How high can GBP/USD fly?

The star of this week has been GBP/USD. The currency pair is set to end the week higher by 3%, that would be the biggest weekly gain since February 2016.

Inflation is overtaking Brexit as the priority

Bank of England [BoE] kept the rate hike talk alive as expected after August CPI printed at 2.9%. According to the minutes of the BOE’s latest meeting, a majority of its nine policy makers judged that “some withdrawal of monetary stimulus was likely to be appropriate over the coming months in order to return inflation sustainable to target” if the economy develops as they anticipate.

The Bloomberg report says, "the BOE already sees some signs of a modest pickup in wage growth, and that could build after Prime Minister Theresa May said she’ll relax a cap on some public-sector increases."

BOE dove turns hawkish

The bid tone around the British Pound strengthened today after BOE's Gertjan Vlieghe, an external member of the Bank of England’s Monetary Policy Committee, despite having voted yesterday to hold rates at an all-time low of 0.25%, said rates could rise in the “coming months”. Vlieghe, renowned dove, went a step further and said that the MPC was unlikely to stop at one rate rise.

The U-turn by Vlieghe clearly indicates that controlling inflation is a priority for the BOE.

Market reaction

- GBP/USD hit a post Brexit vote high of 1.3616

- Ten-year gilt yields are set for their biggest one-week jump since June 2013

- Yields on two- and five-year gilts hit their highest level since the Brexit vote

- Traders now see two rate hikes next year, and have ramped up the odds of a November increase.

Will BOE walk the talk?

Hawkish comments from the one-time dove, Vlieghe does suggest that the BOE is indeed preparing the markets for a lift-off. However, November seems too early. Markets risk running ahead of themselves as the central bank is unlikely to raise rates before Feb 2018.

Moreover, the bank would want to assess the impact of indirect tightening conditions [due to appreciating exchange rate] on the economy before hiking the interest rate.

Reflation trade unlikely to derail the GBP/USD rally

A surge in industrial metals prices and the Australian dollar at the end of July, boosted hopes that China can reinvigorate the so-called reflation trade.

The case for the revival of the reflation trade strengthened after China reported a pick up in the PPI. Note that it was the rebound in Chinese PPI in July/August 2016 that set the ball rolling. Trumpflation was just an icing on the cake.

The speculation is gathering pace that China will end up reigniting the US inflation expectations as it did in Q3/Q4 2016. If so, the US dollar would strengthen as USD is an inflation play. Moreover, pick up in inflation expectations in the US would mean the Fed could maintain the gradual pace of tightening.

However, it is unlikely to derail the GBP/USD rally as it is widely believed that the Fed is ahead of the curve and nearing the new normal interest rate level of 2%. Thus, it is likely to prioritize balance sheet normalization, which is seen happening at a glacial pace.

Fed tightening is old news. Markets are more likely to respond to the increased odds of a a BOE rate hike. Bullish-to-bearish trend reversal could be seen if something goes wrong with Brexit negotiations or the Fed tapers balance sheet at a faster rate.

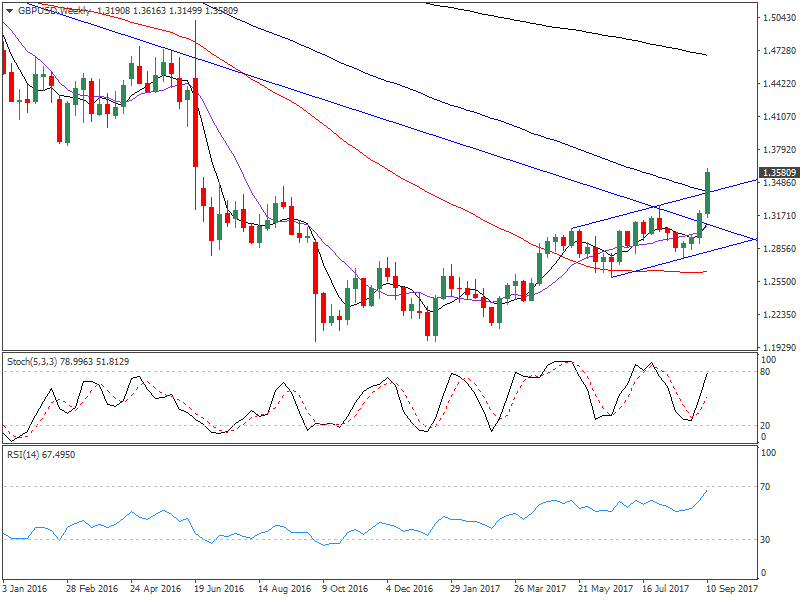

Weekly chart - Bullish break of the rising channel

Breach of the falling trend line last week, followed by a move above the weekly 100-MA and an upside break of the rising channel points to major bearish-to-bullish trend change.

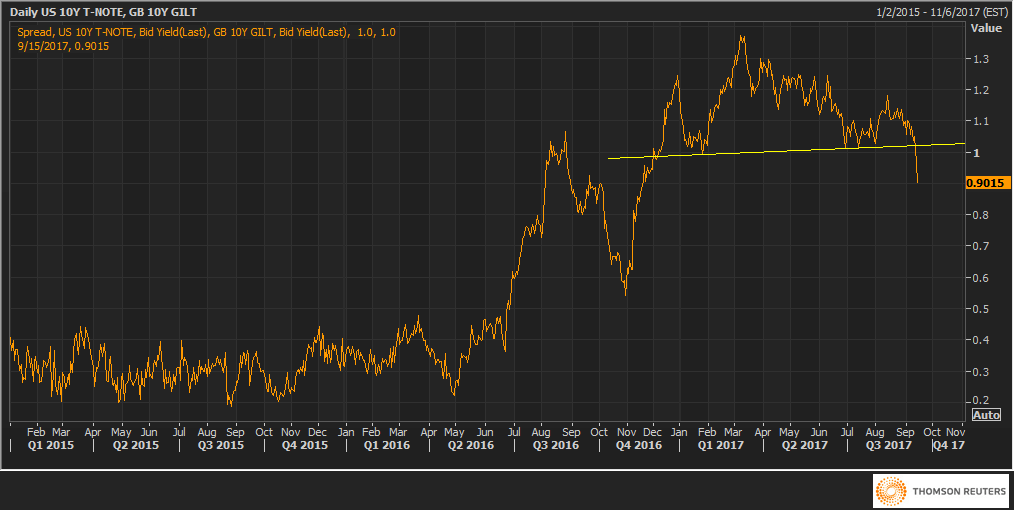

US-UK 10-year Yield spread adds credence to the bullish reversal in Pound

The head and shoulders breakdown [bearish reversal] on the US-UK 10-year yield spread chart indicates the spread is likely to narrow further in favor of the GBP, i.e. GBP/USD is likely to remain well bid in the near-term.

Risk reversals spike

The thee-month 25-delta risk reversals indicate increased demand for bullish bets, i.e. Call options. The sentiment is clearly bullish.

Overbought in the short-term

A technical correction cannot be ruled out as the daily RSI and Stochastics are overbought.

View

- A pullback to the downward sloping weekly 50-MA cannot be ruled out, although bullish-to-bearish trend change is likely only if the spot dips below 1.32.

- A technical pullback followed by a break above 1.36 would open doors for a more sustainable rally to 1.3835 [Feb 2016 low].

Author

Omkar Godbole

FXStreet Contributor

Omkar Godbole, editor and analyst, joined FXStreet after four years as a research analyst at several Indian brokerage companies.