Inflation tracker – Disinflation likely to continue

Headline inflation has stabilised in recent months in the United States, the euro area and the United Kingdom, while it has declined in Japan. Core inflation continues to fall and its decrease is broad-based. Aggregate indicators of price pressures, calculated using PMI surveys, deteriorated again amid longer delivery times linked to the ongoing disruptions to global maritime trade. The PMI input price indices are also up in the US and the UK.

In the euro area, services inflation slipped below 4% y/y in January, but the further decline in the 3m/3m annualised rate to 1.2% points to greater disinflation to come, in line with our current scenario. Disinflation is now well under way in all Eurozone countries. With an inflation rate of 5% and 4.8% respectively in January, Estonia and Croatia were the economies where price increases remained the most pronounced, while four countries recorded a rate of less than 1% (Finland, Italy, Lithuania, Latvia). The ECB's alternative indices, and in particular the PCCI indicator, are falling, confirming the significant slowdown in price increases, as also shown in the chart of generalisation of inflation.

In the United States, most CPI items continued to show declining inflation in December. A third of the listed categories (4 out of 12) posted a level of inflation below their long-term averages (see heatmap on page 8). The core measures for the CPI and the PCE deflator are falling, albeit less markedly for the former (3.9%) than for the latter (2.9%). According to the University of Michigan survey, households' inflation expectations over one year have declined to match long-term inflation expectations (5-year horizon), which have remained stable at around 3%.

The disinflation phase is still less pronounced in the United Kingdom, where almost half of the components of the CPI still showed an annual rate of more than 6% in December. This share stabilised in 2023, in contrast to the euro area and the United States, where it fell sharply. Headline inflation edged down below 4% in December, but the retail price index (RPI) rose more strongly, at 5.2%, underpinned by the jump in mortgage interest payments (+44.1% y/y in December).

In Japan, headline inflation eased to 2.6% in December, on the back of greater energy deflation. However, the increase in food and household goods prices remains significant (6.7% y/y and 6.5% y/y respectively), while the increase in «leisure and culture» strengthened (7.8%). Producer prices, which rose by more than 10% y/y in December 2022, are now at zero inflation. Households' inflation expectations remain highly correlated with the CPI and have logically fallen in tandem.

Chart of the month: The inflationary shock has led to large errors in forecasts

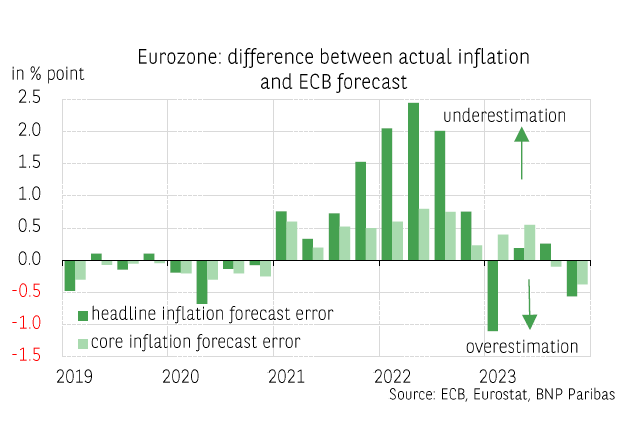

The spike in inflation in 2021 and 2022 surprised everyone, leading to large forecast errors. We are reproducing here a graph coming from a presentation by Philip Lane on the ECB’s forecast errors for euro area inflation[1]. The maximum error of 2.4 points was made in Q2 2022: it corresponds to the difference between the actual headline inflation print for that quarter (8% year-on-year) and the ECB’s March 2022 forecast for Q2 2022 (5.6% y/y). The ECB then continued to underestimate inflation, but less and less so, before overestimating it in Q1 and Q4 2023 for the headline measure (-1.1 and -0.6 points respectively) and in Q3 and Q4 2023 for the core measure (-0.1 and -0.4 points respectively).

It should also be noted that the forecast error is much larger on the headline measure than on core inflation. This illustrates the role played by energy and commodity prices in the rising and falling phases of inflation, as IMF chief economist Pierre-Olivier Gourinchas recalls in his blog post accompanying the latest World Economic Outlook (January 2024) [2]. The IMF’s analysis also shows the role and effectiveness of monetary tightening, through anchoring inflation expectations, in containing rising prices.

For the coming quarters, the question is how quickly inflation will return to the 2% target. Our forecasts differ from those of the ECB: we expect a faster return to the target, as soon as Q2, while the ECB expects it for 2025. Verdict in a few months to find out which forecast will have overestimated or underestimated the trajectory of inflation.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.