in US mid-caps first.

Chart: US yield curve

Source: St Louis Federal Reserve

The US government shutdown remains a drag on sentiment

However, as one risk fades, another one is rising: the prospect of a US government shutdown. This is weighing on US futures on Thursday and is hindering the prospect of dip buying. The Senate Democratic leader said that his party would block a Republican spending bill that would have averted a government shut down this Saturday. He instead said that the Democratic plan would fund the government through to April 11. This is a sticking plaster and suggests that funding the US’s debt position is going to be a long-drawn-out issue that could weigh on volatility in the current market. The risk is that the government shuts down this weekend, and because of Elon Musk’s DOGE’s attempts to cut Federal spending, the shutdown could be prolonged and adds to pressure on growth and the labour market. These are all hypothetical fears, until they are not. Thus, negotiations in the next two days could be pivotal for market sentiment next week.

Market moves

These are still headline driven markets, and any recovery could be fragile. Ahead on Thursday, the focus will be on US PPI, as the market assesses early-stage inflation pressures. The market is expecting final demand PPI to moderate slightly to 3.3% YoY from 3.5% YoY. The core rate of PPI is expected to remain steady at 3.4%. The big economic data to watch, is Friday’s university of Michigan consumer sentiment and inflation expectations for March. If sentiment falls further, it could hinder hopes of a recovery for risky assets.

European markets are lower today, which suggests that traders are not yet ready to buy the dip. The dollar is higher on Thursday, which is limiting upside for the euro, which has slipped below $1.09. We continue to think that the bias is higher for the euro, however, it is running into stiff resistance at $1.09, as the market scales back some of its expectations for Fed rate cuts. A weaker than expected PPI reading later today, could see rate cut expectations get priced back into the market and weigh on the dollar. We also think that if the strengthening dollar persists, then it could boost US equities.

The gold price is up slightly today, and XAU is currently trading at $2,938. If stocks do recover and the market mood improves, then this could be bad news for gold in the short term. If the market sees recession risks as being overdone, then the oil price may also start to recover. Brent jumped back above $70 per barrel on Wednesday and is extending gains on Thursday morning.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.