How to trade the ECB rate decision

This is the base case for the ECB decision:

-

Deposit rate to be left unchanged at -0.5%.

-

PEPP purchases to be kept unchanged as 85 billion euros in 3Q.

-

Balance of risks to be skewed to the downside.

Going into this event it had been expected (around a couple of weeks ago) that this might be the meeting where the ECB announce bond tapering. However, a flurry for ECB speakers leading up to the blackout period has caused these expectations to subside. The general mood music is that the ECB is going to keep bond purchases as they are. However, there is still a chance of a bullish twist and there is an interesting piece on this from the financial source team.

They make the point that the detail is going to be interesting here. In particular, what happens around the upgrades to growth and inflationary. Now interestingly Bloomberg is expecting the ECB’s staff economists to keep the forecasts unchanged. However, a recent run of decent data could lead to a skew in the upgrades. Here are the charts that FS highlights.

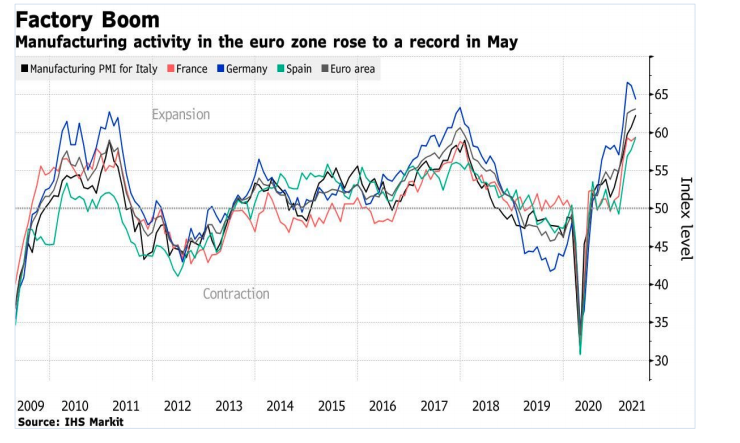

European Market PMI’s hit a record high last week.

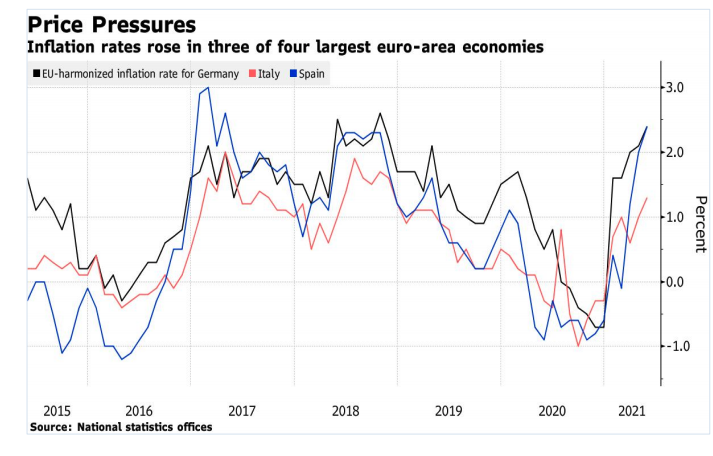

Inflationary pressures building.

German bund yields dropping from recent highs after ECB members take a more dovish stance.

So there is a chance that the ECB could upgrade its growth and inflation projections. However, if they do that runs counter to its ‘now is not the time to taper’ message. The general global background is that economies are more optimistic about economies opening up and a strong global vaccination program.

The takeaway

The main tradable opportunities are:

-

The ECB does taper. Clear EUR buy.

-

The ECB could ‘reduce their PEPP purchases as part of a summer lull’ by reducing purchases in July and August. This may be wrongly construed as ‘tapering’, so would be choppy euro action. Possibly a EUR spike higher and retracement.

-

Changes language to risks being ‘more balance’ (as opposed to ’skewed to the downside). EUR buy.

-

Changes projections for economic upgrades. EUR buy.

This is just a rough guide, but it flags up the major issues ahead of the ECB rate meeting.

