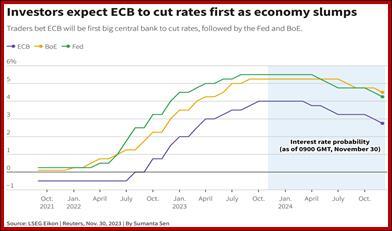

Greater probability of an ECB rate cut than in the US

Outlook: Today we get the official core PCE price index for October. See the Y-Charts chart for September. The text reminds us that the Sept number at 3.68% was down from 3.84% the month before and nearing the long-term average of 3.24%.

Forecasts for today’s numbers are as low as 3.0% for headline and 3.5% for core. Yesterday’s quarterly PCE at 2.3% gave the impression of better progress than today’s monthly will do.

We also get the Atlanta Fed’s Q4 GDPNow, last seen on Nov 22 at 2.1%. We guess it will go up at least a little more. In addition, there is the actual personal income and consumption, plus jobless claims.

Even if we get a really good drop in inflation in the US today, the eurozone beat us to it and unless we get a surprise, the top factor is greater probability of an ECB rate cut and maybe an earlier cut, too, than in the US. The betting is for March (ECB) or May/June (US).

Belong to the “yeah, but” list yesterday, today France reported a disappointing GDP in Q3—at minus 0.2% instead of plus 0.1%. The “yeah, but” it’s only Germany is not the case.

Another factor might be a frisson of fear that China is not recovering properly and this lack of robustness in unexpected and a little mysterious. We expect pundits to point to the youth unemployment rate at over 20%--again. This was a factor in the months after zero Covid was lifted and has not, apparently, changed, despite China declining to report it anymore. The IMF just revised its GDP to 5.4% this year from 5.0%, but honestly, nobody places any bets on IMF forecasts. On the whole, however, we can’t see risk aversion rising because of Chinese underperformance—yet.

Forecast: It’s too soon to say, but the dollar pushback may be growing legs. We have some mechanical factors—month-end, Dec futures rolling over, deeply oversold condition.

We also have some disinflation progress in which the eurozone is beating the US but going forward is more vulnerable to energy prices.

It remains to be seen whether the pushback turns into a full-bore rout. This depends to a certain extent on technical factors, such as a break below the 50% retracement line around 1.0858.

Fundamentals can count, too. The US is getting growth at 2% or more while both of the two big European economies, France and Germany, are skating on the thin ice of zero or a small negative. Besides, the US is food and energy self-sufficient, while Europe is always at the mercy of energy in particular. Herculean stock piling last year saved the day but we await fresh information about how it’s going to get through this coming winter.

Don’t count your chickens.

Tidbit: Charlie Munger died and is much mourned for his kindness, wisdom and snappy one-liners. Henry Kissinger also died and is little mourned, especially in the Kurdistan he betrayed.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat