Inflation monster rears its ugly head. Will gold beat it?

THIS POST HAS BEEN DEPRECATED

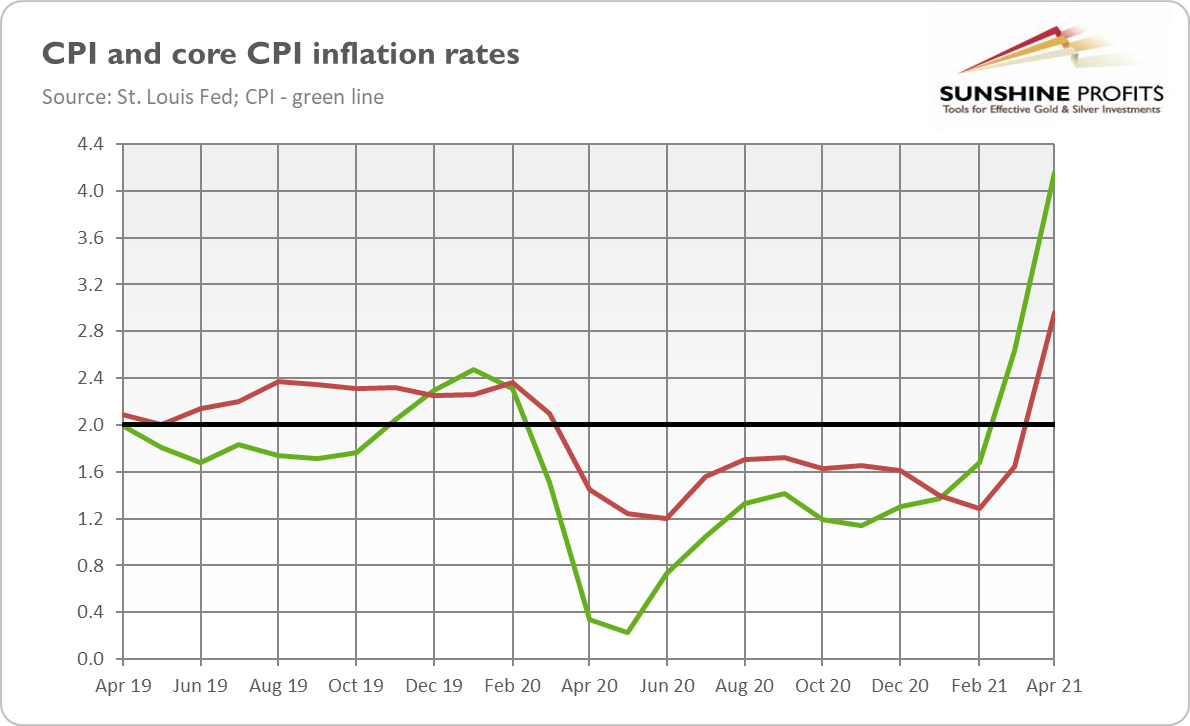

Inflation surged 4.2% in April, but gold declined in response. What is happening?

Unbelievable! The “non-existent” inflation keeps getting stronger. The CPI increased 0.8% in April , after rising 0.6% in March. The pundits cannot blame energy prices for this jump, as the energy index decreased slightly. This shows that the surge in inflation wasn’t caused just by the base effect. Apart from energy, all major component indexes increased last month. In particular, the index for used cars and trucks rose 10.0%, which was the largest monthly increase since the series began in 1953.

As a result, the core CPI, which excludes food and energy, soared even stronger in April, i.e., 0.9%, following a 0.3% jump in March. It was the largest monthly increase since April 1982. But still, there is no inflationary pressure in the economy…

And now for the best part, the true crème de la crème of the recent BLS report on inflation : As the chart below shows, the overall CPI surged 4.2% over the 12 months ending in April , while the core CPI jumped 3.0%. These annual rates followed, respectively, 2.6% and 1.6% increases in March.

So, there was a huge acceleration in inflation last month! The last occurrence of such high inflation was in 2008 during the Great Recession . The quickening was a surprise for many analysts, but not for me. When analyzing the March CPI report , I wrote that it wasn’t an outlier:

What’s important is that the recent jump in inflation is not a one-off event. We can expect that high inflation will stay with us for some time, or it can accelerate further next month.

And indeed, inflation escalated in April. In May, however, inflation could be softer, but it will remain relatively elevated, in my view.

Implications for Gold

-637565153123498811.png)

What happened? Shouldn’t gold have reacted more positively to the surprising speeding up of inflation? As an inflation hedge – it should. But this is far more complicated. First, the bond yields have increased to reflect higher inflation, as traders started to bet that the Fed would have to hike interest rates faster than previously expected.

But the April CPI report won’t force the U.S. central bank to alter its monetary policy and adopt a more hawkish line . After all, they expected acceleration in inflation, and they will simply describe it as a transitory development. As a reminder, the Fed focuses now more on the labor market than price stability – and with employment still more than 8 million short of the pre-pandemic level, the Fed will likely maintain its dovish stance .

Indeed, Fed Vice Chair Richard Clarida reiterated that the U.S. central bank is far away from tightening its monetary policy and confirmed that higher inflation than anticipated won’t alter the Fed’s course, as it would prove to be temporary:

The economy remains a long way from our goals, and it is likely to take some time for substantial further progress to be achieved (…) This is one data point, as was the labor report (...) We have been saying for some time that reopening the economy would put some upward pressure on prices.

What’s more, although traders focused initially on the implications of higher inflation on the federal funds rate and the U.S. monetary policy, in the longer-term gold should come into more favor as a hedge against higher inflation or even stagflation – after all, in April, we witnessed surprisingly disappointing nonfarm payrolls and a surge in inflation. Of course, single reports are not enough, but inflationary risks have definitely risen recently, and we could see some portfolio rebalancing toward gold later this year.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Arkadiusz Sieroń

Sunshine Profits

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017.