Inside Gold-USD Relationship

As the US dollar rally enters its 4th consecutive week – the longest series of uninterrupted advances since September – the following question needs to be asked? Can the strengthening of the USD continue without any technical breakdown in gold? Or is gold’s stabilisation a red flag for USD bulls? Lets look into the Gold-USD relationship.

Here are a few notes to consider:

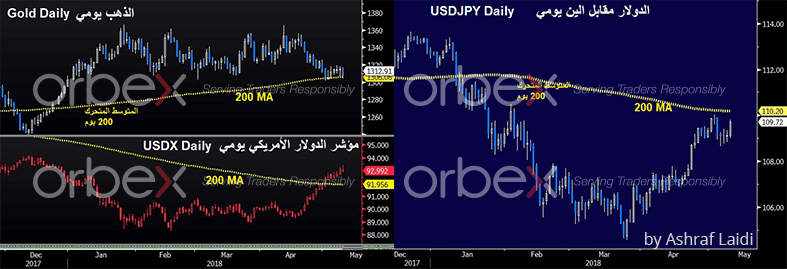

- The US dollar index has breached above its 200-day moving average for the first time in 12 months and continues to do so for the past 7 trading days. Despite that, gold remains above its 200-day moving average as it has done since December.

- The strengthening of the US dollar reflects improvement in US macroeconomic data since mid-April, relative to generally negative surprises in the Eurozone, UK and Japan.

- Do not get me wrong. Gold is weakening as the US dollar strengthens against most currencies. But from a technical standpoint, the trend averages and resistance dynamics continue to hold firm for gold and other commodities.

- In addition to gold, GBP and JPY continue to hold their 200-day moving average against the US dollar (GBPUSD remains above its 200-DMA and USDJPY remains below its 200-DMA). This may well be explained by the fact that the momentum and the trend of this year’s advances in the British pound and yen again have been considerable.

- It can be said that gold’s stabilisation is explained by a neutral to positive inflation expectations in and outside of the US, as well as continued moderate expansion in world economic growth. Copper is down 7% from its year’s high but is up 24% from last year’s lows. Oil is up 14% this year and 43% from last year.

- One explanation to gold’s resilience relative to USD is that the recent pick up in USD momentum had been boosted by the selloff in emerging market currencies, following the fallout in Argentina and selloff in the currencies of Mexico, Poland, Chile, Brazil, Hungary and Turkey.

- Political and economic uncertainty is the aforementioned countries has led to an unwinding of the trades, which initially sought to short USD to benefit from the higher yields in EM currencies. The unwinding may have helped accelerate the rally in USD, without necessarily altering the picture for gold.

- The final and more important factor is related to the Fed. As I have argued last week, the Federal Reserve policy stated earlier this month its commitment to symmetric inflation objective. This means it anticipates inflation to reach the 2.0% target and is willing to allow it to allow it to edge towards 2.5%, just as it has allowed to undershoot to as low as 1.4% last summer. A more relaxed Fed stance towards inflation means it is unlikely to hike rates more than three times this year.

That is good news for gold, and only positive for the USD if US inflation continues to trend over those rates in the rest of the world. But as energy prices end up filtering through the global economy, a more positive inflation outlook has usually proven to be generally in favour of the non-USD complex.

Author

Ashraf L.

CMC Markets

Ashraf Laidi was key speaker at the FXstreet.com International Traders Conference in October 2009 - Barcelona. Ashraf Laidi, Chief Strategist at CMC Markets, author of "Currency Trading & Intermarket Analysis" and founder of AshrafLaidi.