GBP/USD Weekly Forecast: Sterling capped by looming Federal Reserve policy change

- Sterling stalls near the middle of its six-month range.

- UK economic data improves, promising an advance in the third quarter.

- Covid cases climb but future direction and impact are uncertain.

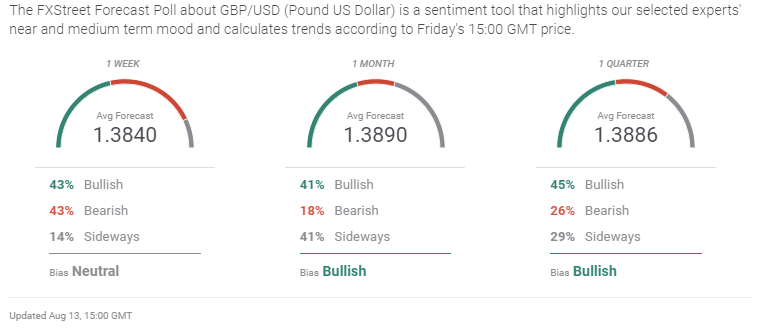

- FXStreet Forecast Poll is bullish but the gains are minor.

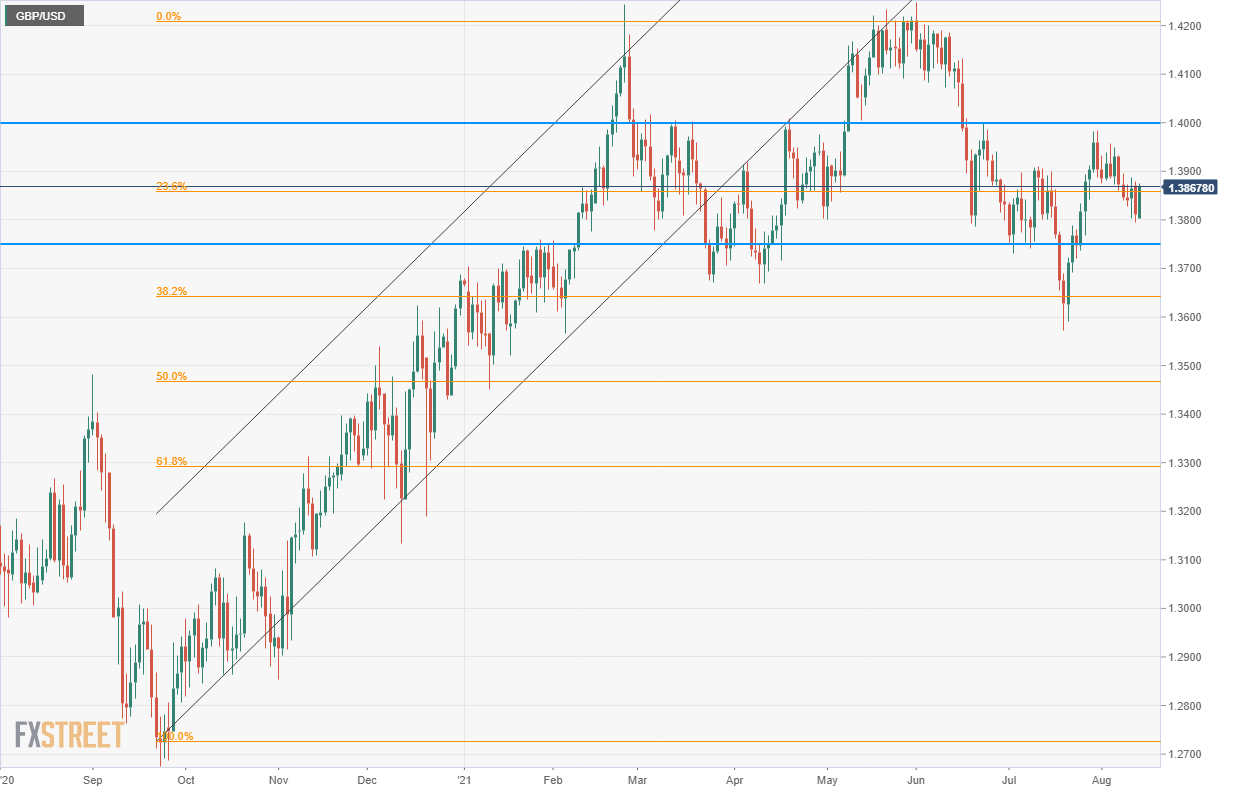

Sterling declined on the week but the close at 1.3861, just points from the open, gave no indication that the pound was any closer to departing from the ranges of the past six weeks, or in a wider definition, the past six months.

Since the second week of June the GBP/USD has traded between 1.3750 and 1.4000, with a brief four-day excursion to 1.3600. Counting from the middle of February the range is wider on the topside, 1.4200, but a nearly identical 1.3700 on bottom. Except for the five weeks above 1.4100 from May 10 to June 15, the majority of the action was between 1.3800 and 1.4000.

This prolonged period of relative stasis stems from the uncertainty over the pandemic, which has now returned three times, and its delay of the UK’s economic recovery.

Whatever progress the UK has made to restore its economy, the accomplishments are still hostage until the pandemic is reduced from being a fulcrum of public policy, if not from the health considerations of the population.

Bank of England (BOE) monetary policy is cautious and unlikely to change until it is clear that the pandemic is no longer a threat to the economy. It is conceivable that this caution could last through the winter flu season. Consumer prices are rising but the gains are nowhere near as dangerous as in the United States.

The galloping inflation in the US, and its profound political consequences, may force the hand of the Federal Reserve as early as its September 21-22 meeting. That, and its possible precursor at the Jackson Hole symposium on August 26-28, is the chief threat to the rise of the pound against the dollar.

