Global macro transmission monitor – Week ending June 19, 2026

How macro shocks propagated through FX, commodities and rates last week.

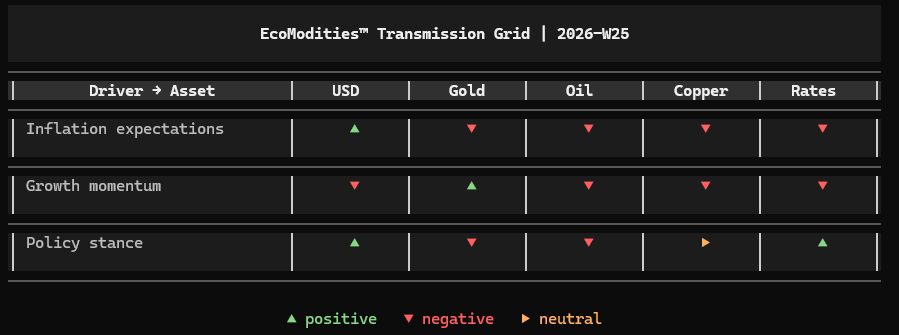

Executive transmission map

Policy transmission reasserted itself as the dominant macro driver last week as the Federal Reserve maintained rates unchanged while reinforcing a restrictive policy stance through its economic projections and forward guidance.

Inflation signals softened modestly outside the United States, with UK CPI undershooting expectations, but markets remained focused on policy differentials rather than disinflation. The result was renewed support for the USD and rates markets, limiting participation across gold and the broader commodity complex.

Growth data remained uneven. New Zealand GDP surprised positively, while UK labor indicators softened and global activity signals remained mixed. Cross-asset alignment strengthened around policy transmission, with the Fed once again becoming the primary anchor of market pricing.

1. Macro shock layer

A. Inflation shock

What moved

Inflation developments remained relatively contained, although UK inflation came in below expectations.

- UK CPI y/y: 2.8% vs 3.0% expected

- Previous: 2.8%

Why it matters

The softer inflation reading reinforced the broader disinflation narrative already visible across several developed economies. However, the market reaction remained limited as investors focused primarily on central-bank guidance rather than inflation surprises.

Transmission path

- USD retained support despite softer inflation data.

- Gold lost part of its inflation-hedge appeal.

- Oil and copper received limited support from disinflation.

- Rates markets remained driven by policy expectations.

FX transmission

Sterling weakened modestly as inflation undershot expectations, while broader FX markets remained focused on relative monetary-policy outlooks.

B. Growth shock

What moved

Growth signals remained mixed across major economies.

- New Zealand GDP q/q: 0.8% vs 0.8% expected.

- Previous: 0.5%.

- UK Claimant Count Change: 31.2K vs 25.8K expected.

- Previous: 8.3K.

Why it matters

The data reinforced the view that global growth remains uneven rather than collapsing. Regional divergences continue dominating growth transmission, preventing a uniform macro narrative from emerging.

Transmission path

- Gold attracted selective defensive flows.

- Oil remained sensitive to demand uncertainty.

- Copper struggled to build momentum.

- USD retained support through relative economic resilience.

FX transmission

Growth-sensitive currencies traded selectively as investors differentiated between regional economic conditions rather than broad risk sentiment.

C. Policy shock

What moved

Central banks dominated the week.

- Federal Funds Rate: 3.75% (unchanged).

- Bank of England Rate: 3.75% (unchanged).

- SNB Policy Rate: 0.00% (unchanged).

- BOJ Policy Rate: unchanged.

More importantly, the Federal Reserve's projections and communication reinforced a relatively restrictive policy stance despite ongoing progress on inflation.

Why it matters

Markets interpreted the FOMC meeting as a reminder that policy easing remains conditional on further evidence of sustainable disinflation. The policy layer therefore regained dominance over both inflation and growth transmission.

Transmission path

- USD strengthened through policy differentials.

- Gold faced pressure from higher-for-longer expectations.

- Oil and copper struggled against tighter financial conditions.

- Rates remained supported by restrictive policy expectations.

FX transmission

The dollar outperformed as the Federal Reserve maintained a more restrictive posture than many market participants had anticipated. Rate differentials once again became a primary driver of FX positioning.

2. Cross-asset transmission grid – 2026-W25

3. Market alignment check

Cross-asset alignment strengthened around policy transmission during the week.

While inflation data continued moving gradually toward disinflation, markets largely ignored inflation as a primary driver and instead focused on the Federal Reserve's commitment to maintaining restrictive conditions until inflation progress becomes more durable.

Gold, oil and copper all struggled to attract sustained participation, while USD and rates markets benefited from renewed policy support.

The macro chain currently shows policy transmission dominating both inflation and growth transmission.

4. Forward pressure points

USD

Pressure remains concentrated around policy differentials and the market's evolving expectations for future Fed easing.

Gold

Gold remains highly sensitive to real yields and higher-for-longer policy expectations.

Oil

Oil continues balancing physical-market fundamentals against tighter financial conditions and demand uncertainty.

Copper

Copper remains dependent on industrial-demand resilience and improving global growth visibility.

Rates

Rates markets remain vulnerable to further hawkish policy communication and delayed easing expectations.

One-line takeaway

The macro transmission chain rotated back toward policy dominance last week, with the Federal Reserve reinforcing restrictive conditions and supporting USD and rates while limiting participation across gold and commodity markets.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.