Interest Rates: Ending the Financial Repression Era

Markets seek an equilibrium after years of financial repression but the path to equilibrium means backtracking through the minefields of mispriced real and financial assets based upon administered rates.

Back to Normalization: Part II

Economic fundamentals have been moving since 2016 in the direction of higher economic growth, higher inflation, a weaker dollar and larger Treasury fiscal deficits. In this difficult context, central bankers now wish to move away from an environment of administered prices (interest rates and bond prices). However, for investors the problem is policymakers. Financial markets are moving from one disequilibrium point with interest rates held below market values (and below inflation, see top graph) to generate growth, to another nexus of interest rates, growth and inflation that remains undefined given the uncertainty about the equilibrium of real interest rates, the potential growth rate of GDP and the Fed’s commitment to a two-percent inflation target. Finally, as the year moves forward, we must ask ourselves if the central bank is committed to market-setting interest rates or are we simply moving from an era of close-to-zero interest rates to an era of slightly higher rates, while still being administered by the central bank?

“John Bull Can Stand Many Things, But He Can’t Stand 2 Percent”

For John Stuart Mill, the problem was that “a low rate of profit and interest… makes capitalists dissatisfied with the ordinary course of safe mercantile gains.” That is, capitalists push the envelope of risk to achieve higher returns commensurate with their perceived target or normal rates of return.

For today, the pursuit of yield has taken investors to a very broad range of asset classes where the accurate measure of risk/return has been altered by the low administered interest rates set by central banks.

In recent years, the era of administered rates provided little guidance on what should be the proper level of interest rates to price financial capital and thereby judge the viability of real world activity. As illustrated in the middle graph, sovereign yields in European debt appear remarkably low, and in some cases are below U.S. Treasury yields. Some observers see this as odd. Our view is that these low yields reflect the policy of the ECB in buying both sovereign and corporate debt. But here is the rub. When the ECB normalizes interest rates, what then happens to business finance, real growth and the euro exchange rate? Again, we are moving from an era of administered rates to an era of market rates—or perhaps less administered rates.

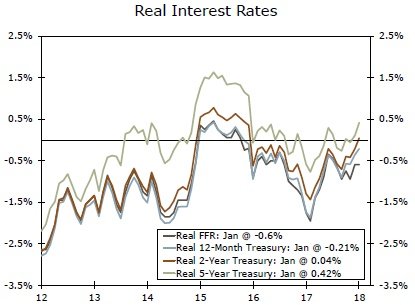

What About Real Interest Rates and Inflation Discounts?

In the bottom graph, we see the pattern of current market pricing for the nominal and real component of interest rates. There is one positive signal here. The rise in the real component is consistent with market expectations for an improved economy since early 2017. In this case, higher real interest rates would be consistent with higher expectations for the real return on capital—a very positive sign indeed.

Author

Wells Fargo Research Team

Wells Fargo