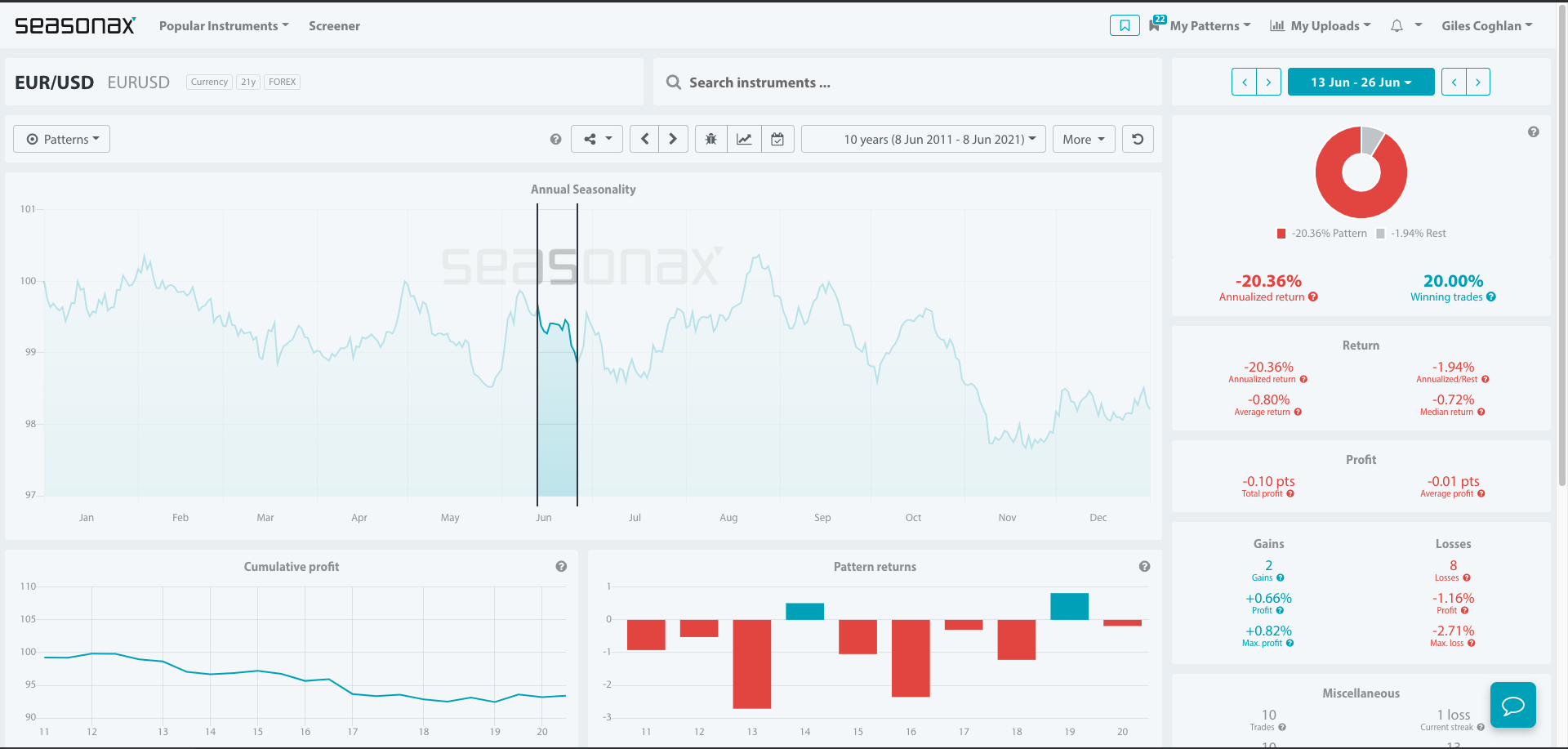

Some seasonals for the EURUSD.

The EURUSD does see some seasonal weakness at this time of year too. Over the last 10 years, the EURUSD has lost value 8 times between June 13 and June 26. The largest loss was in 2013 with a -2.71% loss. This was accelerated by the Fed’s taper tantrum with the effects still being felt. A clearly bearish ECB bias could be a great opportunity to benefit from a time of seasonal weakness too.

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.