Dollar Index indecisive ahead of FOMC decision

Markets and economists forecast that the FOMC will leave the Fed funds target range unchanged at 5.25%-5.50% for a fourth consecutive meeting. Therefore, the policy meeting, scheduled for today at 7:00 pm GMT, will focus on the accompanying Rate Statement, Fed Chair Jerome Powell, and whether we see a pushback against March rate pricing.

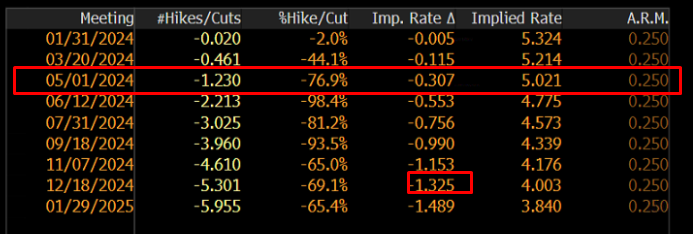

133bps of cuts priced in

December’s policy meeting delivered a dovish shift in its economic projections. The SEP revealed that FOMC market participants project three rate cuts this year, or 75bps, up from 50bps previously forecasted. There remains a disconnect between the Fed and the market. Futures and OIS are pricing around 133bps of cuts this year, with March at around a 40% chance of a cut. The first 25bp cut remains fully priced in for May’s policy meeting (31bps).

Bloomberg Futures Pricing

US CPI inflation data was widely talked about as we ventured into mid-month trading. Year-on-year headline inflation for December reached 3.4%, 0.3 percentage points higher than November’s 3.1% reading, while core inflation, or underlying inflation which strips out energy and food prices, cooled to 3.9% for the same period, down from 4.0% in November. More recently, though, the Core PCE Price Index, which is the Fed’s preferred measure of inflation, inched closer to 2.0% after reporting 2.9% on a year-over-year basis for the month of December; however, it is worth highlighting that quarterly Core PCE has actually been at 2.0% for two consecutive quarters.

So, with inflation clearly heading in the right direction, economic activity still resilient, and the labour market tight, there is still a chance that this FOMC meeting will offer little this evening, which could see a dovish reaction.

Despite this, with a no-change all but signed and sealed today, investors will still be closely scrutinising the Rate Statement and comments from Fed Chair Powell’s presser held thirty minutes later for any hint of policy easing (no new projections for this meeting). A possible tweak in language could be a change to the statement to highlight willingness to cut rates rather than policy firming. It is unlikely that they will remove the sentence: ‘In determining the extent of any additional policy firming that may be appropriate to return inflation to 2 percent over time’. But if they did, this would indicate a clear shift from hikes to cuts and likely underpin a bid in stocks and bonds and weigh on the buck.

March’s meeting continues to lean in favour of a hold, but in light of the resilient economic activity (Q4 2023 real GDP came in at an annualised rate of 3.3%, surprising markets) and inflation continuing to slow, it will be interesting to see if Powell says more on this. Nevertheless, we’re likely to see the chief largely stick to the script here: data-dependent and emphasise a somewhat neutral bias. If this is the case and this evening’s event offers little news, this Friday’s jobs data and CPI inflation number released mid-way through February will be crucial to watch as we head into March’s meeting.

Dollar Index indecisive ahead of FOMC decision

The Dollar Index has been monotonous in recent trading. Price has remained pretty much indecisive since 17 January after touching gloves with resistance on the daily chart at 103.62. Complemented by the 200-day simple moving average (SMA) at 103.53, this has proven a stubborn obstacle for bulls to dethrone. Ultimately, the above-noted resistances will be in focus, and a breakout beyond these levels could ignite interest in another layer of daily resistance from 104.15.

Support to have pencilled in ahead of the FOMC release falls in at 102.92, which happens to share space with the 50-day SMA at 102.82. Any breakout south of here throws light on lows around 102.09 and neighbouring daily support from 101.77.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,