Global economic outlook: A resilient world economy faces US election test

The US and global economies remain resilient ahead of forthcoming US elections. However, Europe’s economic fragility poses challenges for its recovery despite support from the easing of interest rates.

As we enter the fourth quarter of 2024, the global economy continues to grow resiliently in the face of multiple challenges in recent years. The latest challenge is a risk re-appraisal of euro-area sovereign debt markets after the snap elections in France and a sharp global equity-market rout in early August on concerns about US recession and overly tight monetary policy.

However, contrary to widespread concerns, the US economy is not in nor on the brink of recession. Instead, it continues to expand at an above-potential annualised rate of around 3% QoQ according to latest data of the Federal Reserve Bank of Atlanta’s dependable GDPNow nowcast model. Scope Ratings (Scope) estimates US annual growth potential – or the trend rate of growth – at a more moderate 2%. While the unemployment rate has ticked up due to increased labour-force participation, it remains historically low, reflecting the resilience of the labour market.

Financial markets stabilised following the early-August downturn, with US equity indices reaching new bubbly highs. US Shiller P/E ratios remain meaningfully above levels from before the global financial crisis. There is increasing evidence supporting Scope’s long-standing thesis of a soft landing for the US and global economies, despite the sharpest rate hikes on modern record.

In many ways, elements of this cycle have been odd, such as the limited fashion that economies have responded to significant rises in rates alongside false recessionary prophecies from an inverted yield curve. Economic resilience has diverged from the financial crises book-ending significant rate-hike cycles of the past. This may suggest changes within the economy and adaptive alterations of the banking system since the 2008 global financial crisis and adoption of Basel III – even if some of the changes might have reduced the efficacy of the monetary transmission.

Nevertheless, as the US economy repeatedly proves market and economic consensus calls of recession wrong, it supports a level of inflation that is likely to stay above pre-cost-of-living-crisis run rates in the medium term. Core CPI inflation stood at 3.2% year-on-year in August despite having moderated materially from peaks. Scope is estimating average US CPI of 2.9% this year ahead of 2.5% in 2025.

Although inflation is more likely than not to continue declining over time, medium-run risks for the symmetrical 2% inflation goal may be skewed more to the upside today than the balance of risks pre-cost-of-living crisis. This could pose a challenge for the Federal Reserve as it targets cuts of a significant 250bp in aggregate by 2026. Aggregate effects of monetary easing, an expansionary fiscal policy and an already over-heating US economy may complicate the path of significant monetary easing, especially recognising persistent inflation in the services sector and wage growth.

US elections to be decisive for the economic outlook

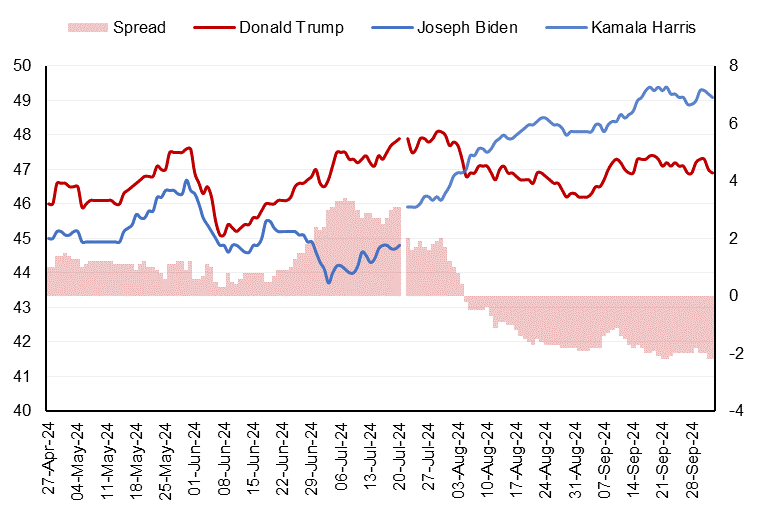

US elections in November will be decisive for the global economic outlook for 2025 and beyond. President Joe Biden dropping out of the race changed the nature of the contest and at this stage the election outcome looks like it will be a very close race between Vice-President Kamala Harris and former President Donald Trump (Figure 1). The party securing the presidency is likely to be in the stronger position to carry the lower house (House of Representatives), whereas the Republican Party may have the edge in the upper house (Senate) given more Democrat seats up for grabs this year.

Figure 1. 2024 US presidential-election opinion polling

Share of national voting intentions, %.

N.B.: Donald Trump (red) versus Kamala Harris (blue) opinion polling; Trump versus Joe Biden before 21 July 2024. Source: RealClearPolitics Polling.

Either a Harris or a Trump presidency will be reflationary despite their varying economic objectives, tax policies, and spending priorities. Nevertheless, Trump pledges of higher tariffs across the board to 10%-20% alongside at minimum 60% on imports from China suggest near-term implications for price rises might be more significant under Trump.

A Harris victory this November would likely offer a greater degree of continuity of existing economic trends, maintaining the current balance of risks, facilitating a continuation of gradual rate reductions. Conversely, a Trump win may upend existing expectations and force a re-assessment of economic and inflation outlooks and the timing and speed of central-bank easing.

Under such a scenario, tariffs and tighter immigration policy may eventually slow output growth even as inflation is temporarily buoyed. Moreover, Trump challenging the independence of the Federal Reserve – advocating for a greater role for the president within central-bank policy – could exacerbate uncertainty around inflation and interest-rate trajectories if he re-enters office.

In the medium run, any Trump presidency may introduce heightened economic risks globally, elevating financial risk from deregulation and geopolitical uncertainties although nearer-term implications may be more mixed due to pro-business policies.

Central banks unlikely to return to an earlier era of ultra-low rates

The Federal Reserve’s jumbo rate cut on 18 September in response to market pressures changes the mathematics of other central banks, regardless of whether they acknowledge this publicly. Even so, as central banks further trim rates, they are unlikely to return to the ultra-low figures of during and before the pandemic crisis. Higher rates for longer – or higher so-called neutral rates than before the cost-of-living-crisis after the conclusion of rate-cut cycles – recognises that easing is coming against above-potential global growth of 3.3% this year and 3.4% for next year. Scope’s global growth figures are in fact 0.2pp stronger and not weaker for each year than its outlook as of the end of last year.

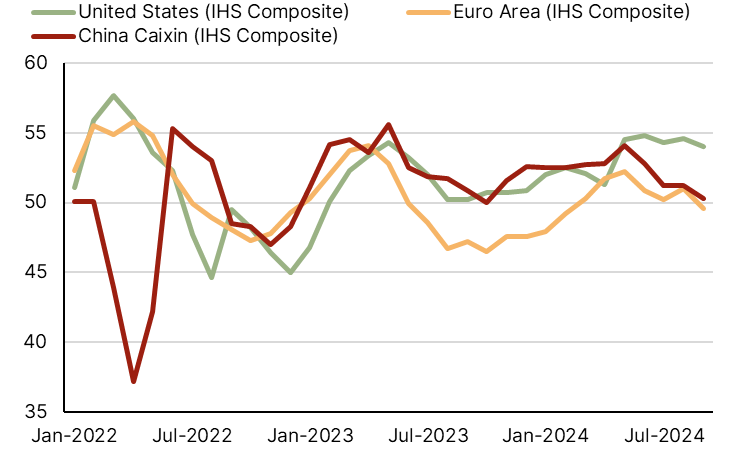

Nevertheless, central-bank intervention remains crucial especially for regions such as the euro area, which has seen a material weakening of its economic outlook. The bloc’s composite purchasing managers’ index dropped below 50 in September (Figure 2) – falling under an expansion-contraction line for the first month since February of this year as a temporary boost from Paris Olympics faded.

The euro-area recovery has been dragged down by the manufacturing sector and a sluggish German economy. A governance crisis in France has sapped confidence in its economy, although French spread movements have recently remained rather idiosyncratic, presenting lesser contagion risk for peer European markets compared with early phases of the crisis. Meanwhile, euro-area periphery economies continue outperforming amid an uneven European recovery.

Figure 2. Composite purchasing managers’ surveys, global

Seasonally-adjusted indices.

N.B.: >50 is expansion; <50 is contraction. Source: S&P Global/IHS Markit, Scope Ratings.

This underscores an urgency for the European Central Bank to consider easing rates again this quarter. Nevertheless, continued high borrowing rates, even as short-end rates are gradually trimmed, may support balance sheets of European financial institutions although higher steady-state rates alongside the fragile economy present challenges for most European credit sectors.

Author

Dennis Shen

Scope Ratings

Dennis Shen is Chair of the Macroeconomic Council and Lead Global Economist of Scope Ratings, the European rating agency, based in Berlin, Germany.