Gold explains some, not all, of sharp widening in December trade deficit

Summary

A large $17.3 billion widening in the December trade deficit reflects a $5 billion drop in exports and a more than $12 billion jump in imports. The size of these moves overstate the impact on Q4 GDP growth and the extent of recent demand.

The trade of non-monetary gold accounted for more than half of December's widening. Since this is excluded from GDP it blunts the impact of net exports on GDP.

Prior to today's report we had anticipated a 0.7 percentage point boost from trade on Q4 real GDP growth. That lift is now poised to shrink. In fact, we might even see a slight drag on growth from trade due to stronger than anticipated imports.

All told goods imports finished the year down and were way down when excluding the lift from a sharp increase in high-tech related imports.

So are we now a country that simply imports less than it did before? We think the pullback in imports last year is overstated and is at least partly a result of wait-and-see around tariffs in 2025. Looking ahead there will inevitably be more rejiggering in supply chains, but we see scope for a modest ascent in imports in spite of tariffs in the year ahead.

Trade normalization continues: Imports up, exports down

If you were rooting for trade to boost economic growth in Q4, just about everything moved in the wrong direction in December. The U.S. economy increased its imports by more than $12 billion, with $10.2 billion off that increase coming from goods and the balance coming from increased service imports.

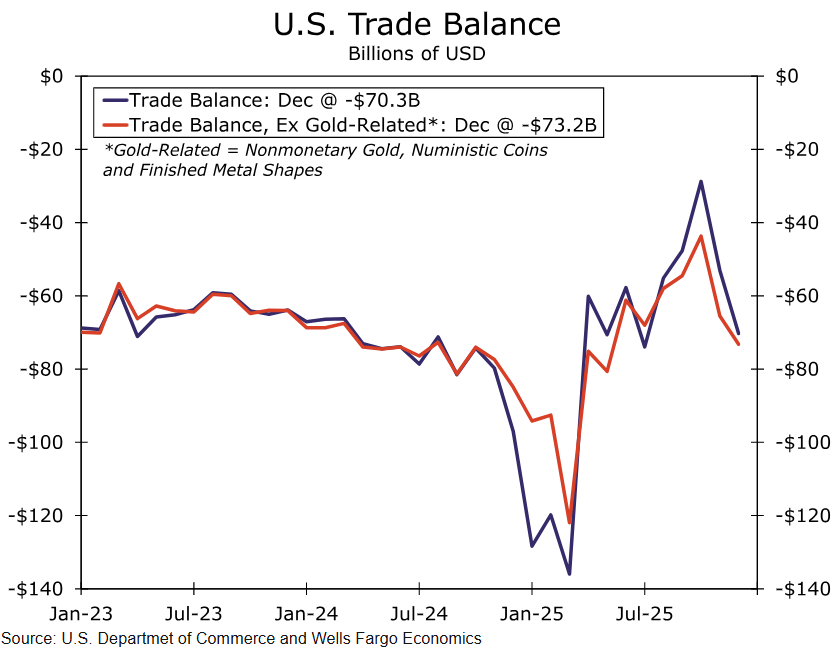

On the other side of the ledger, exports fell by $5.0 billion despite the one silver lining, a scant $0.5 billion increase in service exports being swamped by a $5.5 billion decrease in U.S. goods exports. The total trade balance widened sharply as a result reaching $70.3 billion, falling back to its widest level in six-months.

So while it is true that the U.S. economy is importing more and exporting less, it's much more complicated. The underlying details are less clear, including that almost half of the widening in the December trade deficit will not end up weighing on GDP growth. That's because the Commerce Department excludes non-monetary gold as it reflects asset reallocation under geopolitical stress, not real economic activity. As seen in the top chart, the international trade deficit when excluding these effects has been less volatile in recent months. Additionally, when you exclude high-tech related imports (computers, accessories, communications equipment, semiconductors) the gain in December imports is cut in half.

Author

Wells Fargo Research Team

Wells Fargo