Investors see almost 150 basis points of ECB cuts next year

Outlook: Nonfarm payrolls today is forecast at 183,000 (Bloomberg) after 150,000 in Oct. This runs contrary to the scattered signs of limited labor market weakness in this week’s lead-up reports.

We shall find out how bets on early rate cuts will cope with a hot payrolls number. The early-cut gang would rather see something under the Oct number, like 110,000, and indeed this series is choppy enough to deliver any number higher or lower by a sizable amount.

Context and perspective—data on payrolls is not data on inflation. The Fed claims to use inflation and only inflation in making decisions. Projecting inflation on labor market data alone is two steps away from inflation—consumer spending comes in the middle, and to some extent, consumer spending is dependent on wage growth. Payrolls can suggest future wage growth but not dictate it, and wage growth alone does not dictate consumer spending.

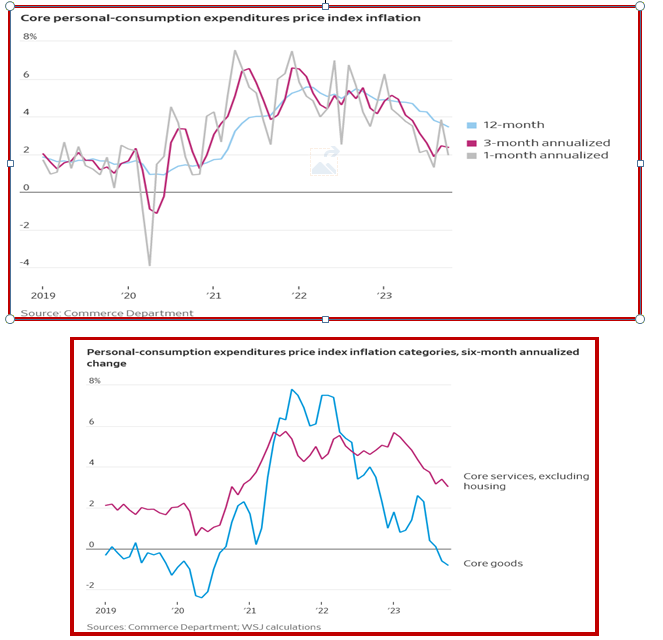

The WJ is helpful in publishing the chart here showing that while core PCE is still highish at 3.5%, the 3-month annualized version is a nice 2.4%. The Fed would have a hard time using 3 or 6-month annualized inflation numbers when the literal dictate is monthly, but never mind—the 3-month might be evidence of how the Fed is thinking. And this little chart shows the early rate-cut crowd is not completely nuts.

At the same time, early cuts and more cuts have been priced into the ECB, too. Bloomberg reports the same second-thoughts as in the US in its latest survey, which shows a pause at the Dec 14 meeting that will hold to June. Then three cuts of 25 bp each. This is a retreat from earlier surveys showing the fitst cut in September.

“The new timetable is still later than financial markets are pricing after inflation in the 20-nation euro zone sank far more quickly than expected — a retreat that hawkish ECB Executive Board member Isabel Schnabel called ‘remarkable.’ Investors see almost 150 basis points of cuts next year, kicking off as early as March. Economists only predict reductions in September and December, after June.” (Aside from the incorrect placement of the word “only,” this lines up with our own estimates for the Fed, although we have doubts about December.)

The other hot news this week was the non-announcement of Japan ending the zero rate policy. This has been building for some time and exploded on what were only hints. Expectations got fast-forwarded to a hike as soon as before year-end. This seems improbable since we don’t get the revised economic projections until the January meeting, and the action itself not until after the turn of the new fiscal year, which is April 1. This runs contrary to a Bloomberg survey showing two-thirds of the economists expect the move by then. The Oct survey had shown less than one-third expected the change in April.

As we see with the rate cut expectations in the US, the rate hike expectations in Japan are premature or to be polite, “leading” the central banks. Central banks issue whispering hints long before they act (usually) in order not to upset the delicate darlings that buy and sell their bonds and the banks that make the loans. The one exception to the long-lead rule is FX intervention, and that has become rare.

