Inflation higher for longer? The interplay between productivity, profit margins and pricing power

A complex interplay between unit labor costs, profit margins, and pricing power will determine whether the current increase in inflation will be longer-lasting. Traditionally, in the early phase of recovery, unit labor costs decline on the back of increased productivity. This should cushion the impact of higher input prices on profit margins. Subsequently, unit labor costs should increase but this does not imply that margins should decline. Given the strength of the growth acceleration, the fact that alternatives for meeting robust demand often do not exist, and that going for market share makes no sense when faced with supply constraints, the conditions seem to be met for a rather significant transmission of higher input prices in producer output prices.

Inflation is grabbing headlines. In the euro area, headline inflation has reached 2.0% in May. Although high by European standards, it’s nothing compared to the 5.0% recorded last month in the US, a 13-year high. A key question for households, companies, markets, and policymakers is to what extent this increase will be temporary or not.

Part of the increase is related to base effects – e.g. the huge increase in energy prices –, which will be visible in the annual inflation numbers for several months to come. This could create a perception that inflation has moved higher on a lasting basis. When assessing whether this is an optical illusion or not, monitoring the price level and its change on a quarterly or monthly basis will be more relevant than annual numbers. A priori, the underlying trend of inflation should gradually move higher as sustained growth, underpinned by expansionary monetary and fiscal policy, should reduce economic slack. This applies to the US but it is also the message from the ECB in its latest projections with core inflation excluding the effect of changes in indirect taxes rising from 0.9% in 2021 to 1.2% next year and 1.4% in 2023.

Whether the current increase in inflation will be longer-lasting, thereby lifting the expected path for inflation in the coming years, depends – for a given level of demand – on a complex interplay between different factors. The value of production in an economy corresponds to the sum of profit margins (gross operating surplus), wages, net taxes – the difference between taxes and subsidies- and intermediate inputs. Changes in producer prices reflect changes in profit margins per unit of production, unit labor costs, net taxes, and the unitary cost of intermediate inputs.

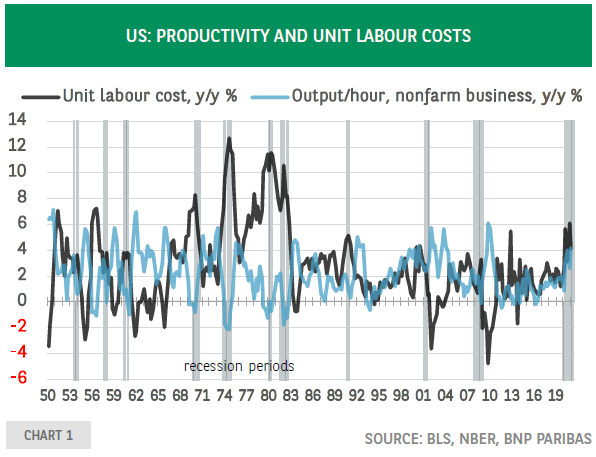

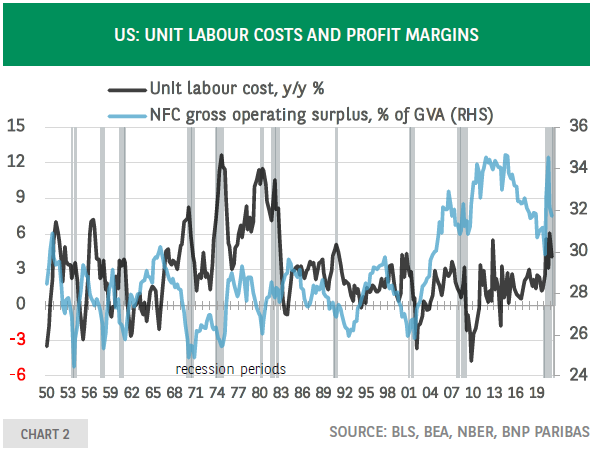

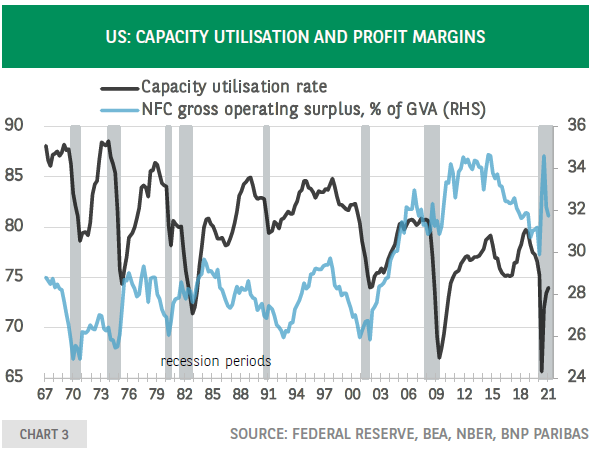

Over the past year, energy has seen a huge price increase and input prices are also up strongly due to supply/demand imbalances. The extent to which this is reflected in higher producer prices in various sectors depends on unit labor costs and unitary profit margins. The former is driven by wages and productivity. The cyclical component of productivity tends to slow in the mature phase of an expansion and decline during a recession before increasing again during the early stages of an economic recovery, whereas wages rise more slowly during recovery due to high levels of labor market slack (chart 1). This implies that, with growth picking up after the Covid-19 recession, the decline in unit labor costs could cushion the impact of higher input costs on profit margins. Chart 2 shows that, historically, after the recession has ended in the US, unit labor costs and unitary profit margins – a gross operating surplus in percent of value-added – tend to be negatively correlated. Later on, during the expansion phase, the relationship is less clear-cut. However, in an economy that is recovering from a pandemic and its restrictions on mobility, the price elasticity of demand will be very low in certain sectors because people are keen to go out again, travel, etc. Accumulated savings is another factor explaining this low elasticity. This offers an opportunity for companies to reflect the increased cost of intermediate inputs into higher producer prices, thereby protecting their margins. This depends on the strength of demand, the existence of alternatives, and the pricing strategy of competitors. Given the strength of the growth acceleration this year, the fact that alternatives often do not exist – e.g. copper in the construction sector, semiconductors – and that going for market share makes no sense when faced with supply constraints, the conditions seem to be met for a rather significant transmission of higher input prices in producer output prices. Subsequently, as input prices stabilize and the relationship between demand and supply normalises, this transmission should decline, under the influence of more intense competition. Another factor that is at play in the early stage of recovery is the fact that profit margins are procyclical, as shown in chart 3. Rising capacity utilization – a proxy for the output gap- is associated with higher profit margins, reflecting increased pricing power and thus contributing to higher prices. Thus far, the analysis has focused on producer prices whereas central banks are focusing on consumer prices. The latter incorporates distribution costs and profit margins for the wholesaler and the retailer. These may dilute the pass-through of a given percentage increase in producer prices in the consumer price index. Pricing strategy also plays a role in this respect considering that research for the US retail sector shows that gross margins (sales minus costs of goods sold as a fraction of sales) “are relatively stable over time and acyclical or mildly procyclical”.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.