How bad management of currencies impacts markets

Outlook:

On the US calendar today is Nov PPI, likely to have the same market effect as yesterday's CPI—none. CPI was 1.2% in the headline and 1.6% in the core. Today PPI is forecast at 0.2% or 0.7% y/y and 1.2% in the core. Some hardliners persist in expecting higher inflation in the coming year as recovery gets a grip, but not yet. We await the University of Michigan survey of long-term inflation expectations, which is reported alongside the flash Dec sentiment index (forecast at 76 from 76.9).

We rank institutional factors at the top of the list of factors influencing FX prices. This is almost always the central bank and its responsiveness to inflation and/or recession. Most analysts shy away from any consideration of other forms of governance, especially anything smelling of politics, even when the politics are central to the economic outlook (think of the last Italian election). Politics rears its ugly head in the Hungary/Poland blocking of the EU budget and in the US, Republican party obstructionism in the name of power to the donors.

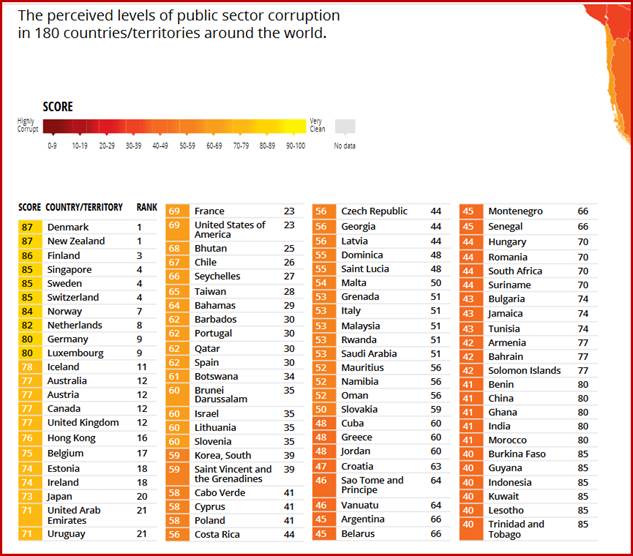

Rarer still is any comparison of plain, old-fashioned managerial competence. Critics of the eurozone like to bash Brussels for bureaucratic stupidities, but on the whole, we may measure corruption and other issues, but no gold stars for management. On the subject of corruption, Denmark, New Zealand and Finland are the cleanest; the UK ranks 77th (of 180) and the US, 69th. We'd guess is behind the times when it comes to evaluating corruption in the US today.

We all knew Trump was an incompetent manager—just look at his collection of not "the best people." Three cabinet secretaries were kicked out for corruption, not to mention all the campaign people who went to jail and the impeachment itself, based on an effort to strongarm a foreign leader into election interference. Trump botched the pandemic response and even how much vaccine to order, so that now we face a shortage. To pretend this mismanagement is not affecting the economic consequences is short-sighted, to say the least. Former Fed chief Volcker wrote his last book on the need for professional management in government.

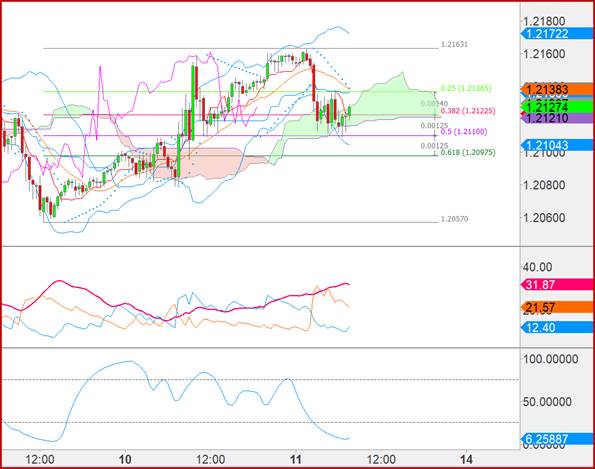

We guess the contrast between obvious bad management in the US and far better management in the EU and ECB is the reason the euro took off to the upside yesterday. There was nothing really new in the ECB decision and all of the new measures should have been fully priced in, but the euro rallied 100 points on the news anyway. To be fair, profit-taking emerged right away but the euro gave back only 50% and as of 6:30 am ET is already on the rise again. See the 30-minute chart.

