Import surge leads US trade deficit to balloon in April

Summary

The US deficit in international trade widened sharply in April amid a surge in imports. Extracting precise trends from the monthly data is challenging given volatility, but we believe this sharp widening somewhat overstates the current trade deficit.

Deficit may be smaller than it appears

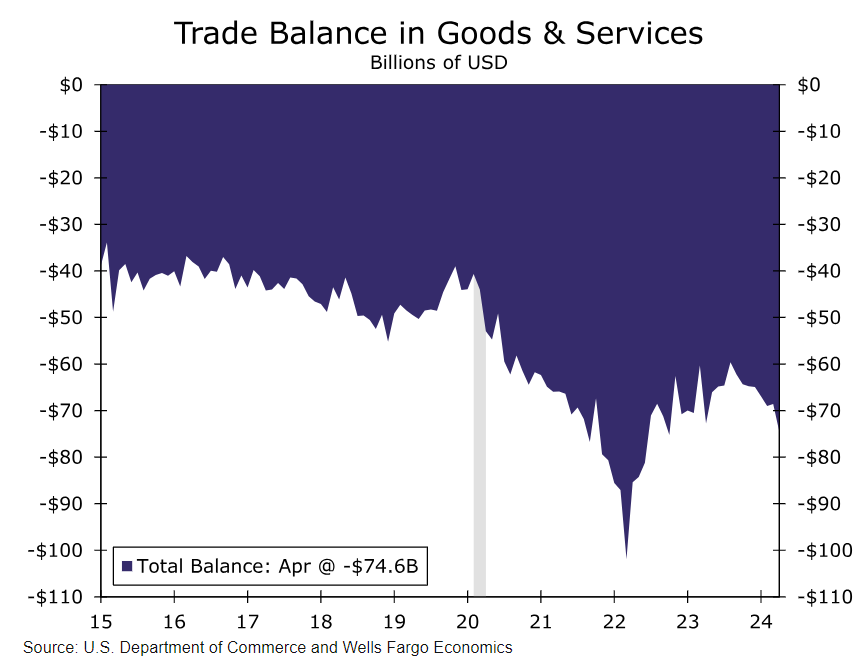

The U.S. international trade deficit widened sharply in April. The balance declined by nearly $6 billion, marking the largest one-month contraction in a year and pushing the overall balance to a deficit of $74.6 billion. Such large monthly swings in the deficit are not completely unusual, but the volatility has increased in the wake of the pandemic. Consider that the trade balance's average monthly change, in absolute value terms, was $2.4 billion in the four years leading into the pandemic. That nearly doubled in the past four years to an absolute average of $4.6 billion. Monthly volatility leaves the data noisy, meaning it can take a few months before discernable trends appear.

U.S. exports rose $2.1 billion in April, led higher by goods exports specifically, but that gain paled in comparison to imports, which rose four-times as fast as exports, surging by $8.0 billion. This outstripping of exports by imports is what caused the overall trade deficit to sharply widen.

As seen in the nearby chart, the deficit now sits at its widest point since October 2022, but given how sharp of a decline we saw in the balance and some relatively concentrated strength in imports, we expect this outturn may overstate the current trend.

Digging into the details, consumer goods imports slipped 0.3% in April. The softening was foreshadowed by downward revisions to consumer spending on durable goods over the past few months. Most types of consumer goods imports fell over the month, while medical, dental and pharmaceutical preparations posted a 12% increase (+$2.3 billion) on the heels of a double-digit percentage point gain the prior month. If we strip out this component from total consumer goods, then consumer goods imports would have contracted 5% in April. The outturn underscores that the household sector is pivoting away from discretionary items amid the challenging interest rate environment and persistent inflation.

While elevated borrowing costs are starting to squeeze personal consumption, demand in the factory sector has shown some recent signs of stabilization. Durable goods orders have risen for three straight months, with notable strength in transportation equipment, computers and electrical equipment. Strengthening orders in these categories corroborate with the 3.1% gain in capital goods and the 10.4% jump in automotive vehicle imports in April.

Computers and accessories together accounted for 67% of the gain in capital goods imports last month. And, as alluded to previously, if it were not for a surge in pharmaceutical preparations, consumer goods would have slid by about ten-times as much. Together these categories accounted for nearly half of the gain in imports last month, demonstrating some concentrated strength.

The largest dollar gain on the exports side was in capital goods, which rose $1.9 billion in April. The data were somewhat broad based, but the two notable standouts so far this year (civilian aircraft engines and computer accessories) gave back some ground in the month. Consumer goods exports were also fairly strong, with the largest monthly change in 15 months, as exports were also partly lifted by the pharmaceutical preparations category.

Industrial supplies were the weak spot, slipping for the third time in four months and marking the largest drop at $1.0 billion of any major export category. What stands out to us is the 35% tumble (-$369 million) drop in metallurgical grade coal, the largest decline after non-monetary gold. While commodity trade can be very volatile, we expect this decline is related to the partial closure of the Port of Baltimore after the collapse of the Francis Scott Key Bridge in late March.

Baltimore is a major coal exporter on the Eastern Seaboard, with coal previously being the largest export category (measured by tonnage) at the port and representing around a 20% share of the port's exports each month. It's also a key player for the entire country. Prior to its closure, nearly a quarter of all U.S. coal exports (NAICS 270) left from the Port of Baltimore. Last month, the port accounted for just 0.7% of U.S coal exports by value. Until the port is operating normally, we expect to see delays and disruptions with key products. But with other options available, like nearby entry points at the Ports of Charleston, Norfolk and New York/New Jersey, this supply challenge is less severe, on a macro level, than those that occurred amid the pandemic.

Author

Wells Fargo Research Team

Wells Fargo