GBP/USD Weekly Forecast: Pound Sterling looks for further upside in UK CPI, Fed-BoE decision week

- The Pound Sterling staged a late rebound against the US Dollar, with 1.3000 tested.

- GBP/USD awaits a fresh directional impetus from the UK CPI data and Fed, BoE decisions.

- Pound Sterling buyers fight back control above 21-day SMA, as the daily RSI flips bullish.

The Pound Sterling (GBP) stalled its correction from over two-year highs against the US Dollar (USD) and staged an impressive comeback, with the GBP/USD pair having tested the critical 1.3000 threshold.

Pound Sterling – A tale of two halves

GBP/USD witnessed good two-way price action, correcting sharply to a three-week low of 1.3002 in the first half of the week only to recover the weekly losses in the latter part. The sentiment around the pair was mainly driven by the dynamics of the US Dollar. The Greenback continued to remain at the mercy of the market’s expectations on the size of the interest rate cut by the US Federal Reserve (Fed) in the upcoming week.

The August US labor market data fuelled a late recovery in the USD against its major rivals last week, which extended well into this week and weighed heavily on the GBP/USD pair. US Nonfarm Payrolls rose by 142,000, missing a 160,000 gain estimated. On the other hand, the Unemployment Rate edged down to 4.2%, in line with expectations.

Discouraging US employment data rekindled worries about a possible economic downturn and lifted the haven demand for the Greenback. Markets continued to run for cover in the buck, bracing for the critical US inflation data on Wednesday. Data published by the US Bureau of Labour Statics (BLS) showed Wednesday that the CPI rose 0.2% MoM in August, aligning with the expected 0.2% print. US August core CPI jumped 0.3% MoM vs. estimates of 0.2%. Sticky underlying inflation figures prompted markets to rule out an outsized Fed rate cut this month.

The Pound Sterling also felt the heat from softer UK pay growth and Gross Domestic Product (GDP) data released on Tuesday and Wednesday respectively. Average Earnings excluding Bonus in the UK rose 5.1% 3M YoY in July versus a 5.4% growth seen in June. The UK economy showed no growth over the month in July after stalling in June, data from the Office for National Statistics (ONS) showed Wednesday, missing the expected 0.2% growth.

These fundamental factors dragged GBP/USD to the lowest level in three weeks to just above the 1.3000 level. Buyers, however, managed to defend that key level, as the US Dollar saw a fresh selling wave on dismal US Producers Price Index (PPI) and Jobless Claims data, which reinforced bets of a 50 basis points (bps) rate reduction by the Fed at its September 18 policy announcement.

Annually, the headline PPI rose 1.7% in August, compared to the market consensus of a 1.8% print. The core PPI increased by 2.4% YoY in the same period, below the estimate of 2.5%. Meanwhile, the Initial Jobless Claims came in at 230,000 for the week ended Sept. 7, up 2,000 from the previous period while aligning with the forecast. Dismal US data combined with the Wall Street Journal (WSJ) article on the Fed's rate cut dilemma brought back bets for a jumbo cut at the September meeting, smashing the Greenback while propping up GBP/USD back above 1.3100.

Markets are now pricing in a 43% chance of the Fed cutting rates by 50 bps, up from 27% a day earlier, with a 57% probability of a 25 bps cut, the CME Group’s FedWatch tool showed. Increased dovish Fed expectations exacerbated the US Dollar’s pain on Friday. The last data release from the US showed ahead of the weekend that the consumer confidence improved slightly in early September, with the preliminary University of Michigan's Consumer Sentiment Index edging higher to 69 from 67.9 in August. This reading came in above the market expectation of 68 but failed to help the USD stage a rebound.

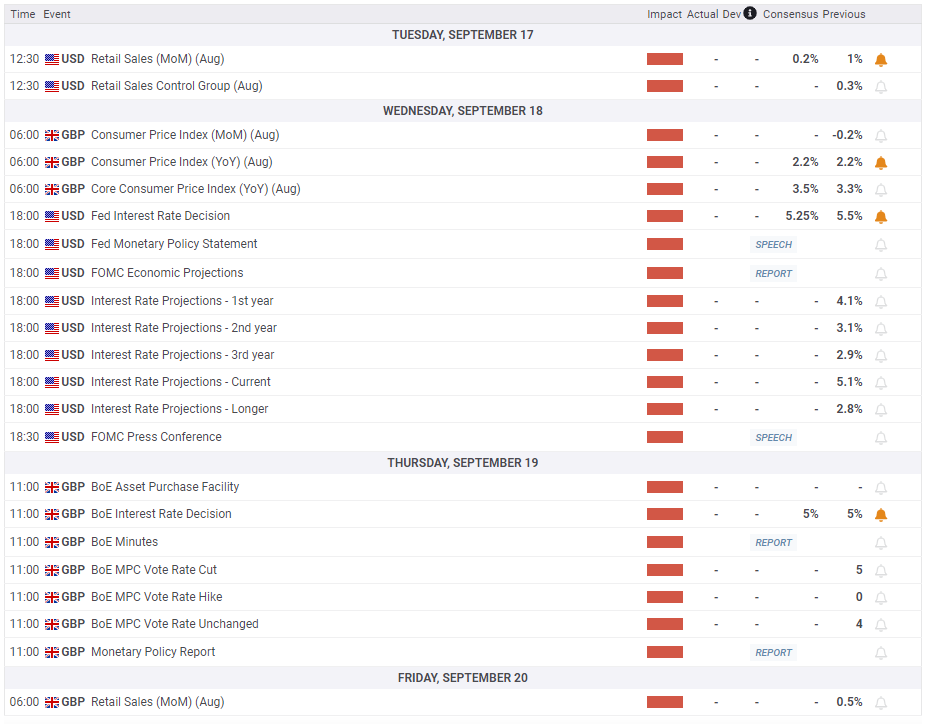

Week ahead: All eyes on UK CPI data, Fed and BoE verdicts

All eyes now turn to the high-impact UK CPI inflation report and the all-important Fed and BoE policy announcements, which will determine the next directional move in the GBP/USD pair.

It’s a quiet start to the big central banks’ week, with no relevant data to be released on Monday. Tuesday will feature the US Retail Sales data while the UK docket remains data-dry.

Wednesday is a busy one, with the UK inflation data slated for release before the key Fed verdict and Chairman Jerome Powell’s press conference.

It’s not a ‘Super Thursday’, as the BoE will only announce its rate decision without the update projections and Governor Andrew Bailey’s presser to follow. That same day, the US calendar will see the publication of the weekly Jobless Claims, Existing Home Sales and Philly Fed Manufacturing data.

On Friday, the UK will release the Retail Sales data, as traders will look to a speech from BoE policymaker Cathrine Mann.

Fed policymakers will also return to the rostrum on Friday, as the Fed’s ‘blackout period’ comes to an end.

GBP/USD: Technical Outlook

As observed on the daily chart, the GBP/USD pair defied bearish pressures and managed to find its footing above the key support at 1.3045 (July 17 high), having tested bids briefly at 1.3000.

On the road to recovery, the pair recaptured the 21-day Simple Moving Average (SMA) at 1.3119 on a daily closing basis, negating the bearish outlook in the near term.

Adding credence to the renewed upside, the 14-day Relative Strength Index (RSI) has regained the 50 level, currently near 58.00.

On the upside, GBP/USD must crack the falling trendline resistance at 1.3218 before aiming for the 29-month high of 1.3266.

Further up, Pound Sterling buyers will find the next relevant resistance levels at the 1.3300 round level and the 1.3350 psychological barrier.

Should buyers face rejection at the abovementioned trendline barrier at 1.3218, a correction could unfold toward the July 17 high of 1.3045.

A failure to sustain above that level could trigger a fresh decline toward the 50-day SMA at 1.2964.

The next relevant cushion aligns at the March 8 top of 1.2894, a break below which the 100-day SMA support at 1.2819 will come into play.

BoE FAQs

The Bank of England (BoE) decides monetary policy for the United Kingdom. Its primary goal is to achieve ‘price stability’, or a steady inflation rate of 2%. Its tool for achieving this is via the adjustment of base lending rates. The BoE sets the rate at which it lends to commercial banks and banks lend to each other, determining the level of interest rates in the economy overall. This also impacts the value of the Pound Sterling (GBP).

When inflation is above the Bank of England’s target it responds by raising interest rates, making it more expensive for people and businesses to access credit. This is positive for the Pound Sterling because higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls below target, it is a sign economic growth is slowing, and the BoE will consider lowering interest rates to cheapen credit in the hope businesses will borrow to invest in growth-generating projects – a negative for the Pound Sterling.

In extreme situations, the Bank of England can enact a policy called Quantitative Easing (QE). QE is the process by which the BoE substantially increases the flow of credit in a stuck financial system. QE is a last resort policy when lowering interest rates will not achieve the necessary result. The process of QE involves the BoE printing money to buy assets – usually government or AAA-rated corporate bonds – from banks and other financial institutions. QE usually results in a weaker Pound Sterling.

Quantitative tightening (QT) is the reverse of QE, enacted when the economy is strengthening and inflation starts rising. Whilst in QE the Bank of England (BoE) purchases government and corporate bonds from financial institutions to encourage them to lend; in QT, the BoE stops buying more bonds, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive for the Pound Sterling.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.