Indonesia may have stabilised the Rupiah, but the bigger fight is not over

Bank Indonesia’s emergency rate hike has bought the Rupiah some time, but the currency’s hesitant response suggests it has not yet restored confidence. Can higher interest rates solve the Rupiah’s problem, or do the country’s challenges run deeper?

Indonesia's central bank took the unusual step of raising interest rates between scheduled policy meetings last week, delivering an emergency 25 basis point increase in an effort to halt the rapid decline of the Rupiah.

The move initially appeared to work.

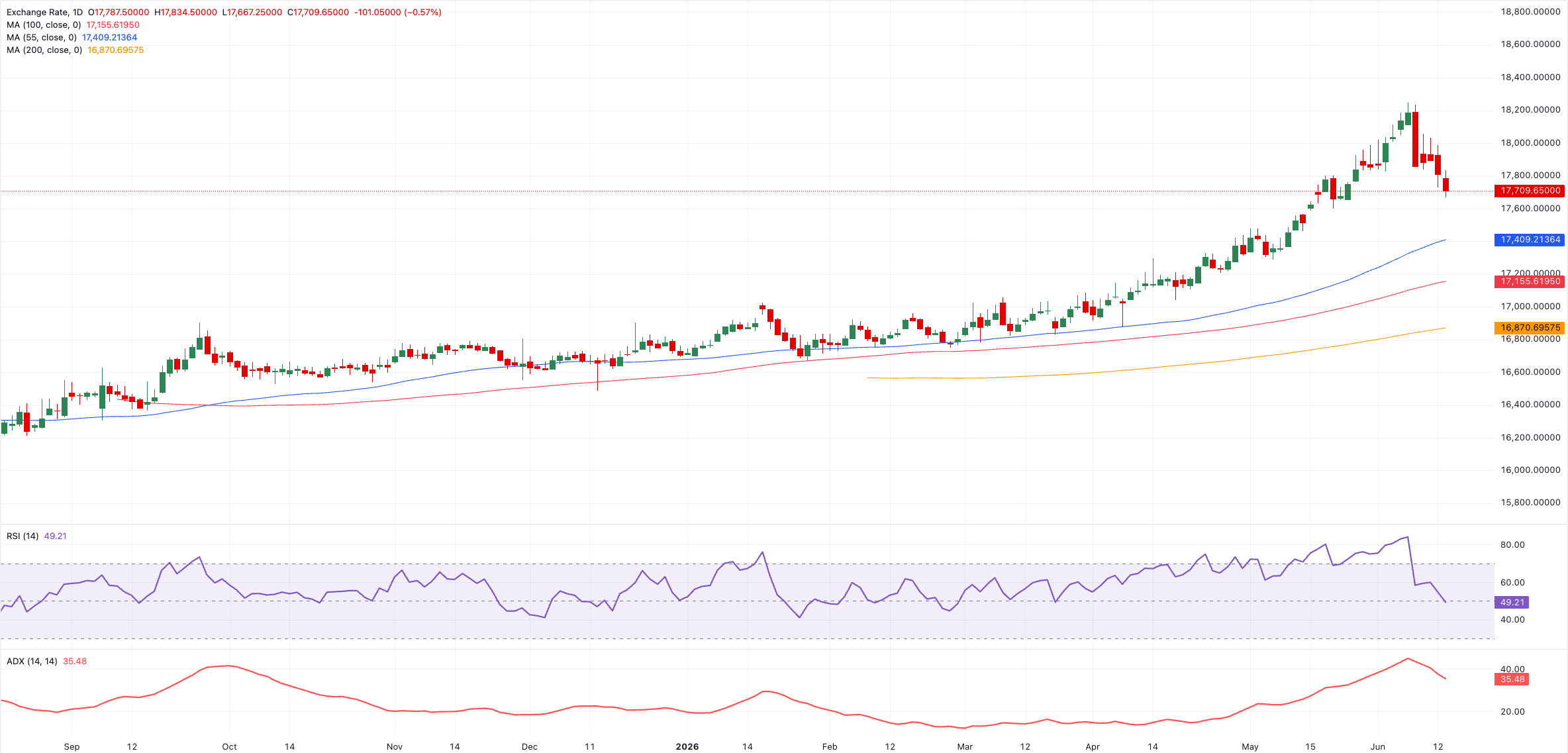

The Indonesian currency strengthened sharply after the announcement, recovering from record lows near 18,200 against the US Dollar. However, the relief is still needed to prove its sustainability, with USD/IDR hovering around the 18,000 region as investors continue to question whether higher interest rates alone can solve the country’s challenges.

That may be the most important takeaway from the surprise decision.

Why did Bank Indonesia act?

According to Bank Indonesia, the emergency move was designed to stabilise the Rupiah amid heightened volatility linked to the conflict in the Middle East and broader global uncertainty.

The currency has been under intense pressure for months.

Despite a 50-basis-point rate increase in May and repeated intervention in FX markets, the Rupiah remains one of Asia's worst-performing currencies this year, having lost around 8% against the US Dollar.

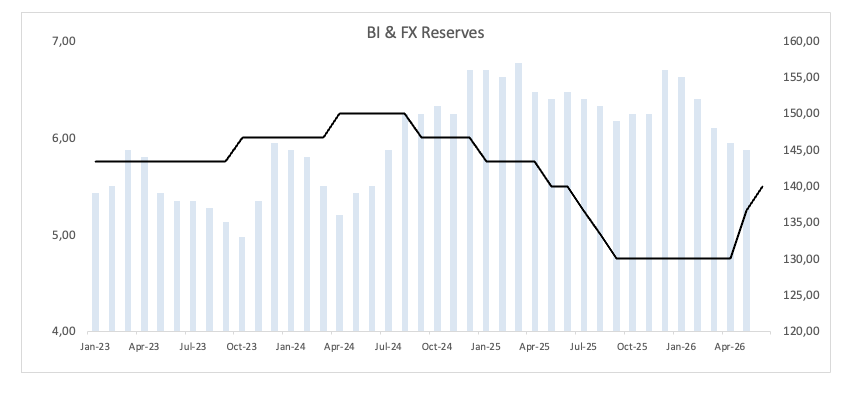

At the same time, the central bank's foreign exchange reserves have been steadily declining as policymakers attempt to slow the currency's fall. In May, those reserves dropped to the lowest level since July 2024 at around $145 billion.

That combination appears to have convinced officials that stronger action could no longer wait until the next scheduled meeting.

A currency problem or a confidence problem?

The emergency hike highlights a growing concern among investors.

Higher rates can be a good support for a currency, making local assets more attractive, but they are not a cure-all.

The Rupiah failed to sustain early gains, showing markets may be focusing on wider issues than just monetary policy.

Investors are monitoring Indonesia's fiscal outlook, capital flows and longer-term growth prospects, with some analysts saying it will take more than higher borrowing costs to restore confidence.

In other words, the challenge facing Indonesia may be evolving from a currency story into a confidence story.

The bond market is sending a message

One signal came from Indonesia's bond market.

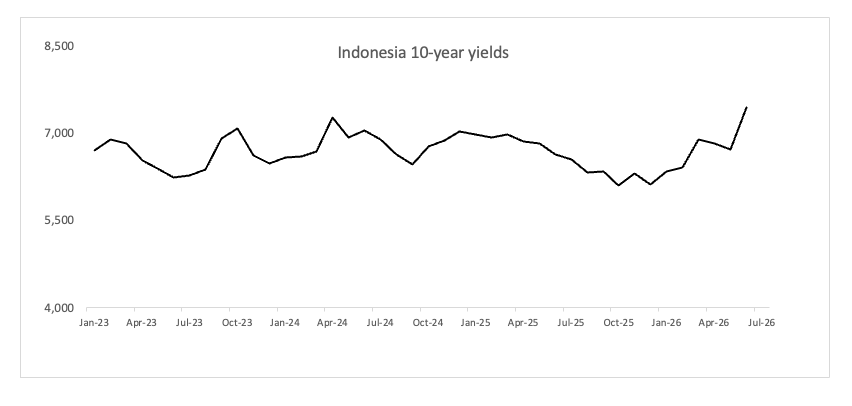

Yields on 10-year government bonds reached their highest levels since late 2022 after the surprise decision.

Normally, a rate hike aimed at defending a currency should reassure investors.

Instead, rising bond yields suggest markets are demanding additional compensation for holding Indonesian assets, a sign that concerns about the broader outlook have not disappeared.

That does not mean investors expect a crisis.

But it does suggest confidence has not fully returned, despite an aggressive response from the central bank.

What happens next?

The next few weeks could prove crucial. The temporary peace agreement between the US and Iran is expected to ease immediate pressure on central banks, including Bank Indonesia, to raise interest rates further, but it remains to be seen whether that’s enough.

Investors will be closely watching whether the Rupiah can stabilise below the psychologically important 18,000 level against the US Dollar and whether pressure on FX reserves begins to ease.

If the currency continues to weaken despite higher interest rates, markets may start to question whether they will need further tightening or additional measures.

For now, Bank Indonesia has bought itself some time. But whether it has restored confidence is a very different question: judging by the Rupiah's hesitant reaction after the emergency move, investors are not yet fully convinced.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.