Gold jumps despite hawkish FOMC Minutes

The September FOMC minutes were rather hawkish, but gold prices rose yesterday. Did higher inflation finally push the yellow metal up?

Yesterday (October 13, 2021), the FOMC published minutes from its last meeting in September. For me, the publication is rather hawkish, as it signaled that the Fed could begin tapering its asset purchases as soon as mid- November or mid-December.

Participants noted that if a decision to begin tapering purchases occurred at the next meeting, the process of tapering could commence with the monthly purchase calendars beginning in either mid-November or mid-December.

This is because the FOMC members decided that the “substantial further progress” toward the Committee’s price- stability and maximum-employment goals has almost been met:

Many participants noted that although the economic recovery had slowed recently and the August increase in payrolls had fallen short of expectations, the labor market had continued to show improvement since the Committee’s previous meeting. A number of participants assessed that the standard of substantial further progress toward the goal of maximum employment had not yet been attained but that, if the economy proceeded roughly as they anticipated, it may soon be reached. On the basis of the cumulative performance of the labor market since December 2020, a number of other participants indicated that they believed that the test of “substantial further progress” toward maximum employment had been met.

The disappointing September nonfarm payrolls triggered some doubts about whether the Fed could announce tapering as soon as in November, but the recent comments from Atlanta Fed President Raphael Bostic and Fed Vice Chair Richard Clarida dispelled these doubts. The former official said: “I think that the progress has been made, and the sooner we get moving on that the better,” while the latter declared “I myself believe that the 'substantial further progress' standard has more than been met with regard to our price-stability mandate and has all but been met with regard to our employment mandate”. These remarks cement the expectations that the Fed’s tapering will start soon this year.

The Fed officials also discussed the pace of tapering, which they wouldn’t do if they weren’t convinced that the time was right to go ahead:

Participants also expressed their views on how slowing in the pace of purchases might proceed. In particular, participants commented on an illustrative path, developed by the staff and reflecting participants' discussions at the Committee's July meeting, that gave the speed and composition associated with a tapering of asset purchases (…) The path featured monthly reductions in the pace of asset purchases, by $10 billion in the case of Treasury securities and $5 billion in the case of agency mortgage-backed securities (MBS). Participants generally commented that the illustrative path provided a straightforward and appropriate template that policymakers might follow, and a couple of participants observed that giving advance notice to the general public of a plan along these lines may reduce the risk of an adverse market reaction to a moderation in asset purchases.

Given that the Fed continues to purchase Treasury securities by at least $80 billion per month and MBS by at least $40 billion per month, the signaled path of tapering implies that the quantitative easing is going to start in November 2021 and end in June 2022. Such a timeline pleases the Fed, as it will enable it to hike the federal funds rate if inflation turns out to be more persistent than initially thought:

No decision to proceed with a moderation of asset purchases was made at the meeting, but participants generally assessed that, provided that the economic recovery remained broadly on track, a gradual tapering process that concluded around the middle of next year would likely be appropriate.

Indeed, the FOMC members showed stronger worries about inflation, dropping references to the transitory character of inflation, and acknowledging that there were some upside risks:

Most participants saw inflation risks as weighted to the upside because of concerns that supply disruptions and labor shortages might last longer and might have larger or more persistent effects on prices and wages than they currently assumed.

Oh, really, inflation could last longer than you repeated for months?! You were wrong once again, what a surprise! What’s more, the committee also expressed concerns about the impact of easy monetary policy on elevated asset prices and financial stability:

In addition, some participants mentioned the risks associated with high asset valuations in the United States and abroad, and a number of participants commented on the importance of resolving the issues involving the federal government budget and debt ceiling in a timely manner (…)

Several participants expressed concern that the high degree of accommodation being provided by monetary policy, including through continued asset purchases, could increase risks to financial stability. Indeed, it’s high time for reducing the monetary stimulus, given the scale of irrational exuberance in the financial markets (investors are now so desperate to seek yields that they even buy non-existent sculptures)!

Implications for gold

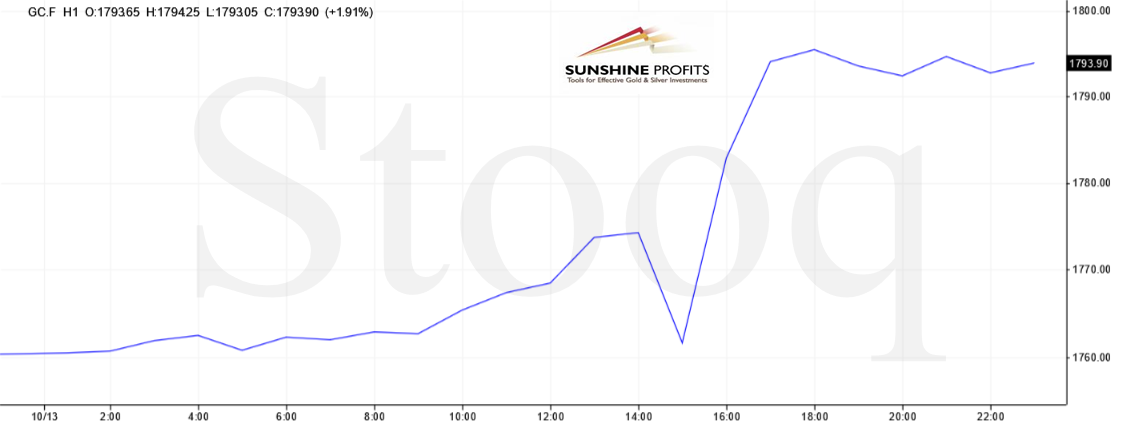

What do the recent FOMC minutes imply for the gold market? Well, the publication is rather hawkish, so it should be negative for gold prices. At least in theory. But the price of gold increased yesterday, approaching almost $1,800. What happened?

The detailed analysis of yesterday’s price movement displayed on the chart below shows that the FOMC minutes didn’t affect the gold market in any meaningful manner. This is probably because this year’s tapering has already been reflected in gold prices. The yellow metal reacted significantly, but to something different: the September CPI report.

Inflation rose slightly last month from 5.3% to 5.4% year-over-year, according to the BLS (so, no, inflation is not going away, just as I was warning investors for months). The price of gold declined initially, only to gain later. It seems that, at first, investors decided that higher inflation equals higher interest rates and a more hawkish Fed, so they decided to push gold down (just as they used to in response to higher inflationary readings earlier this year). However, after a while, traders changed their minds. So, although it’s too early to conclude this with certainty, it’s possible that the markets finally started to fear inflation, its persistence, and its impact on economic growth. If this is the case, we could see more safe-haven inflows into gold.

Nonetheless, investors shouldn’t expect too much from one trading day, even though yesterday’s gold reaction gives some hope that the yellow metal will ultimately behave as an inflation-hedge and benefit from elevated inflation. We will see – gold has to jump above $1,800 first.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Arkadiusz Sieroń

Sunshine Profits

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017.