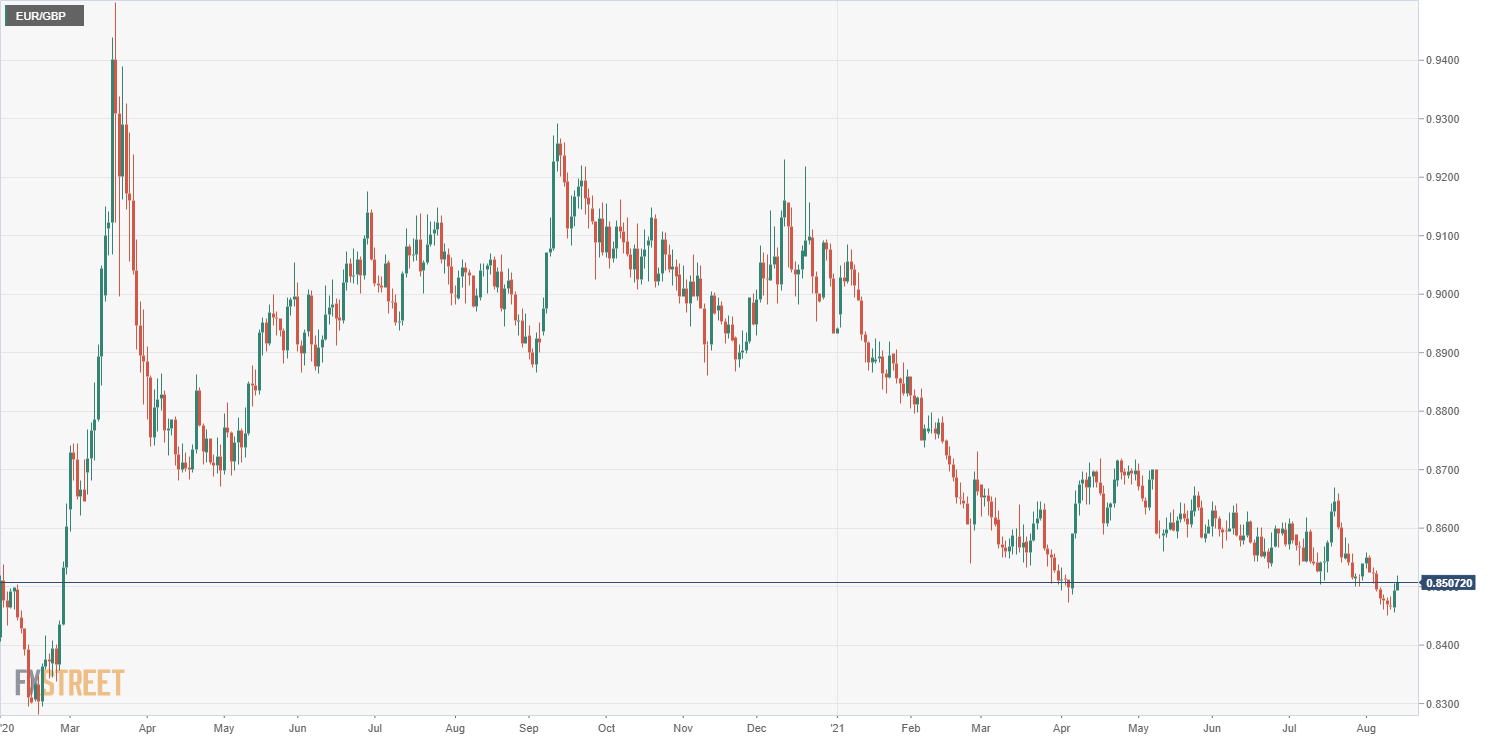

For the EUR/GBP there is almost no chance that the united currency will regain the initiative in the next two quarters. The year-long descent of the cross should continue.

Vaccination rates on the continent are well behind those of the UK and the recovery in the EU, lags that of Great Britain by a substantial amount. European Central Bank (ECB) monetary policy is paralyzed and will remain so.

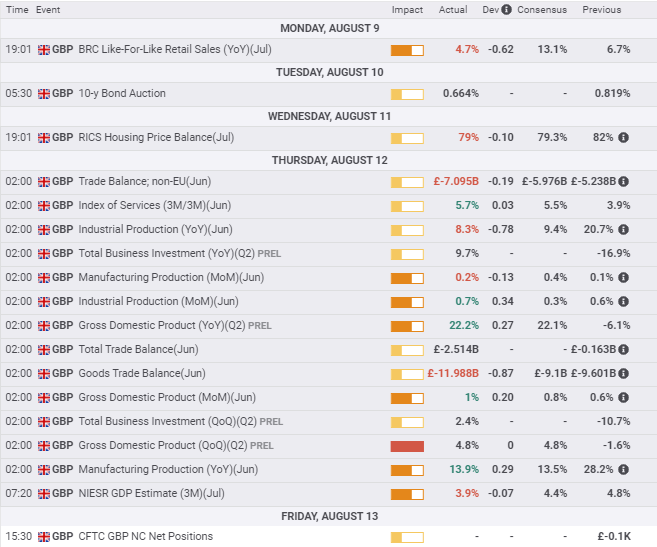

Economic data this week was good for the UK and the pound. Gross Domestic Product (GDP) was better than expected in June and for the second quarter. Industrial Production more than doubled forecast in June and Manufacturing Production completed its third exceptional month in a row.

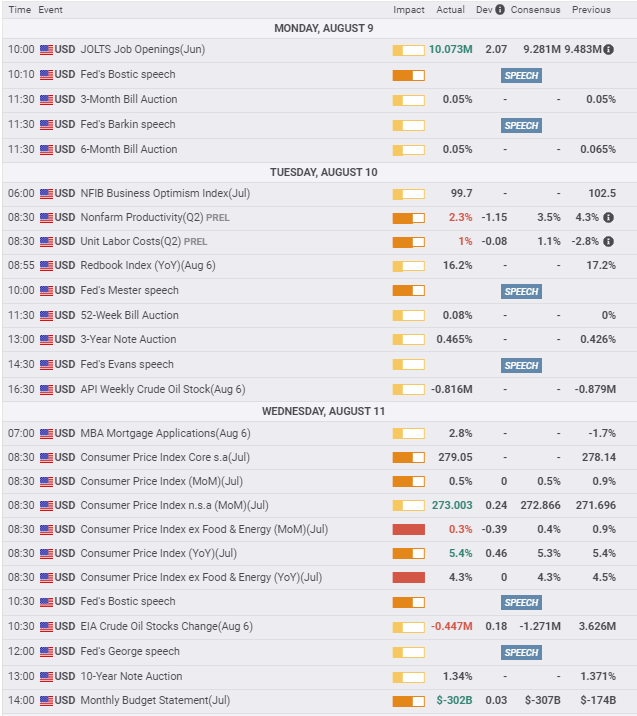

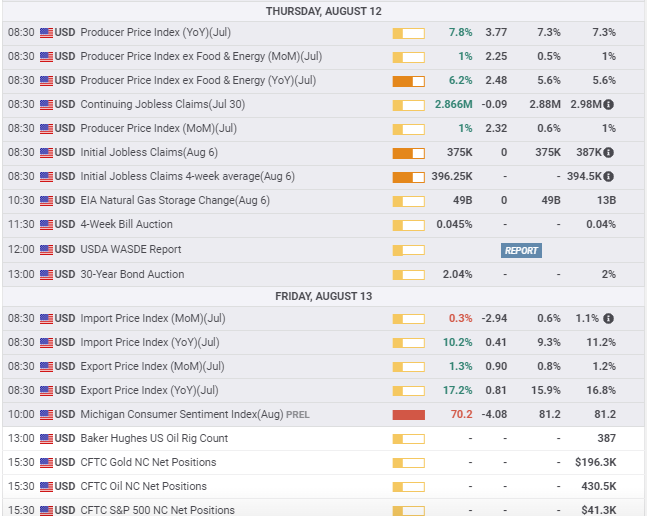

In the US, July's annual Core CPI at 4.3%, a bit less than the 4.5% forecast, and the unchanged headline rate at 5.4%, supported the Fed’s contention that the inflation increases will be transitory. However, PPI for July was the opposite with the headline rate of 7.8%, and the core gauge at 6.2%, setting records and far above their forecasts.

American companies are far more willing to pass on cost increases to customers this year than at any time in a generation, and these gains are sure to show up in CPI in the next few months.

Markets are unsure if the spreading Covid-19 Delta strain will bring on a new series of economic closures and a flight to the safety of the US dollar.

Israel is said to be considering reimposing some restrictions as its cases rise despite its early and high vaccination rate. A key will be the hospitalization and mortality rates, which are below the earlier waves but rising.

Federal Reserve policy is also undetermined. Several bank officials, including Vice-Chair Richard Clarida, have suggested that a reduction in the amount of bond purchases may be nearing. The Fed’s contention that the recent inflation spike is temporary will be discussed at the August 26-28 annual Jackson Hole symposium, but whether the conclave will produce a consensus for the FOMC meeting a month later is highly speculative.

Nonetheless, the potential for policy developments will restrain movement during the August vacation season in Europe and the United States.

Treasury rates in the US were lower. The 10-year yield lost its weekly gain after the August Michigan Consumer Sentiment Index plunged below its prior pandemic low and closed at 1.283% down 8 basis points on Friday.

GBP/USD outlook

In normal times the sterling and the dollar would be in an economic and policy competition. With both economies performing well and interest rates near historic lows, the betting would be on which central bank would be the first to hike. Accelerating GDP and inflation would be the determining factors.

For the BOE and the Fed, the status of the pandemic is the overriding concern. If infection rates continue to climb, neither bank will change their accommodative policies.

However, if the pandemic subsides, US inflation rates make the Fed the odds-on favorite for the first reduction in its bond support program. That possibility is an implicit cap on the GBP/USD and should override any differential benefit from the UK’s economic progress.

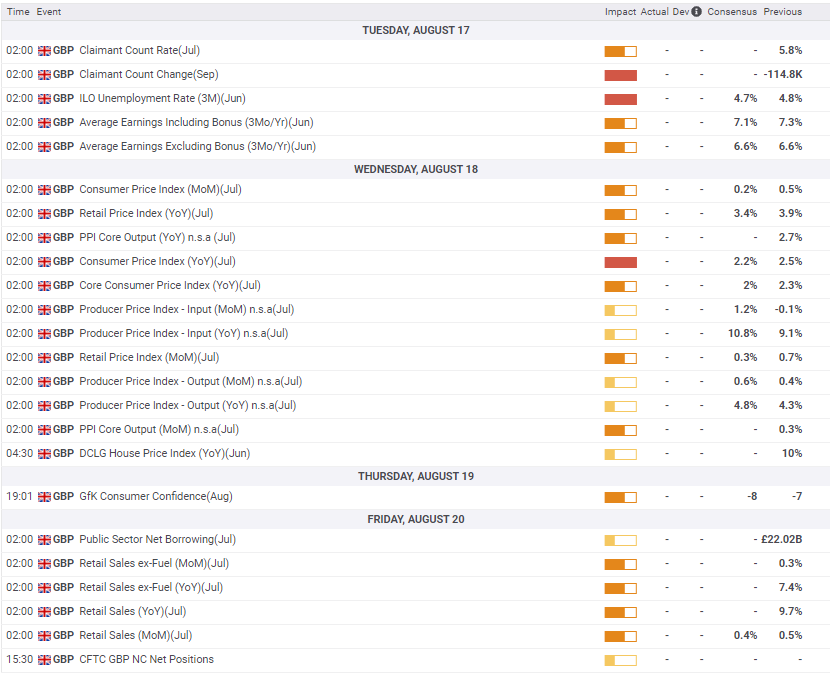

The UK has a busy week on tap with unemployment for June and inflation and Retail Sales figures for July.

Producer price increases, which have been even higher than in the US, have yet to show much impact on consumer inflation. If that changes it could provide modest support for the sterling.

On the US side, Fed policy is in abeyance until at least the Jackson Hole meeting on August 26-28, or the September 21-22 FOMC.

American data centers on Retail Sales for July on Tuesday, which are forecast to show a cooling from June’s unexpectedly strong results. A good number will provide dollar support. Industrial Production for July 45 minutes later is forecast to be unchanged from June.

Trading bias for the week ahead is mildly lower. Retail Sales data from each country and price statistics from the UK will not change the economic picture and the focus on the Fed policy is a benefit for the dollar.

The lack of a good reason to buy the pound argues for a continuation of the measured decline. The final two weeks of the August vacation are unlikely to produce a surprise.

UK statistics August 9–August 13

US statistics August 9–August 13

FXStreet

UK statistics August 16–August 20

FXStreet

US statistics August 16–August 20

GBP/USD technical outlook

With the GBP/USD near the mid-point of its four-week range the Moving Average Convergence Divergence (MACD) is neutral as is the Relative Strength Index (RSI). True Range has turned lower as the week's efforts produced a slight decline. None of these indicators suggest major motion in the week ahead.

The 21-day moving average (MA) and the 200-day MA are support. The shorter term at 1.3832 was passed on Friday's ascent and is first in line. The 50-day MA at 1.3889 is part of the resistance band from there to 1.3900 which is also backstopped at 1.3927 by the 100-day MA.

Support and resistance lines are the products of a long period with the market traversing the same ranges. In that environment the moving averages play a heightened role.

Bias in the GBP/USD is slightly lower given the series of lower highs over the past month, but it is far less than a negative trend and would be reversed by any positive fundamental development.

Resistance: 1.3889 (50 MA), 1.3900, 1.3927 (100 MA) 1.3935, 1.4000. 1.4100

Support: 1.3832 (21 MA), 1.3800, 1.3750, 1.3690, 1.3630

FXStreet Forecast Poll

The bullish outlook of the FXStreet Forecast Poll is in name only. The range is less than 50 points.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.