GBPUSD Forecast H2 2016: Here are the reasons why cable might continue to sink

So far this year the British Pound has weakened over 10% against the US Dollar and tested its worst levels in more than three decades. Majority of the year-to-date losses were recorded on the day when British voters decided that UK should end its 43 year old association with the European Union (EU). The surprise outcome led to an unprecedented fall in sterling, taking the GBP/USD pair to the lowest level since 1985.

Uncertainty to Rule

Despite of the historic referendum, so-called Brexit, UK will continue to be a part of EU as the actual process would take a minimum of two years, or more, once Article 50 is invoked. For the UK to initiate the process of leaving the economic bloc, it has to give an official notice under an agreement called Article 50 of the Lisbon Treaty, which governs the withdrawal process and stipulates two year to negotiate / agree on terms of withdrawal.

The official notice was not given immediately after the referendum as the proposal has to be ratified by Parliament. Moreover, the current Prime Minister, Theresa May, has indicated that the process will not kick-off before the end of 2016. It, however, remains unclear if Britain will invoke Article 50, hold a second referendum, or work to renegotiate the terms of its membership, which eventually fuels several years of tremendous uncertainty over UK’s changed relationship with the EU.

UK Economy Headed Towards a Recession?

Until the uncertainty is cleared up, the decision to leave EU is expected to cause a major negative shock and might have far-reaching consequences for the UK economy in years to come. Although the longer-term implication on the UK economy is far from clear, the early Brexit fallout sentiment indicators are showing signs of a sharp economic slowdown. A special post-referendum survey clearly revealed that business activity and confidence took a sharp knock in July.

According to first preliminary release of Markit’s UK PMI figures for the month of July, manufacturing index dropped to its lowest level since February 2013 and the services index showed its biggest drop on record. The composite (services and manufacturing) index fell from 52.4 in June to an 87-month low of 47.7, signaling a sharp contraction in activity and fueled fears of an imminent recession.

Chris Williamson, the chief economist at Markit, said: “July saw a dramatic deterioration in the economy, with business activity slumping at the fastest rate since the height of the global financial crisis in early 2009."

On the contrary, the Bank of England's latest regional agent report, its first monthly assessment of the impact on business conditions after the referendum, suggested that the UK economy may have, so far, withstood the shock of the Brexit vote. Although, the report showed a noticeable rise in uncertainty but there was no clear evidence of a substantial drop in the overall confidence level. The report also indicated little impact on consumer spending, with some cautiousness over big-ticket items.

However, the preliminary estimate of Q3 GDP, covering July-September period, will be released in October. That’s when we will come to know if the Brexit vote is really dragging the economy back into recessionary phase.

What Happens to Inflation and Labor Market?

With over a month since Britain's vote to leave EU, what we still don’t know quite well is the impact of falling Pound on inflation and trend in labor market. The recent sharp slide in the British Pound would make imports more expensive and hit prices, but some experts believe that the effect might not kick-in immediately.

On the other hand, despite of a looming recession, a plunge in sterling has given exporters a boost, which many economists believe should keep UK labor market vibrant. According to the Office for National Statistics, UK unemployment rate fell to 4.9% for the three months to May, the lowest since July 2005. The figures, meanwhile, cover the period before the Brexit vote and hence, some analyst warned that the positive trend is unlikely to continue for much longer. Meanwhile, the first release of employment data, comparing July, August and September 2016 data with the months prior to the vote, will be released in November and will show the real picture of the labor market condition in post-referendum regime.

BOE Set to Dominate

The central bank still has no official data to assess the extent of economic implication of the Brexit and hence, there would be less urgency shown by the BOE to further ease its monetary policy immediately. However, the bank might still take some interim measures to help support the economy and announce a rate-cut for the first time in over 7-years.

The BOE monetary policy stance would now be one of the most important factors that would drive cable in the near-term. Once the incoming data flow confirms actual economic fall-out, BOE will opt to aggressively ease its monetary policy and could also decide on expanding its quantitative easing (QE) program during the later part of 2016.

Domino Effect

Another factor that might trigger a fresh bout of volatility in the British pound is the likelihood of a second referendum on Scottish independence to leave the UK. Almost two-third of Scots voted for UK to remain with the EU, which prompted Scotland's First Minister Nicola Sturgeon to put forward the option to hold another referendum on independence.

Finally, Brexit-led fears of a dramatic reduction in foreign investment flows, although some of it might get negated by rise in UK exports, has now drawn spotlight on Britain's bulging current-account deficit. In the first quarter of 2016, UK's current account deficit was £32.6 billion, accounting to around 6.9% of GDP at current prices, slightly lower than a record high of 7.2% in the last quarter of 2015. In recent year, UK had been relying on large inflows of foreign capital to offset massive current account deficit. Thus, failure to resist a widening current account deficit would now push rating agencies to downgrade UK’s AA credit rating.

Increasing Odds of a Fed Rate Hike

Some of the decline in the GBP/USD pair might also come on the back of strength in the US Dollar, which remains underpinned by a moderate growth trajectory of the US economy and increasing prospects of an eventual Fed rate-hike. Despite of a weaker-than-expected advanced GDP number for the second-quarter of 2016, the US economy has been showing signs of strength of late. The upcoming US Presidential election on November 8th might add to the level of economic uncertainty but with strong labor market performance, which has been an important pillar of strength for the US economy, rising wages would now trigger a faster pace of inflation and revive hope of a Fed rate-hike decision later during this year. At its meeting in July, FOMC left interest-rates unchanged but has set the stage for a potential rate-hike in September. Moreover, the Federal Reserve has already hinted towards possibilities of an imminent interest rate-hike before the end of this year.

Numerous uncertainties concentrating in such a short-period of time might exert more selling pressure on the British Pound. Consequently, we believe that the GBP/USD pair remains vulnerable until end-2016 and should witness a substantial drop even from current levels.

GBP/USD Technical Set-up

Although in the near-future, the pair might witness some rebound from oversold conditions. However, the pair has decisively broken below 1.3500 swing lows support, held in the aftermath of 2008’s global financial crisis.

Moreover, the pair has also failed to hold a longer-term descending trend-line support, extending from last quarter of 2011 through lows touched in March 2013 and early 2016.

Hence, any near-term recovery might now be capped at this important support, now turned strong resistance, near 1.3500 psychological mark.

Looking at the long-term bearish set-up, the pair’s up-move to July 2014 high marks 50% retracement of December 2007-March 2009 sharp slide. Thus, a break below previous swing lows support has now opened room for test of 61.8% Fibonacci expansion level support near 1.2450.

Post-BOE update*

The 23.6% Fibonacci retracement level of Brexit-led sharp slide once again proved to be a strong resistance, with the pair plummeting over 200-pips from the session-high after BOE announcement. The central bank slashed its benchmark interest rates by 25 bps to a new record low of 0.25% and was broadly in-line with market expectations.

Markets, however, were surprised with the central bank's decision to expand its program of purchasing UK government bonds by an additional £60 billion, taking the total stock of these asset purchases to £435 billion. Moreover, a sharp downgrade of the UK economic growth in 2017 added on to the intense selling pressure surrounding the British Pound.

For the time being, the pair might have found a temporary support near 1.3100-handle but any recovery attempts might now be capped at 100-SMA (4-hourly) near 1.3200-region.

Meanwhile, on the downside, bears might still be targeting for a retest of the very important horizontal support near 1.3060-50 region. A follow-through selling pressure below this strong support would now turn the pair vulnerable to extend its downslide and break through 1.3000 psychological mark towards testing its next major support near 1.2930-25 region.

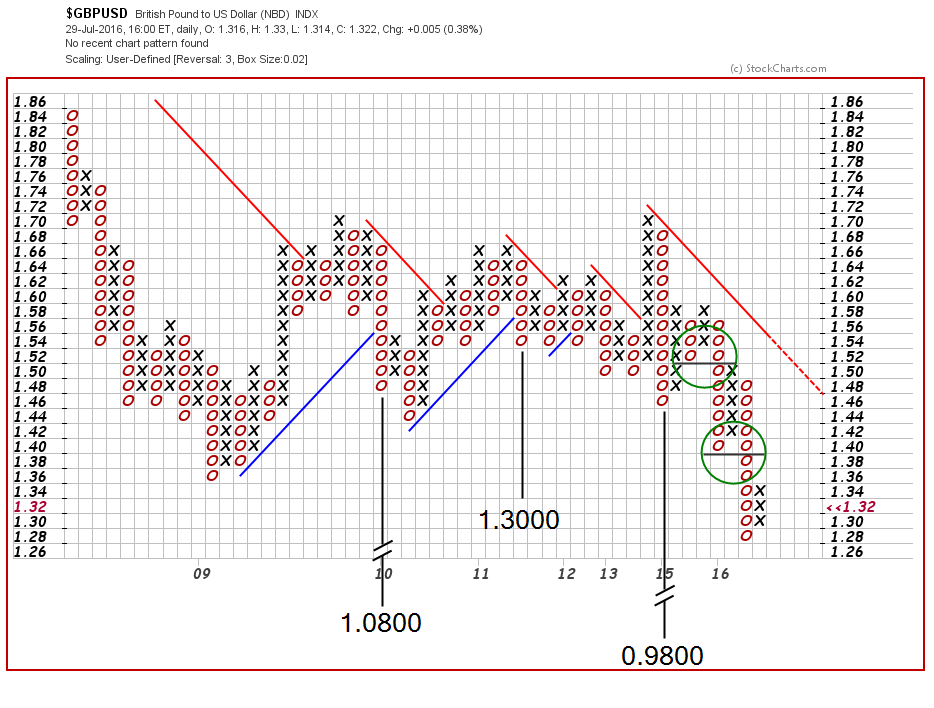

GBPUSD Point & Figure Chart, by Gonçalo Moreira

Already at the end of 2015, a 3-box reversal approach to GBP/USD hinted at a chart which was about to leave behind its consolidative tone. The upper green circle was the technical breakdown signal (a point and figure double-bottom, not to confound with the double bottom reversal pattern in bar charts) we took as an omen for the forthcoming weakness.

The lack of definition as for trend direction during the years 2009 2015- at least at this 3-box granularity, was not an impediment for point and figure charts to establish several potential price targets. Herewith pictured are some of them, of vertical nature, based on those columns that were considered structural changers at different moments in recent history. 1.30 can be considered a filled count, while the other two ascertained projections, 1.08 and 0.98 predict a continued bearish roadmap before we reach a reversal point.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.