Gold storms back as Chinese demand roars in — The Dragon’s bid is back

Gold’s bounce back to $3,300 isn’t just another dead-cat rally—it’s a statement, and once again, China’s in the driver’s seat. After flirting with the psychological floor just above $3,100 last week, gold has roared back to where it closed April. But this time, it’s not Western hedgers or ETF flows leading the charge—it’s a familiar heavyweight: Chinese onshore demand.

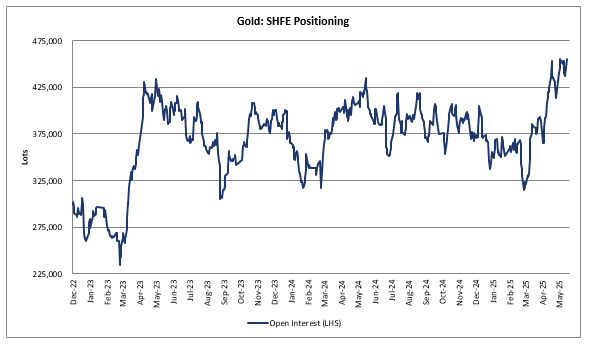

According to Goldman’s flow tracker, Shanghai’s night session has come alive, triggering a classic COMEX sympathy bid. Open interest on SHFE is back at all-time highs, with gold and silver both seeing a sharp jump—+3% and +4%, respectively. That kind of synchronized positioning doesn’t happen by accident.

More telling is the resilience of domestic Chinese traders. Despite the 8% drawdown from the recent peak, they held their fire, refusing to dump positions. That’s not momentum chasing—that’s conviction. And when the SGE/LBMA arb lit up, global buying interest reignited.

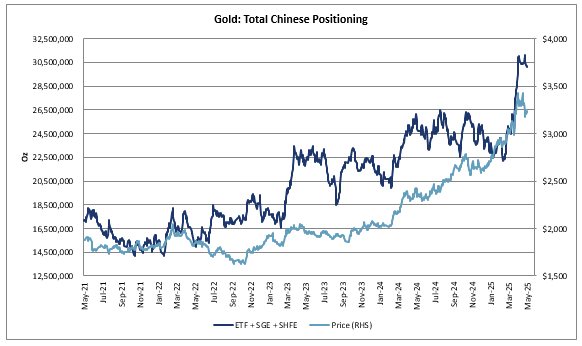

Chinese physical imports (ex-PBoC) also just clocked in at a 1-year high for April. That’s impressive given gold’s elevated nominal levels—it means the physical premium on the Shanghai Gold Exchange (SGE) isn’t just holding up, it’s punching through resistance.

And the market setup is clean. Ex-China hedge fund positioning is light, and CFTC data shows specs are flat, not leaning long. That makes the skew look dirt cheap—6-month 25-delta risk reversals are trading around 2.25v, with 6m implied vols near 19.5%. I think you want to own that optionality—vol should outperform if we break new highs, and the vanna tailwind is real.

Bottom line? This isn’t just a bounce. This is a reset. The physical bid from China, the clean slate in Western positioning, and the quietly persistent vol buyers all suggest one thing:

The gold bull isn’t dead—it was just consolidating. And the dragon just hit the buy button again.

Sovereign credit risk is fast becoming the fuel behind gold’s breakout bid—and for good reason. When trust in government paper starts fraying at the edges, the flight isn’t just to quality—it’s to autonomy. Gold’s core appeal in this climate? No counterparty risk. No IOUs. No need to worry whether Uncle Sam, Tokyo, or Rome can pay the coupon. It’s a pure asset, unleveraged and unimpeached by fiscal mismanagement.

As debt-to-GDP ratios stretch to absurd level in Japan and the U.S.—the cracks are showing. The market is beginning to reprice sovereigns not as “risk-free” but as structurally impaired assets. And when Moody’s fires a shot across the U.S. fiscal bow, traders know we’re in a different paradigm.

That’s why gold’s catching a strong bid—not just from central banks (who’ve been front-running this trend for two years), but from allocators rediscovering the age-old truth: in times of sovereign doubt, gold is the only thing that settles without a signature. You don’t need a credit default swap to hedge physical bullion. It doesn’t care about ratings downgrades, budget showdowns, or who chairs the Fed next.

The recent surge in Chinese demand only amplifies the signal: trust in fiat is eroding fastest where monetary policy has been tightest but credibility remains thinnest. Gold isn’t just a commodity anymore—it’s morphing back into the role it’s held for millennia: the final refuge in a system built on promises. And with those promises looking shakier by the day, the bid for no-counterparty, no-politics collateral is only getting louder.

The bond market is beginning to mutiny—and gold is the quiet beneficiary of that insurrection.

Wall Street’s starting to price in what gold bugs have known for years: sovereign bonds, especially U.S. Treasuries, aren’t sacrosanct—they’re debt instruments wrapped in a confidence game. And when that confidence cracks? Gold doesn't need a rating, a coupon, or a signature. It clears on trust alone. No counterparty risk. No “extend and pretend.” Just a rock-solid store of value in a world where even AAA ratings don’t mean what they used to.

Options skew is screaming downside in bonds. Long-dated puts aren’t just yield-curve hedges anymore—they’re IOU insurance. U.S. CDS just blew past Greece, for God’s sake. Traders are lobbing $11 million option premiums on Treasury downside like it’s Vegas, bracing for a fiscal blowout that could make 2023’s downgrade tantrum look quaint. This isn’t just a yield story anymore—it’s a credibility crisis, and the smoke is coming from the U.S. deficit fire that Trump’s tax-cut revival threatens to pour gasoline on.

As bond vigilantes grab the wheel and sovereign debt loses its luster, we’re seeing gold quietly reprice as the ultimate collateral—one that doesn’t default, dilute, or depend on political theater. If 10 year yields breach 5%, it won’t just be a bond market bloodbath—it’ll be the moment gold shrugs off its “safe haven” label and takes center stage as the only asset that doesn’t come with a promise someone else has to keep.

Gold doesn’t care about Fitch, Moody’s, or who chairs the Fed. That’s why it’s bid.

The bottom line is that the old “risk-free” benchmark looks anything but.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.