The US authority to pay for government ends at midnight tonight. The House has passed a continuing resolution and the Senate is expected to pass it today, but to toy with a government shutdown because politicians are pig-headed in the biggest economy in the world is downright stupid. It stinks of bad management. An arm-twister like Lyndon Johnson or Ronald Reagan would never have let such a thing happen. Granted, we have had shutdowns before and the republic survives, but when the Treasury Secretary is pettily stashing cash out of reach during a pandemic and a recession, bad governance is not confined to the Congress.

Fans of Biden believe competence will return on Jan 20, but that's not realistic. Not only do the Dems get themselves tangled up in identity politics and political correctness, they face a formidable counterweight in the form of all those obstructionist Plubs in Congress and seeded throughout the Establishment in thousands of jobs. Hilariously, two agencies are already showing some mettle—the Environmental Protection Agency and the CDC/FDA.

The effect of bad management on currencies tends to be marginal except in the most extreme cases (Argentina, Turkey). We are not proposing that bad management in the US and UK and seemingly better management in Europe has a lot to do with the fate of the dollar, pound and euro but it has something to do with it. Both Trump and Boris are buffoonish; nobody in Europe today gets that label. So here's the hypothesis: risk assessment is about to change. We grew accustomed, starting pretty much with Grexit, to judging risk appetite and risk aversion on the grounds of the institutional factors. The very existence of the eurozone and the euro was in doubt. Noble laureates wrote books on how badly organized the very concepts were (Stiglitz).

We struggled for a few years with interpreting geopolitical events as currency-relevant, including war. But then it morphed into the Trump years where uncertainty over an erratic leadership triggered flight to safety, with nobody missing the irony of the cause and paradoxical effect. In a nutshell, we need a new model of what can and should drive perception of risk. The obvious candidate is the government response to the pandemic. The US is the worst responder of the majors, with the UK not far behind, and Australia and Japan are the best responders. It seems fairly clear that economies will follow how governments deal with the pandemic; even if restaurants and nightclubs are closed, factories will still be running and it's things like industrial production and purchasing manager indices that we examine. This is the sense in which China's draconian measures were correct—the economy is roaring again.

We tend to think that the US has a more robust and responsive economy than the UK or Europe because of the entrepreneurial spirit, but that can't get unleashed until we have vaccines and herd immunity. Realistically, plenty of other countries are going to get recovery ahead of the US. It's not inconceivable that if we watch the Covid data, we will be able to find a strong correlation between disease recovery and economic recovery across countries. If so, dumping dollars remains the right strategy for another few months at the least.

US Politics: We thought the Supreme Court would rule on the Texas challenge to the Pennsylvania voting process, but apparently there is no set schedule. Many more states have joined Texas (for a total of 18) and yesterday a slew of members of the House (106 at last count), to the disgust of the few. That means 90 Republican members did not give in to Trumpian arm-twisting.

CNN reports "Each of the four battleground states targeted by a Texas lawsuit seeking to overturn President Donald Trump's election defeat issued blistering briefs at the Supreme Court on Thursday, with Pennsylvania officials going so far as to call the effort a "seditious abuse of the judicial process." The court filings from Georgia, Michigan, Pennsylvania and Wisconsin come a day after Trump asked the Supreme Court to intervene in the lawsuit brought by Texas Attorney General Ken Paxton seeking to invalidate millions of votes in their states. The lawsuit amounts to an unprecedented request for legal intervention in an election despite there being no evidence of widespread fraud."

More than 20 other states and Washington, DC also submitted an "amicus" brief to the Supreme Court ridiculing the very idea of one state trying to dictate how another state can run its elections. Texas has no standing and can't show it has been harmed. More importantly, the Texas case is "legally indefensible and is an affront to principles of constitutional democracy." More states (20) oppose the case than support it (18), but it's doubtful the Supreme Court is taking that into account. It's the law that counts.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat