Hardly anyone thinks the Fed will hike in September

Outlook:

We get important data today in the US, including retail sales, final demand PPI, industrial production and cap utilization, the Philly Fed manufacturing index and the usual weekly jobless claims. No wonder traders want to pare positions. Retail sales is probably the biggie, especially if it's a loss, as forecast, if by only -0.1%. Ex-autos, retail sales should be up 0.3%.

The danger is whipsaws in various prices if traders' nerves get too frayed. Analysts say some trades are too "crowded," meaning too many traders holding the same position and jumping off the bandwagon at the slightest bump in the road. We see this all the time in FX but it tends to be less common in the bond market.

But no more. The WSJ reports "Investors yanked $1.9 billion out of government bond funds in the week ended Sept. 7, according to strategists at Bank of America Merrill Lynch, marking the largest weekly outflow in six months. Exchange-traded funds tracking long-dated bonds received $5.3 billion of net inflows in the first half of the year, according to data provider HIS Markit... but long-dated bond ETFs are on track for their heaviest month of outflows since May 2015, when investors briefly fled govern-ment debt as Germany's bond yields rose following a long decline."

Besides, corporations have been taking advantage of low rates and have flooded the market with new issuance, $48.43 billion in just the latest week, the most since May. This has the effect of pushing yields up in Treasuries, although the appeal of Treasuries is falling all on its own, as shown by the lousy indi-rect bid at the last 10-year auction (54.8% vs. the average of 65.4% for the previous eight auctions) and 57.9% for the 30-year on Tuesday, the lowest since January.

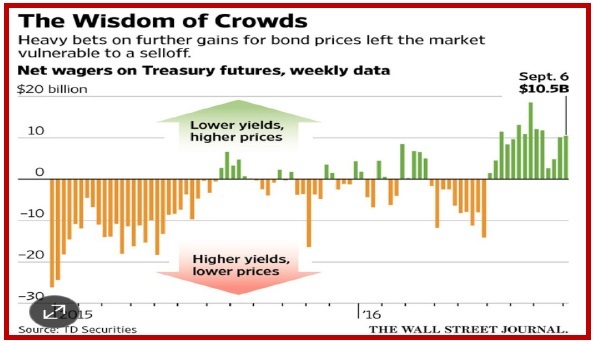

We have the conditions for a reversal and yet many say this is just a temper tantrum—an overreaction to mostly imaginary developments. See the WSJ chart. The WSJ asks "Is the bond bubble bursting? Supposedly safe government bonds have sold off aggressively in recent days, in what looks like a clas-sic correction of overextended prices. While investors watch every twitch from central bankers—with even the timing of a speech moving the market this week—the bond market's lack of interest in the economy is worrying." Again, analysts note there is no actual catalyst (like Lehman).

The bond gang has long believed economic conditions are going to be grim more or less forever, mean-ing no inflation anywhere in sight. But can we really believe in secular stagnation and that central banks are not only lower-for-longer, but lower-forever? Bloomberg cites a report from JPMorgan Chase saying the latest sell-off is exactly like the "taper tantrum" in 2013. This is a function of over-positioning rather than good economic analysis. Traders had excessive long positions in long-dated sovereign paper. If you don't like the longer-term outlook, go shorter-term. The 5-30 year yield curve has been steepening for 9 straight days, the longest such streak since 2012.

The US yield curve hit its steepest in over two months yesterday, according to Reuters. Hardly anyone thinks the Fed will hike in September, so this is a preview of what to expect when the Fed does actually move, presumably in December.

We wouldn't dare to opine on whether the bond market is overpriced and a bubble, or whether the sell-off is a temper tantrum or the shape of things to come. What we do know is that the overall data on the US economy is a B-minus. Some imagine it should be A+ to justify a hike but Yellen & Company seem to think B-minus is nice and will suffice. The problem is the classic overreaction to bad data (dollar-negative) and asymmetrically lower reaction to good data (should be dollar-positive but usually fails). For example, the last time we had a sub-par outcome in retail sales and also in industrial produc-tion, the dollar fell more than it had risen on other good data, like payrolls. This means we are not opti-mistic about today's outcomes, but you never know—it's up to the bond boys. FX traders may prefer to buy dollars on some good data but feel forced to sell if the bond boys don't see it the same way. Con-sidering that everyone is a little nuts this week, the wise course of action is retreat.

| Current | Signal | Signal | Signal | |||

| Currency | Spot | Position | Strength | Date | Rate | Gain/Loss |

| USD/JPY | 102.37 | LONG USD | NEW*STRONG | 09/14/16 | 102.73 | -0.35% |

| GBP/USD | 1.3231 | LONG GBP | STRONG | 09/02/16 | 1.3101 | 0.99% |

| EUR/USD | 1.1248 | LONG EUR | WEAK | 09/12/16 | 1.1223 | 0.22% |

| EUR/JPY | 115.16 | LONG EURO | WEAK | 09/02/16 | 115.83 | -0.58% |

| EUR/GBP | 0.8501 | SHORT EURO | WEAK | 09/02/16 | 0.8426 | -0.89% |

| USD/CHF | 0.9736 | SHORT USD | WEAK | 09/07/16 | 0.9693 | -0.44% |

| USD/CAD | 1.3203 | LONG USD | NEW*STRONG | 09/15/16 | 1.3203 | 0.00% |

| NZD/USD | 0.7272 | LONG NZD | STRONG | 08/02/16 | 0.7204 | 0.94% |

| AUD/USD | 0.7481 | LONG AUD | WEAK | 08/02/16 | 0.7576 | -1.25% |

| AUD/JPY | 76.58 | LONG AUD | WEAK | 09/05/16 | 78.90 | -2.94% |

| USD/MXN | 19.2815 | LONG USD | STRONG | 05/06/16 | 17.9418 | 7.47% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat