Gold: How far can the bulls go?

-

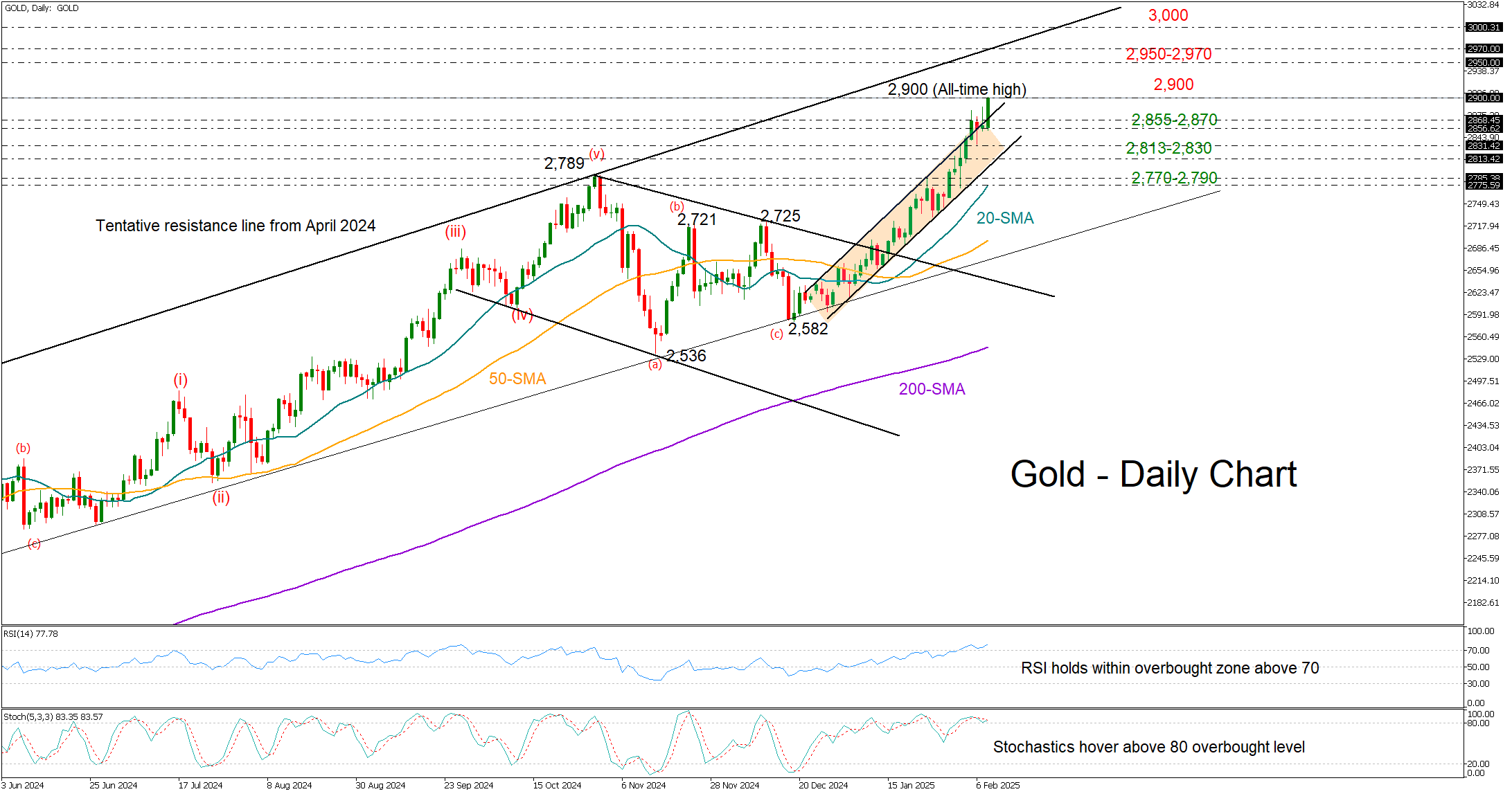

Gold extends record bull run, touches $2,900 psychological level.

-

Overbought signals are evident, but there is support at $2,850-$2,870.

Gold has been on a relentless bull run, posting only eleven days of minor losses since the ongoing upleg began in mid-December.

The price is currently testing the $2,900/ounce round level after opening the week with a bang, but the real challenge would be to maintain support above the channel’s upper band at $2,870 and the $2,850 base. If that proves to be the case and the bulls successfully claim the $2,900 ceiling too, the rally could continue towards the $2,950-$2,970 region where the 161.8% Fibonacci extension of the previous downfall and the resistance line, which joins the April and October 2024 highs, are sitting.

However, a warning note from the technical indicators should not be ignored. The RSI and stochastic indicators are both firmly in overbought territory, signaling that the road ahead could get choppy. Nevertheless, only a dive beneath $2,850-$2,870 could activate selling orders towards Thursday’s low near $2,830 or closer to the channel’s lower band currently seen near $2,813. Then, October’s peak of $2,790 and the 20-day simple moving average (SMA) near $2,770 could be the next destination. A break lower would neutralize the medium-term picture.

In summary, gold seems poised for another potential surge, but the key to a continuation higher lies in holding above $2,850-$2,870. If the bulls can maintain their grip here, a fresh wave towards higher levels could be on the cards.

Author

Christina joined the XM investment research department in May 2017. She holds a master degree in Economics and Business from the Erasmus University Rotterdam with a specialization in International economics.