Now consider that the US, UK and eurozone will be cutting rates somewhere in March-June while the BoJ will be raising them, or at least letting loose the cap. The result should be a convergence in FX prices, but we can’t count on it being regular and stable. That would be too easy. The BoJ can retreat, the Fed can disappoint, etc. It’s too soon to project the dollar/yen going back to (say) 125—so far.

Tidbit: A newsletter from a former Fed economist delivers updates on the “Sahm rule” that holds you can expect recession when the 3-month average unemployment rate rises 0.50% above the low of the prior 12 months.

Originally built in part to forecast unemployment benefit costs, the rule got blind-sided by the giant truck of the Covid pandemic. The latest work shows it’s not there yet, with a reading of 0.33 but potentially over the 0.50 line if unemployment goes over 4%. One question is whether the rule remains valid after the Covid recovery and structural change in the labor population.

Tidbit: Whatever the nonfarm payrolls today, the cumulative effect of the labor data so far is of a soft landing. We see deceleration but not a contraction. The rate of job creation consistent with population growth is 75,000-100,000 and even the ADP release is over that. Whatever recession-thundering headlines you may see, the labor market is still quite tight and jobs are still plentiful, at least in some sectors if not all of them.

Concerning the labor stats: The FT reports H. Shierholz, president of the Economic Policy Institute and former chief economist at the Labor Dept. has an optimistic view. She says wages come closer to what we seek about inflation than the jobs numbers. “The way to think about wage growth that is sustainable long term is inflation plus productivity growth. So, it’s 2 per cent inflation plus roughly 1.5 per cent trend productivity growth, which means roughly 3.5 wage growth is the target. We are basically there in recent months.”

Far be it for us to quarrel with a top economist, but no. Nominal wage growth is 4.5%. Subtract inflation at what? say 3.5%. That leaves 1% true wage growth. And it gets worse. There is $2.50 discrepancy between what wages should have been and actual wage growth over a long period. Accordingly, workers’ share of corporate income lags. We can assume the data does not include the latest auto-workers’ settlement.

As for the productivity statistics, the BLS delivers them in quarterly format. Productivity was lousy in 2022 at 0.40%. The current number is a wild 4.70%, up from 3.60% in Q2. The long-term average is 2.17%.

Without paying any heed to the niceties of proper statistical work, this means inflation (3.5%) plus productivity 4.70% = 8.20%. This should be wage growth. It’s not. It’s also not long-term. So, long term inflation is what?

Averaging these, we get 3.94%. So, here we go again: inflation (3.94%) plus productivity (2.17%) = 6.11%. That’s the rate at which wages should be rising. And it’s not. Nominal wage growth is 4.5% for the latest quarter and see the Atlanta Fed’s bigger-picture chart. It rose 4% starting in Oct 2021 and reached 6.7% in June 2022, but falling since then. We do not have a long-term average.

This is more down in the weeds than anyone likes, but it makes the point that to blame wage inflation for overall inflation is a dog that don’t hunt. Wages falling short of what the formula shows it should be is inherently disinflationary.

Equally important, it shows how unreliable some modelling can be, whether by the regional Feds or the Economic Policy Institute. If one of the factors in an equation is as jumpy as these inflation numbers, the entire exercise is not useful.

Forecast: The premature and over-the-top rate-cut mania is going to be very hard to break but payrolls today may well deliver some dents. That’s if payrolls are on the high side. A crummy number under Oct’s 150,000 would feed the frenzy.

We see doubts developing in the form of the dollar against some big currencies (pound, euro, Chf) starting to return to the big-picture downmove. This is unreliable and maybe even attributable to fallout from the dollar/yen shock yesterday. Still, whatever payrolls turns out to be, we must expect spikey prices before the dust settles. Those spikes make it very hard to trade currencies on anything more than a 10-minute timeframe.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat